Canada Macro Daily(Beta Mode)

GDP Edges Up, Oil Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 32,768.00 | +2.61% |

| USD/CAD | 1.39 | -0.24% |

| EUR/CAD | 1.60 | -0.10% |

| WTI Crude | 99.16 | -2.19% |

| Natural Gas | 2.85 | -1.28% |

| Gold | 4,773.00 | +2.70% |

| Brent Crude | 102.15 | -13.69% |

| Bitcoin | 68,547.81 | +0.46% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Month-over-Month | 0.20 | 0 | 0.10 |

| GDP Month-over-Month Prel | 0 | - | 0.20 |

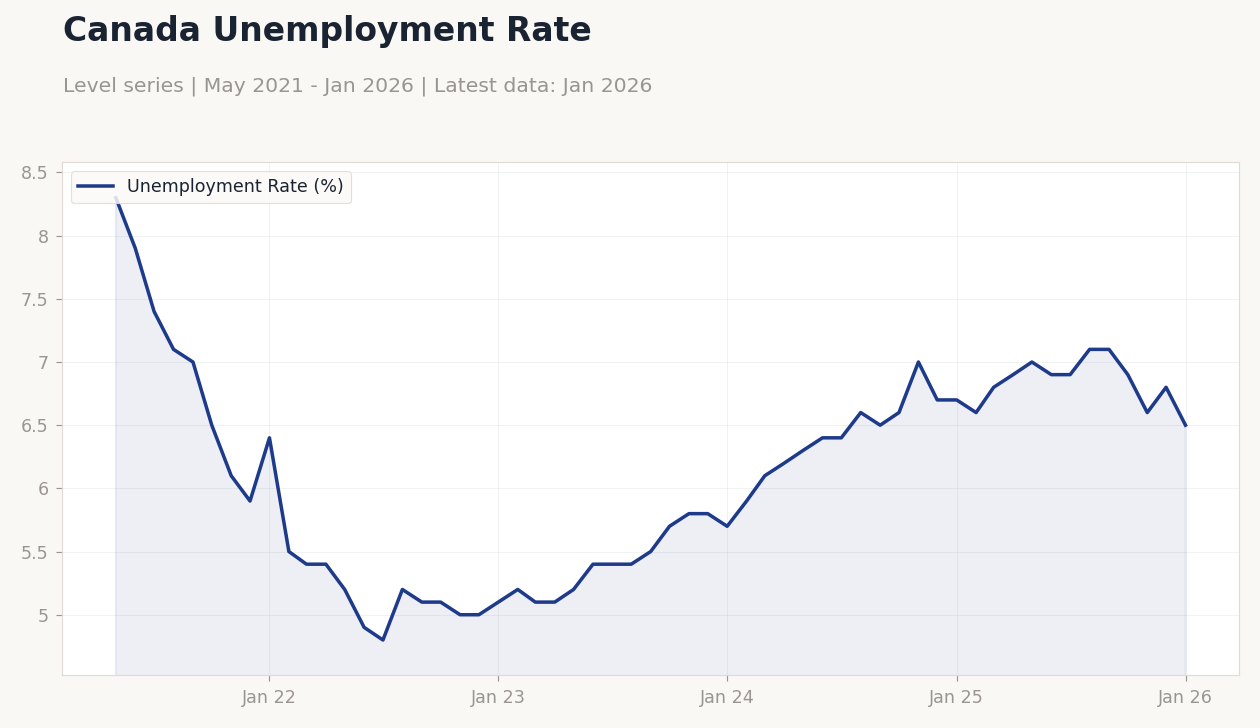

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.5 (2026-01-01) | Range: 4.8–8.3 | Trend(5pt): 8.3,4.8,5.5,7,6.5

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.5 (2026-01-01) | Range: 4.8–8.3 | Trend(5pt): 8.3,4.8,5.5,7,6.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Index | 51 | - | 05:30 |

| BoC Summary of Deliberations | - | - | 09:30 |

| Thursday (2026-04-02) | |||

| Trade Balance | -3,650m | -2,300m | 04:30 |

- Canadian GDP rose 0.1% m/m in February, beating consensus of 0%, with preliminary March at 0.2%, signaling modest growth amid global headwinds.

- S&P/TSX surged 2.61% to 32,768.00, buoyed by commodity rebounds, while WTI crude fell 2.19% to $99.16 amid Iran war volatility.

- USD/CAD dipped 0.24% to 1.39, reflecting CAD strength on GDP data, as Canada 10Y yield dropped 3.35% to 3.29%.

Yesterday's Recap

Canadian GDP for February advanced 0.1% month-over-month, surpassing the consensus flat reading, driven by services sector resilience despite manufacturing drags, while the preliminary March figure showed 0.2% growth, easing some recession concerns. Markets reacted positively, with the S&P/TSX Composite climbing 2.61% to 32,768.00, led by gains in mining and energy stocks amid gold's 2.70% rise to $4,773.00. USD/CAD edged down 0.24% to 1.39, supported by the upbeat data, though EUR/CAD slipped just 0.10% to 1.60.

Energy commodities weakened, with WTI crude dropping 2.19% to $99.16 and Brent crude plunging 13.69% to $102.15, pressured by Iran war disruptions and supply chain fears. Natural gas fell 1.28% to $2.85, reflecting milder demand outlooks. Canada 2Y government yield held steady at 2.25%, but the 10Y yield declined 3.35% to 3.29%, signaling increased bets on BoC easing.

Overall, the session highlighted Canada's economic stability against global volatility, with Bitcoin up modestly 0.46% to $68,547.81.

The Day Ahead

Today's S&P Global Manufacturing PMI at 05:30 ET is expected to provide insights into factory activity, following February's 51.0 reading, potentially influencing TSX industrials if it signals expansion. The BoC Summary of Deliberations at 09:30 ET will detail the rationale behind recent policy holds, offering clues on inflation and growth views amid the 2.25% policy rate. Tomorrow's Trade Balance release at 04:30 ET, with consensus at -2.3 billion versus previous -3.65 billion, could sway CAD crosses if exports rebound on energy prices.

Markets will watch for any spillover from global oil fluctuations, especially with Iran war rhetoric impacting commodity trades. Broader events include monitoring US data for cross-border effects on Canadian yields. Expect volatility in energy-linked assets like natural gas and TSX resources.

Other Economic Notes

Broader themes include persistent inflation pressures, with Canada CPI at 2.32% YoY as of March 2025, complicating BoC's balancing act between growth support and price stability. (cont...)