Canada Macro Daily(Beta Mode)

BoC Eyes Oil Risks in Rate Call

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 32,929.09 | +0.16% |

| USD/CAD | 1.37 | +0.08% |

| EUR/CAD | 1.58 | +0.48% |

| WTI Crude | 94.15 | -2.14% |

| Natural Gas | 2.95 | -2.57% |

| Gold | 4,968.70 | -0.65% |

| Brent Crude | 103.70 | +0.27% |

| Bitcoin | 73,902.58 | -0.03% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

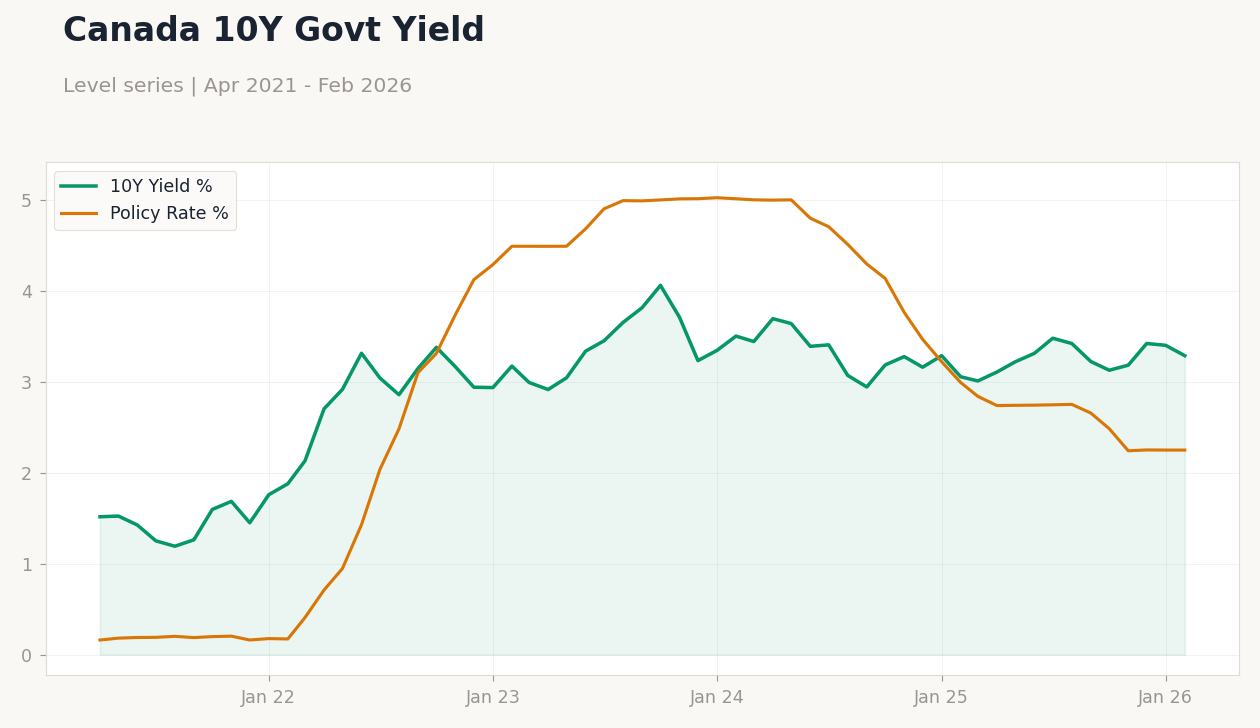

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Housing Starts Level | 250,900 | 252,500 | 238,500 |

| Inflation Rate Year-over-Year | 2.30 | 1.90 | 1.80 |

| Core Inflation Rate Year-over-Year | 2.60 | - | 2.30 |

| Inflation Rate Month-over-Month | 0 | 0.70 | 0.50 |

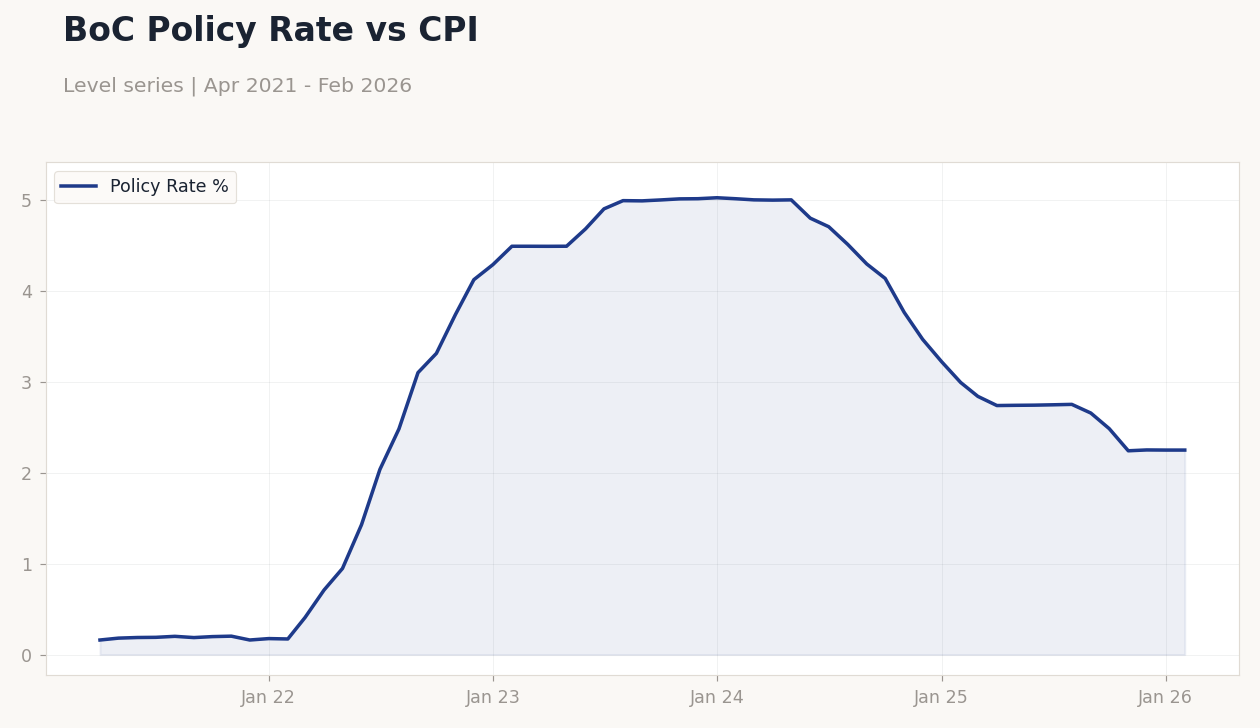

BoC Policy Rate vs CPI | Type: macro_line | Policy Rate %: 2.25 (2026-02-01) | Range: 0.1603–5.026 | Trend(6pt): 0.1603,1.429,4.994,4.138,2.251,2.25

BoC Policy Rate vs CPI | Type: macro_line | Policy Rate %: 2.25 (2026-02-01) | Range: 0.1603–5.026 | Trend(6pt): 0.1603,1.429,4.994,4.138,2.251,2.25

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoC Interest Rate Decision | 2.25 | 2.25 | 05:45 |

| BoC Press Conference | - | - | 06:30 |

| Friday (2026-03-20) | |||

| New Housing Price Index Month-over-Month | -0.40 | -0.30 | 04:30 |

| Retail Sales Excluding Autos Month-over-Month | 0.10 | 1.20 | 04:30 |

| Retail Sales Month-over-Month Final | -0.40 | 1.50 | 04:30 |

| Retail Sales Month-over-Month Prel | 1.50 | - | 04:30 |

- Canadian inflation eased to 1.8% YoY in February, below consensus, while housing starts disappointed at 238,500.

- Markets mixed: TSX up 0.16%, CAD steady, but oil prices volatile on geopolitical tensions.

- BoC rate decision today expected to hold at 2.25%, with focus on oil-driven inflation risks.

Yesterday's Recap

Canadian economic data released yesterday showed softer-than-expected inflation, with the headline rate dropping to 1.8% year-over-year in February, missing the 1.9% consensus and down from January's 2.3%. Core inflation eased to 2.3% year-over-year, signaling cooling price pressures amid subdued demand. Housing starts fell to 238,500 annualized units, below the 252,500 forecast and prior 250,900, reflecting ongoing weakness in the real estate sector tied to high borrowing costs.

Month-over-month inflation rose 0.5%, short of the 0.7% expectation, further easing concerns over persistent price gains. Markets reacted modestly: the S&P/TSX Composite edged up 0.16% to 32,929.09, supported by energy stocks despite WTI crude declining 2.14% to $94.15. USD/CAD ticked up 0.08% to 1.37, while Canada 10-year yields fell 3.35% to 3.29%, pricing in potential BoC caution.

Natural gas dropped 2.57% to $2.95, adding to commodity volatility.

The Day Ahead

The Bank of Canada announces its interest rate decision at 5:45 ET today, with consensus expecting a hold at 2.25% amid elevated oil prices from Middle East tensions. A press conference follows at 6:30 ET, where Governor Tiff Macklem may address inflation risks and forward guidance. No major releases tomorrow, providing markets a breather to digest the BoC's stance.

On Friday, the new housing price index is due at 4:30 ET, with consensus for a -0.3% month-over-month change, highlighting persistent housing affordability issues. Retail sales data releases simultaneously, including month-over-month final at a forecasted 1.5% and ex-autos at 1.2%, offering insights into consumer spending resilience. These figures could influence expectations for future BoC moves.

Other Economic Notes

Broader Canadian economic themes center on the housing market's stagnation, exacerbated by high interest rates and the potential prolongation from Iran War-driven oil shocks, as noted in recent analyses. Debt burdens continue to outweigh the benefits of potential BoC rate cuts, with households facing elevated servicing costs amid slowing wage growth. Energy sector dynamics remain pivotal, with rising oil prices bolstering exports but risking imported inflation, complicating the recovery outlook.