Canada Macro Daily(Beta Mode)

BoC Holds Amid Oil Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,182.00 | +0.22% |

| USD/CAD | 1.39 | -0.22% |

| EUR/CAD | 1.61 | +0.19% |

| WTI Crude | 114.67 | +2.01% |

| Natural Gas | 2.83 | +0.71% |

| Gold | 4,672.70 | +0.34% |

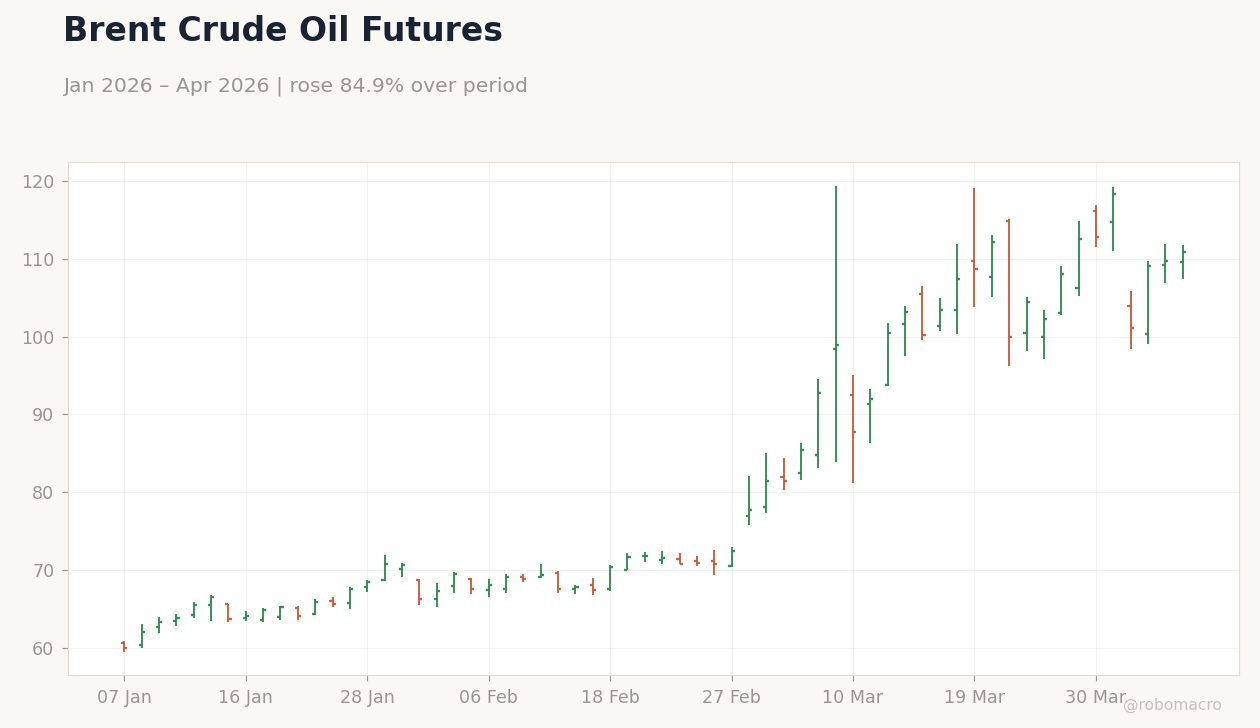

| Brent Crude | 110.74 | +0.88% |

| Bitcoin | 68,413.80 | -0.65% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

WTI Crude Oil Prices | Type: macro_line | WTI Price ($/Barrel): 104.7 (2026-03-30) | Range: 55.44–123.6 | Trend(6pt): 59.61,110.3,91.43,70.87,96.18,104.7

WTI Crude Oil Prices | Type: macro_line | WTI Price ($/Barrel): 104.7 (2026-03-30) | Range: 55.44–123.6 | Trend(6pt): 59.61,110.3,91.43,70.87,96.18,104.7

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ivey PMI Seasonally Adjusted | 56.60 | 57.20 | 06:00 |

| Friday (2026-04-10) | |||

| Headline Unemployment Rate | 6.70 | 6.80 | 04:30 |

| Employment Change | -83,900 | 15,000 | 04:30 |

| Full-Time Employment Change | -108,400 | - | 04:30 |

| Labor Force Participation | 64.90 | - | 04:30 |

| Part-Time Employment Change | 24,500 | - | 04:30 |

- Canadian markets edged higher with TSX up 0.22% on oil gains, despite limited CAD strength.

- BoC expected to maintain rates at 2.25% amid Middle East tensions boosting WTI to $114.67.

- Services sector contraction weighs on CAD, with USD/CAD dipping slightly to 1.39.

Yesterday's Recap

Canadian markets showed modest gains yesterday with the S&P/TSX Composite closing at 33,182.00, up 0.22%, driven by energy sector strength amid rising oil prices. WTI Crude advanced 2.01% to $114.67, supported by Middle East supply concerns, while Brent Crude rose 0.88% to $110.74. Natural Gas edged up 0.71% to $2.83, reflecting stable demand outlooks.

The Canadian dollar posted limited gains, with USD/CAD falling 0.22% to 1.39 as services economy shrinkage offset oil buoyancy, and EUR/CAD climbed 0.19% to 1.61. Government bond yields diverged, with the 10-year yield dropping 3.35% to 3.29% on safe-haven flows, while the 2-year yield held steady at 2.25%. Gold rose 0.34% to $4,672.70, and Bitcoin dipped 0.65% to $68,413.80, mirroring mixed global risk sentiment.

No major data releases occurred, but bank stocks like Royal Bank of Canada and National Bank of Canada outperformed, lifting financials.

The Day Ahead

Today's key release is the Ivey PMI Seasonally Adjusted at 06:00 ET, with consensus at 57.2 versus previous 56.6, potentially signaling manufacturing resilience amid oil-driven growth. A stronger-than-expected print could bolster CAD and TSX energy shares, while a miss might pressure yields lower. Looking ahead to Friday, the headline Unemployment Rate is forecast at 6.8% from 6.7%, alongside Employment Change consensus of 15,000 after a prior drop of -83,900.

Full-Time and Part-Time Employment Changes, plus Labor Force Participation at 64.9% prior, will provide labor market depth. These figures could influence BoC rate expectations, with softer data raising cut odds. No other events today, but markets will watch global oil dynamics for CAD crosses.

Other Economic Notes

Broader themes highlight persistent services sector weakness, as evidenced by shrinking activity limiting CAD gains despite oil surges. Housing affordability remains strained under the 2.25% policy rate, with potential for further pressure if unemployment rises. Energy exports continue to support trade balances, but trade uncertainty from U.S.

policies weighs on overall growth prospects.