Canada Macro Daily(Beta Mode)

CAD Slips Amid Oil Turmoil

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 31,934.90 | -0.08% |

| USD/CAD | 1.39 | +0.34% |

| EUR/CAD | 1.60 | +0.16% |

| WTI Crude | 103.53 | +0.63% |

| Natural Gas | 2.83 | -1.84% |

| Gold | 4,604.80 | +1.74% |

| Brent Crude | 107.44 | -4.73% |

| Bitcoin | 66,727.11 | +0.05% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

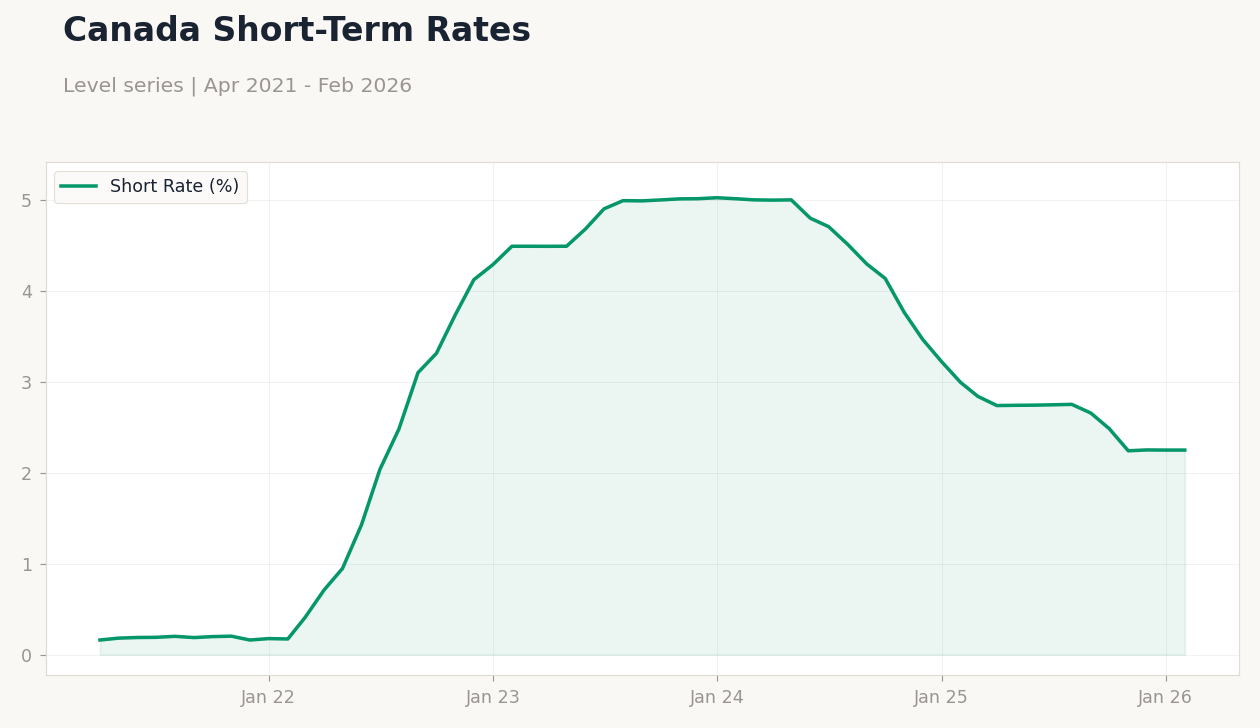

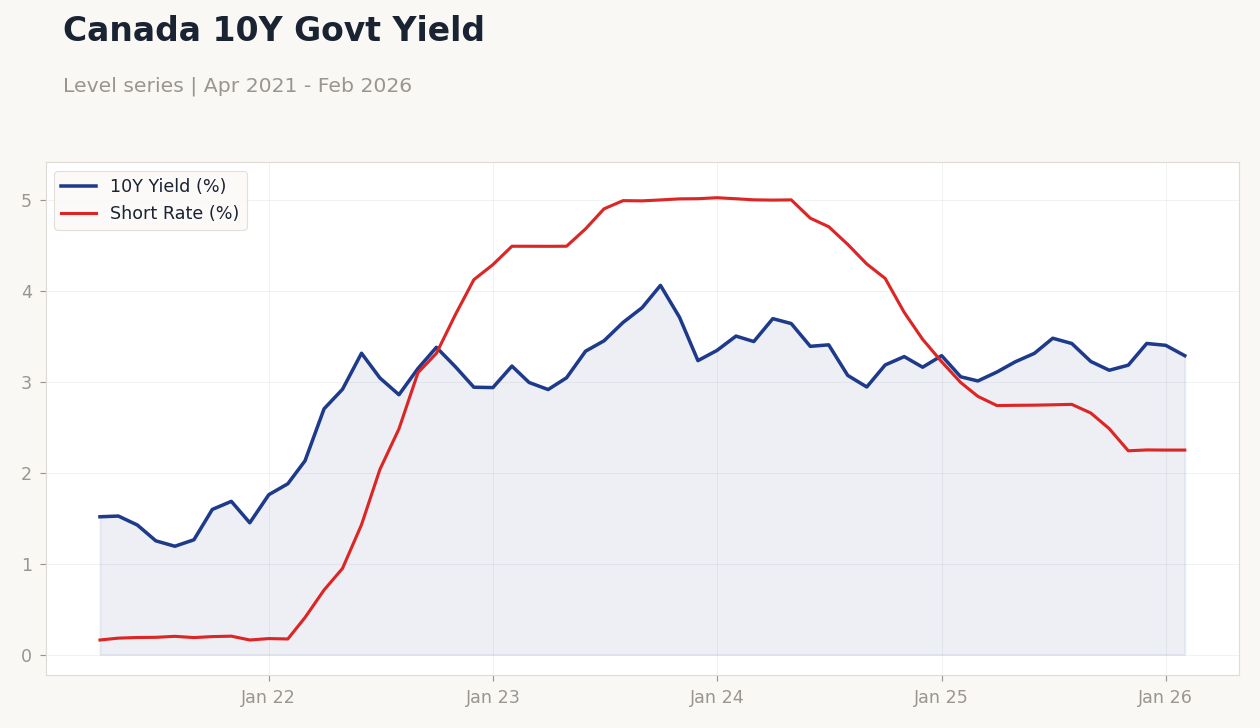

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield (%): 3.288 (2026-02-01) | Range: 1.192–4.062 | Trend(6pt): 1.516,3.315,3.654,3.186,3.423,3.288 | Short Rate (%): 2.25 (2026-02-01) | Range: 0.1603–5.026 | Trend(6pt): 0.1603,1.429,4.994,4.138,2.251,2.25

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield (%): 3.288 (2026-02-01) | Range: 1.192–4.062 | Trend(6pt): 1.516,3.315,3.654,3.186,3.423,3.288 | Short Rate (%): 2.25 (2026-02-01) | Range: 0.1603–5.026 | Trend(6pt): 0.1603,1.429,4.994,4.138,2.251,2.25

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Month-over-Month | 0.20 | 0 | 04:30 |

| GDP Month-over-Month Prel | 0 | - | 04:30 |

| Wednesday (2026-04-01) | |||

| S&P Global Manufacturing PMI Index | 51 | - | 05:30 |

| BoC Summary of Deliberations | - | - | 09:30 |

| Thursday (2026-04-02) | |||

| Trade Balance | -3,650m | -1,900m | 04:30 |

- Canadian markets mixed as oil volatility from Iran war pressures CAD and TSX energy sector.

- Bond yields fall, signaling rate-cut bets; gold surges as safe haven.

- No major data releases yesterday; focus shifts to today's GDP figures.

Yesterday's Recap

Canadian markets ended mixed on March 30, with the S&P/TSX Composite dipping 0.08% to 31,934.90, dragged by energy weakness amid volatile oil prices from the Iran conflict. USD/CAD rose 0.34% to 1.39, reflecting CAD softening on commodity pressures, while EUR/CAD edged up 0.16% to 1.60. WTI Crude climbed 0.63% to 103.53, but Brent Crude fell sharply by 4.73% to 107.44, highlighting supply disruption fears.

Natural Gas declined 1.84% to 2.83, pressured by milder demand outlooks. Gold rallied 1.74% to 4,604.80 as investors sought havens amid global tensions. Canada 10Y Govt Yield dropped 3.35% to 3.29%, with the 2Y unchanged at 2.25%, as markets priced in potential BoC easing.

Bitcoin held steady with a minimal 0.05% gain to 66,727.11, decoupled from broader risk-off moves.

The Day Ahead

Today's key releases include GDP Month-over-Month and its preliminary reading at 04:30 ET, with consensus expecting flat growth following a prior 0.2% print, potentially influencing CAD and TSX sentiment. Tomorrow brings the S&P Global Manufacturing PMI at 05:30 ET, previous at 51.0, offering insights into industrial health amid global trade strains. Also on April 1, the BoC Summary of Deliberations at 09:30 ET could clarify recent policy thinking, impacting rate expectations.

Thursday features the Trade Balance at 04:30 ET, with consensus at -1.9 billion versus prior -3.65 billion, key for export-dependent sectors. These events may drive volatility in CAD crosses and energy stocks. Markets will watch for any signals on inflation or growth slowdowns.

Other Economic Notes

Broader Canadian themes highlight energy sector vulnerability, with oil price shocks from the Iran war boosting WTI but pressuring natural gas amid supply chain disruptions. Housing and retail face headwinds from high rates, as seen in softer CPI trends at 2.32% YoY, potentially easing affordability pressures. Corporate developments, like Canopy Growth's awards and Bombardier's debt extensions, underscore resilience in cannabis and aerospace amid economic uncertainty.