Canada Macro Daily(Beta Mode)

GDP Edges Up, BoC Eyes Oil Shock

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 32,958.00 | +0.58% |

| USD/CAD | 1.39 | +0.15% |

| EUR/CAD | 1.60 | -0.33% |

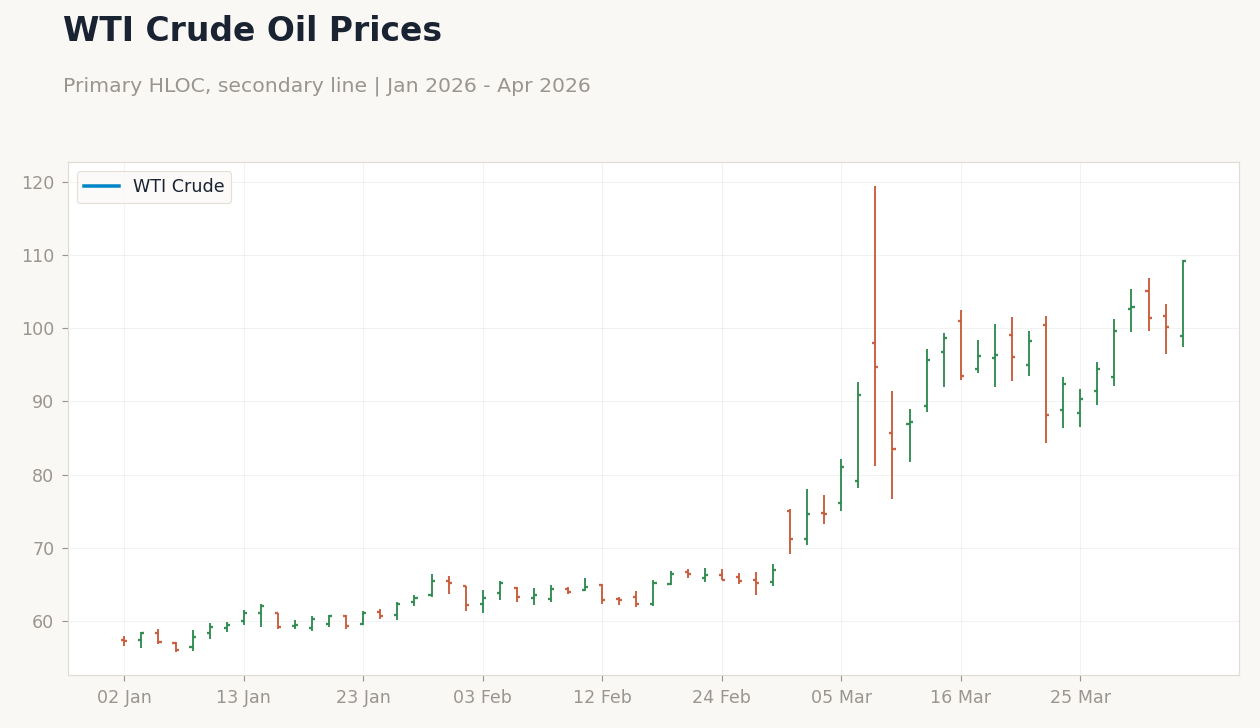

| WTI Crude | 109.07 | +8.94% |

| Natural Gas | 2.84 | +0.67% |

| Gold | 4,637.00 | -3.06% |

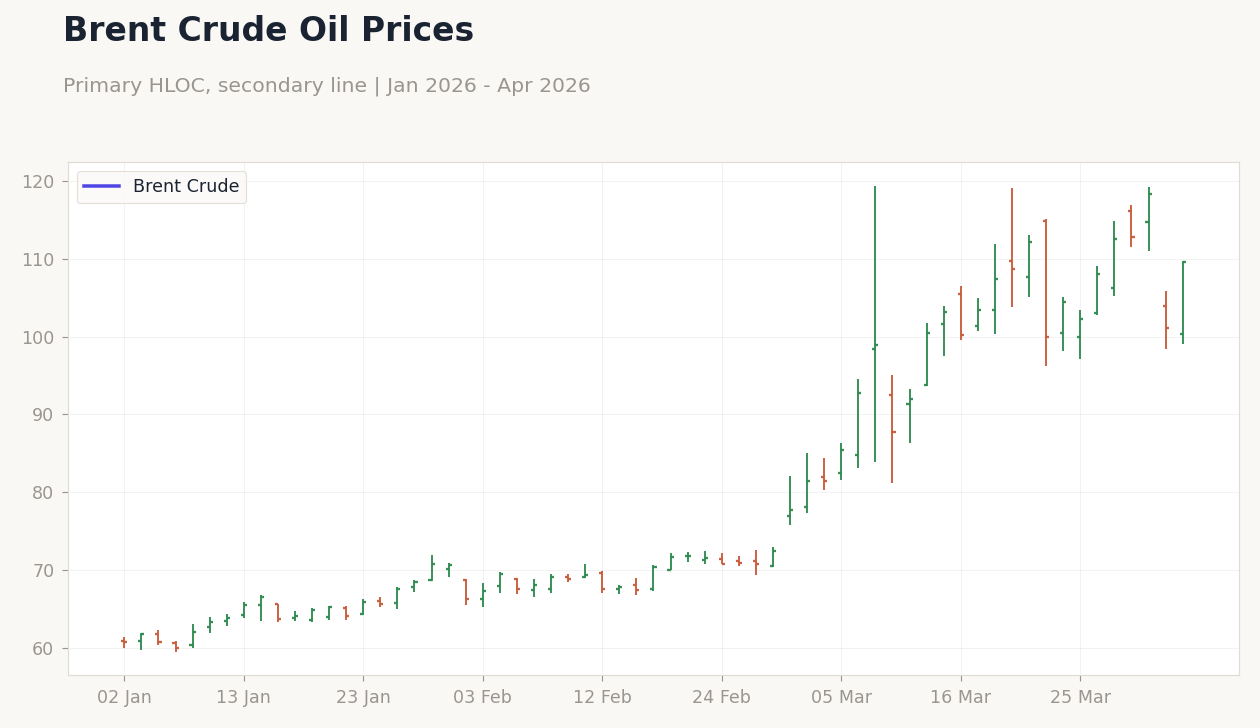

| Brent Crude | 109.52 | +8.26% |

| Bitcoin | 66,369.23 | -2.51% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Month-over-Month | 0.20 | 0 | 0.10 |

| GDP Month-over-Month Prel | 0 | - | 0.20 |

| S&P Global Manufacturing PMI Index | 51 | - | 50 |

| BoC Summary of Deliberations | - | - | "" |

BoC Policy Rate vs Inflation | Type: macro_line | Short-term Rate (%): 2.25 (2026-02-01) | Range: 0.1604–5.026 | Trend(5pt): 0.1809,2.037,4.992,3.765,2.25

BoC Policy Rate vs Inflation | Type: macro_line | Short-term Rate (%): 2.25 (2026-02-01) | Range: 0.1604–5.026 | Trend(5pt): 0.1809,2.037,4.992,3.765,2.25

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | -3,650m | -2,300m | 04:30 |

- Canadian GDP rose 0.1% MoM in February, beating consensus of 0%, while preliminary March data showed 0.2% growth, signaling fragile economic momentum amid external shocks.

- S&P Global Manufacturing PMI fell to 50.0 from 51.0, indicating stagnation in factory activity, with markets reacting to BoC's summary highlighting Iran war risks to inflation.

- TSX climbed 0.58% on energy gains from surging oil prices, while USD/CAD rose 0.15% to 1.39 as dovish BoC signals weighed on the loonie.

Yesterday's Recap

Canadian GDP for February advanced 0.1% month-over-month, surpassing consensus expectations of no change and following a 0.2% prior reading, though the preliminary March figure at 0.2% suggested ongoing but tepid expansion. The S&P Global Manufacturing PMI dropped to 50.0 from 51.0, reflecting neutral conditions in the sector amid supply chain pressures from global energy disruptions. The Bank of Canada released its Summary of Deliberations, emphasizing concerns over the Iran war's impact on oil prices and inflation, without altering the policy rate.

Market reactions included a 0.58% rise in the S&P/TSX to 32,958.00, driven by energy stocks as WTI crude surged 8.94% to 109.07 and Brent climbed 8.26% to 109.52. USD/CAD strengthened 0.15% to 1.39, while EUR/CAD weakened 0.33% to 1.60, reflecting CAD vulnerability to oil volatility and dovish BoC tones. Canada 10Y government yield fell 3.35% to 3.29%, signaling easing bets, while the 2Y yield held steady at 2.25%.

Gold dropped 3.06% to 4,637.00, pressured by a firmer dollar, and natural gas edged up 0.67% to 2.84.

The Day Ahead

Canada's February trade balance is due at 4:30 ET, with consensus expecting a deficit of -2.3 billion CAD, narrower than January's -3.65 billion, potentially supporting CAD if exports benefit from higher oil prices. A wider-than-expected deficit could pressure the loonie amid ongoing energy market turbulence. No other major Canadian data releases are scheduled, shifting focus to global cues like US factory orders.

Markets will watch for any spillover from rising oil prices on Canadian energy equities and bond yields. Broader sentiment may hinge on geopolitical developments in the Iran conflict, influencing commodity dynamics.

Other Economic Notes

Canada's housing crisis continues to undermine productivity, as shortages limit labor mobility to high-growth regions, exacerbating economic drag per recent analyses. (cont...)