Canada Macro Daily(Beta Mode)

BoC Holds, Flags Oil Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 32,312.67 | -1.87% |

| USD/CAD | 1.37 | +0.34% |

| EUR/CAD | 1.58 | +0.38% |

| WTI Crude | 95.99 | -0.34% |

| Natural Gas | 3.17 | +3.52% |

| Gold | 4,697.50 | -3.93% |

| Brent Crude | 107.73 | +0.33% |

| Bitcoin | 70,130.59 | -1.56% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

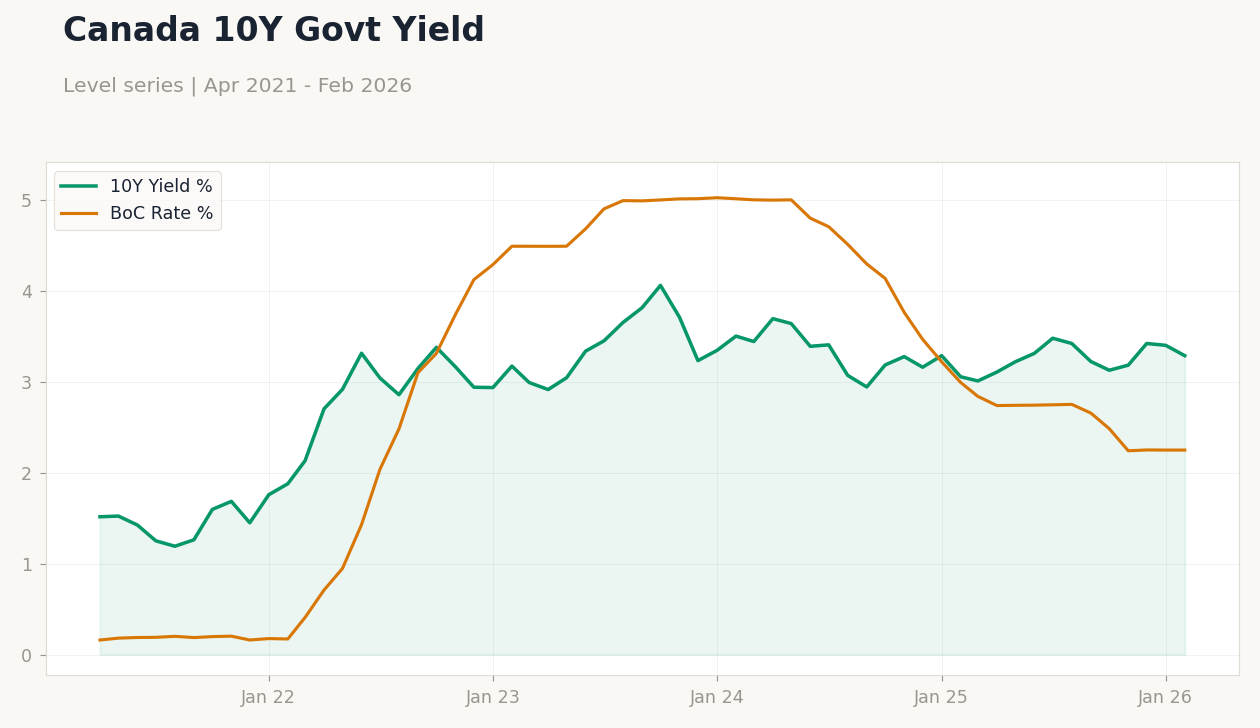

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Housing Starts Level | 250,900 | 252,500 | 238,500 |

| Inflation Rate Year-over-Year | 2.30 | 1.90 | 1.80 |

| Core Inflation Rate Year-over-Year | 2.60 | - | 2.30 |

| Inflation Rate Month-over-Month | 0 | 0.70 | 0.50 |

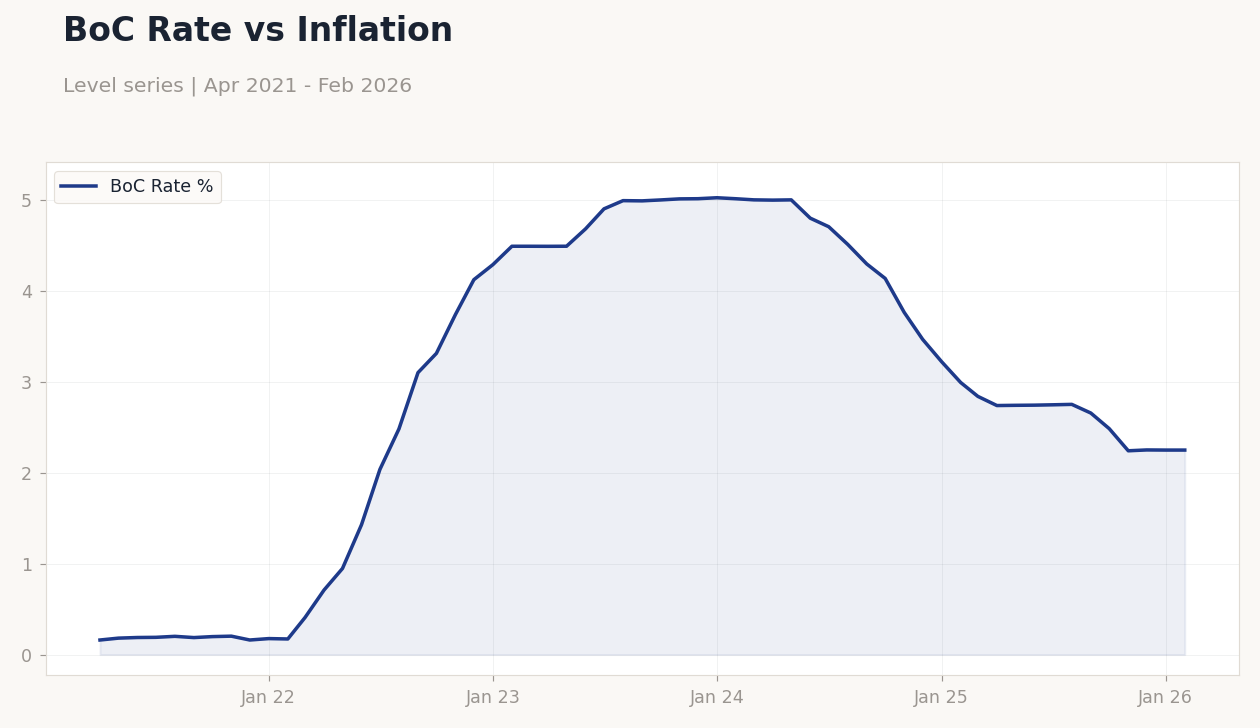

| BoC Interest Rate Decision | 2.25 | 2.25 | 2.25 |

| BoC Press Conference | - | - | - |

BoC Rate vs Inflation | Type: macro_line | BoC Rate %: 2.25 (2026-02-01) | Range: 0.1603–5.026 | Trend(6pt): 0.1603,1.429,4.994,4.138,2.251,2.25

BoC Rate vs Inflation | Type: macro_line | BoC Rate %: 2.25 (2026-02-01) | Range: 0.1603–5.026 | Trend(6pt): 0.1603,1.429,4.994,4.138,2.251,2.25

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-03-20) | |||

| New Housing Price Index Month-over-Month | -0.40 | -0.30 | 04:30 |

| Retail Sales Excluding Autos Month-over-Month | 0.10 | 1.20 | 04:30 |

| Retail Sales Month-over-Month Final | -0.40 | 1.50 | 04:30 |

| Retail Sales Month-over-Month Prel | 1.50 | - | 04:30 |

- Bank of Canada maintains policy rate at 2.25%, citing Middle East tensions and potential oil-driven inflation pressures.

- February inflation data undershot expectations, with YoY rate at 1.8% versus 1.9% consensus, easing some rate cut bets.

- Housing starts disappointed at 238,500, signaling ongoing weakness in residential construction amid high borrowing costs.

Yesterday's Recap

Canadian markets reacted to the Bank of Canada's rate decision and softer inflation data, with the S&P/TSX Composite closing down 1.87% at 32,312.67, driven by declines in energy and materials sectors. USD/CAD rose 0.34% to 1.37, reflecting a stronger U.S. dollar and commodity price volatility, while EUR/CAD gained 0.38% to 1.58.

February's inflation release showed YoY CPI at 1.8% against a 1.9% consensus, with core inflation at 2.3% and MoM at 0.5% versus 0.7% expected, pressuring bond yields lower as the 10-year Government of Canada yield fell 3.35% to 3.29%. Housing starts came in at 238,500, below the 252,500 forecast, highlighting persistent softness in the housing market. The BoC held its policy rate at 2.25% as anticipated, with the subsequent press conference emphasizing risks from Middle East conflicts on oil prices.

WTI crude dipped 0.34% to 95.99, while natural gas surged 3.52% to 3.17 amid supply concerns. Gold tumbled 3.93% to 4,697.50, mirroring broader safe-haven unwinds. Brent crude edged up 0.33% to 107.73, and Bitcoin fell 1.56% to 70,130.59.

The 2-year Canada government yield held steady at 2.25%.

The Day Ahead

Tomorrow brings key releases on March 20, including the New Housing Price Index MoM, expected at -0.3% following -0.4% prior, which could underscore cooling in real estate amid elevated rates. Retail sales data will be in focus, with MoM final consensus at 1.5% after -0.4% previous, potentially signaling consumer spending resilience. Excluding autos, retail sales are forecasted at 1.2% MoM versus 0.1% prior, offering insights into core consumption trends.

Preliminary retail sales MoM lacks a consensus but follows 1.5% prior, adding to volatility expectations. No major events today on March 19, allowing markets to digest yesterday's BoC hold and global oil dynamics. Traders will watch for any spillover from U.S.

Fed decisions impacting CAD crosses.

Other Economic Notes

Broader Canadian economic themes point to a slowdown in housing activity, exacerbated by high interest rates and affordability challenges, as evidenced by weak starts and price indices. (cont...)