Canada Macro Daily(Beta Mode)

PMI Plunges, Yields Drop

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,477.70 | -0.43% |

| USD/CAD | 1.38 | -0.11% |

| EUR/CAD | 1.62 | +0.36% |

| WTI Crude | 97.88 | +0.01% |

| Natural Gas | 2.67 | +0.11% |

| Gold | 4,786.20 | -0.13% |

| Brent Crude | 96.00 | +0.08% |

| Bitcoin | 72,223.99 | +0.64% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

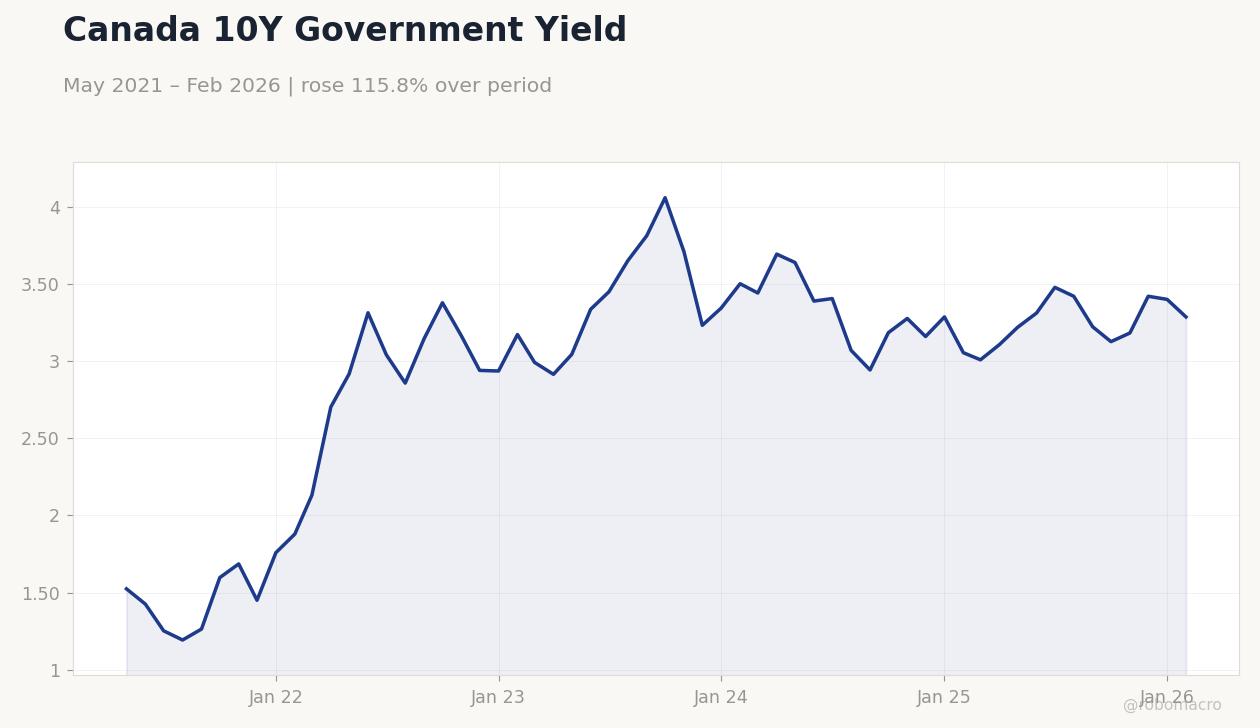

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Ivey PMI Seasonally Adjusted | 56.60 | 55.90 | 49.70 |

Canada 10Y Government Yield | Type: macro_line | 10Y Yield (%): 3.288 (2026-02-01) | Range: 1.192–4.062 | Trend(6pt): 1.524,3.043,3.816,3.279,3.402,3.288

Canada 10Y Government Yield | Type: macro_line | 10Y Yield (%): 3.288 (2026-02-01) | Range: 1.192–4.062 | Trend(6pt): 1.524,3.043,3.816,3.279,3.402,3.288

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 6.70 | 6.80 | 04:30 |

| Employment Change | -83,900 | 15,000 | 04:30 |

| Full-Time Employment Change | -108,400 | - | 04:30 |

| Labor Force Participation | 64.90 | - | 04:30 |

| Part-Time Employment Change | 24,500 | - | 04:30 |

- Ivey PMI fell to 49.7, below 55.9 consensus, signaling contraction and weighing on CAD sentiment.

- TSX declined 0.43% to 33,477.70; 10Y yields dropped 3.35% to 3.29% on easing bets.

- Jobs data ahead, with unemployment expected at 6.8%, may shape BoC rate outlook.

Yesterday's Recap

Canada's Ivey PMI seasonally adjusted dropped to 49.7, missing the 55.9 consensus and down from 56.6 prior, indicating business activity contraction and raising slowdown concerns. The S&P/TSX Composite closed at 33,477.70, down 0.43%, amid market caution despite energy resilience. USD/CAD eased 0.11% to 1.38, supported by stable oil, while EUR/CAD rose 0.36% to 1.62 on euro gains.

Canada 10Y yields fell 3.35% to 3.29%, and 2Y yields held at 2.25%, reflecting dovish BoC bets. WTI Crude rose 0.01% to 97.88, Brent gained 0.08% to 96.00, buoyed by demand signals, while natural gas increased 0.11% to 2.67. Gold dipped 0.13% to 4,786.20, and Bitcoin climbed 0.64% to 72,223.99, showing mixed sentiment.

Markets viewed the PMI miss as supporting potential BoC easing, with limited CAD volatility.

The Day Ahead

Canada's labor data releases at 4:30 ET, featuring unemployment rate consensus at 6.8% from 6.7% prior, potentially affecting BoC's rate path if softening emerges. Employment change is forecast at 15,000 after -83,900 prior, with full-time, part-time changes, and participation from 64.9%. Weak results could pressure CAD, amid global inflation focus.

No BoC events scheduled, but watch for comments on data. Attention includes U.S. indicators' spillover to TSX and yields.

Other Economic Notes

Housing strains persist, with studies showing EV adoption could save costs amid high fuel prices, per recent reports. Energy dynamics are key, as oil stability aids exports but PMI weakness highlights manufacturing risks. Fiscal deficits may heighten inflation if unmanaged, impacting yields.

Bank stocks like Royal and National rose, outperforming amid strong momentum and AGM results rejecting proposals.

Global Macro News

Inflation worries continue globally, with Thailand's central bank holding rates to support growth despite price rises, mirroring commodity pressures on Canada. U.S. dollar gains offset CAD's oil benefits, as prices eased, per analyses.

(cont...)