Canada Macro Daily(Beta Mode)

Oil Gains, Yields Dip on BoC Outlook

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,102.40 | +0.66% |

| USD/CAD | 1.38 | -0.00% |

| EUR/CAD | 1.62 | +0.09% |

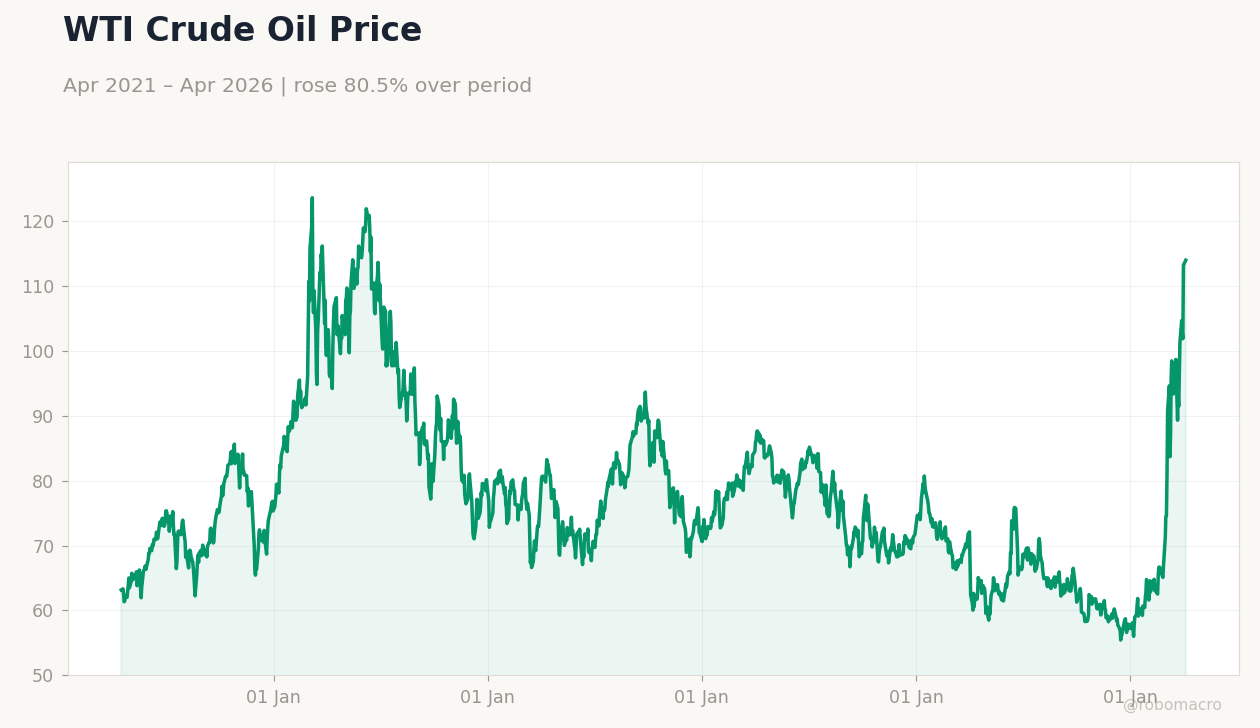

| WTI Crude | 92.32 | +1.14% |

| Natural Gas | 2.59 | -0.46% |

| Gold | 4,829.00 | +0.08% |

| Brent Crude | 95.82 | +1.09% |

| Bitcoin | 74,058.75 | -0.17% |

| Canada 2Y Govt Yield | 2.25% | +0.00% |

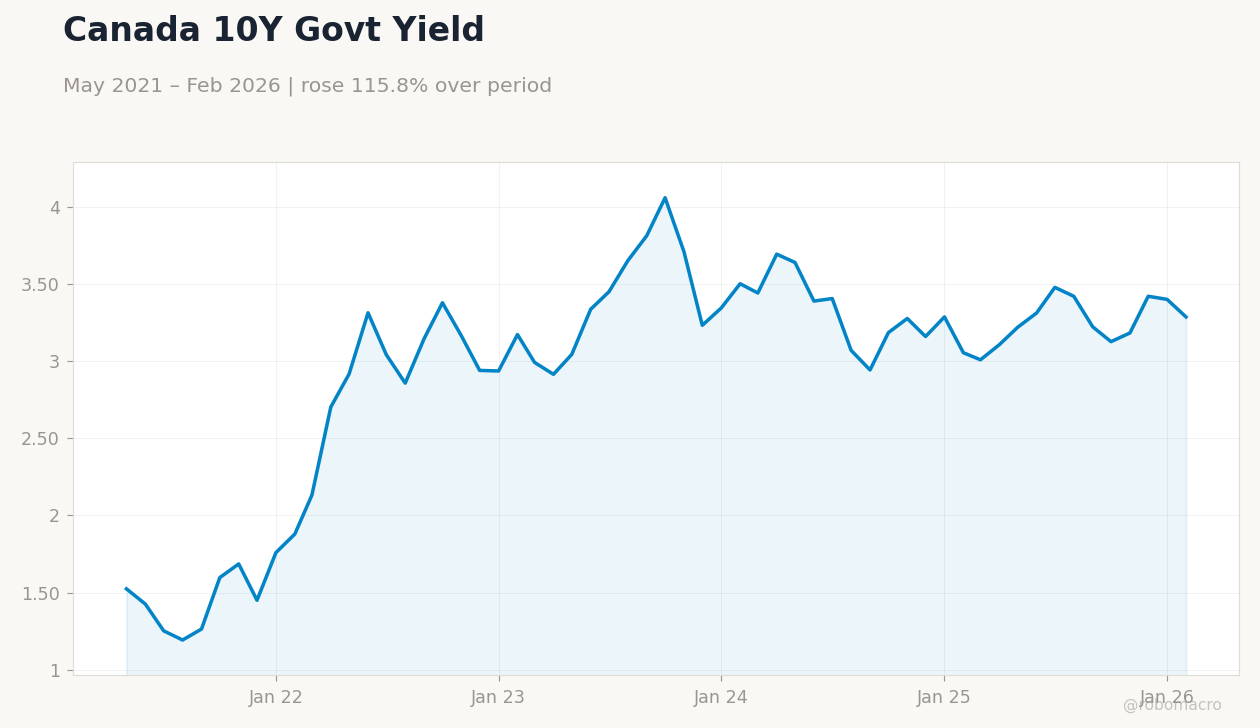

| Canada 10Y Govt Yield | 3.29% | -3.35% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Canada Policy Rate | Type: macro_line | Rate %: 2.25 (2026-02-01) | Range: 0.1604–5.026 | Trend(5pt): 0.1809,2.037,4.992,3.765,2.25

Canada Policy Rate | Type: macro_line | Rate %: 2.25 (2026-02-01) | Range: 0.1604–5.026 | Trend(5pt): 0.1809,2.037,4.992,3.765,2.25

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-04-17) | |||

| Housing Starts Level | 250,900 | 255,000 | 04:15 |

- Canadian markets rose modestly with S&P/TSX up 0.66% amid stable CAD and falling 10Y yields.

- News highlights BoC's view of prolonged economic detour but later growth, with oil spikes unlikely to reignite inflation.

- Global context includes Fed's wait-and-see on rates and easing oil fears supporting CAD strength.

Yesterday's Recap

Canadian markets showed resilience on April 14, with the S&P/TSX Composite climbing 0.66% to 34,102.40, driven by gains in non-energy sectors offsetting commodity volatility. USD/CAD held steady at 1.38 with no daily change, while EUR/CAD edged up 0.09% to 1.62, reflecting a risk-on mood pressuring the US dollar. WTI Crude advanced 1.14% to 92.32 and Brent Crude rose 1.09% to 95.82, buoyed by supply concerns despite no major disruptions.

Natural Gas dipped 0.46% to 2.59, weighed by mild demand forecasts, while Gold inched up 0.08% to 4,829.00 as an inflation hedge. Canada 10Y Government Yield fell 3.35% to 3.29%, signaling easing rate expectations, and the 2Y Yield remained flat at 2.25%. Bitcoin slipped 0.17% to 74,058.75 amid broader crypto caution.

No economic data releases occurred, but news on March jobs adding 14,000 positions, holding unemployment at 6.7%, supported market sentiment.

The Day Ahead

On April 15, no major Canadian economic releases are scheduled, providing a quiet day for markets to digest recent news flows. Attention turns to upcoming US data, including potential jobless claims that could influence CAD crosses. Looking further, Housing Starts data on April 17 at 4:15 ET is anticipated, with consensus at 255,000 versus previous 250,900, offering insights into residential construction trends.

Bank of Canada officials have no speeches planned, keeping focus on global rate narratives. Markets may react to any geopolitical updates on the Iran war, impacting oil and yields. Overall, low event risk suggests CAD stability unless external shocks emerge.

Other Economic Notes

Broader themes include persistent inflation concerns, with opinion pieces calling for a "war on inflation" amid stable CPI at 2.32% YoY as of March 2025. Housing market warnings highlight recession risks, potentially cooling prices if global downturns intensify. Fiscal outlooks, including TD Securities' analysis of Mark Carney's prospects, underscore prudent budgeting needs amid green subsidies.