Canada Macro Daily(Beta Mode)

TSX Edges Up, Yields Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,156.00 | +0.16% |

| USD/CAD | 1.37 | -0.27% |

| EUR/CAD | 1.62 | -0.42% |

| WTI Crude | 88.55 | -3.00% |

| Natural Gas | 2.62 | +0.50% |

| Gold | 4,838.50 | +0.80% |

| Brent Crude | 95.75 | +0.86% |

| Bitcoin | 74,700.68 | -0.14% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

BoC Short-Term Rates | Type: macro_line | Short-Term Rate %: 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

BoC Short-Term Rates | Type: macro_line | Short-Term Rate %: 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-04-17) | |||

| Housing Starts Level | 250,900 | 255,000 | 04:15 |

- S&P/TSX rose modestly amid mixed commodity moves, with yields surging on inflation concerns.

- CAD strengthened versus USD as risk appetite improved, despite falling oil prices.

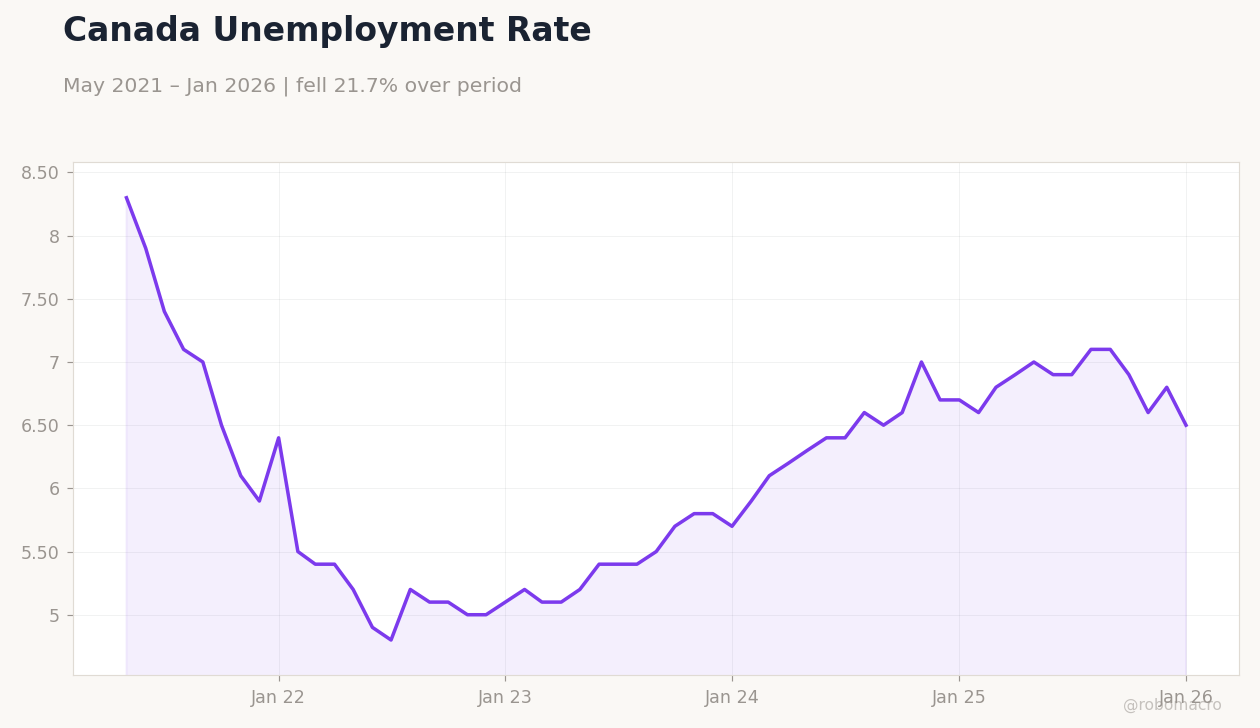

- BoC signals cautious stance on rates amid steady unemployment and disinflation trends.

Yesterday's Recap

Canadian markets showed resilience with the S&P/TSX Composite closing at 34,156.00, up 0.16%, driven by gains in financials despite energy sector weakness. USD/CAD fell to 1.37, down 0.27%, as a risk-on mood bolstered the loonie, while EUR/CAD dropped 0.42% to 1.62. Government bond yields climbed sharply, with the 10-year at 3.44% (up 4.61%) and 2-year at 2.26% (up 0.44%), reflecting bets on persistent inflation.

WTI Crude plunged 3.00% to 88.55, pressured by global demand fears, contrasting with Natural Gas up 0.50% to 2.62 on supply dynamics. Gold advanced 0.80% to 4,838.50, serving as a haven amid volatility, while Bitcoin edged down 0.14% to 74,700.68. Brent Crude bucked the trend, rising 0.86% to 95.75, highlighting divergent oil market signals.

No major data releases occurred, but sentiment was influenced by steady unemployment reports from prior periods.

The Day Ahead

Tomorrow brings the Housing Starts release at 04:15 ET, with consensus at 255,000 versus previous 250,900, offering insights into residential investment amid high rates. This medium-impact data could sway CAD if it signals cooling construction activity. No events are scheduled for today, allowing markets to digest recent yield movements and commodity shifts.

Broader focus will be on U.S. data spillover, potentially affecting CAD crosses. Expect volatility in energy prices to influence TSX energy stocks.

Traders should monitor any unscheduled BoC commentary for rate clues.

Other Economic Notes

Unemployment in Canada has steadied with modest hiring recovery, supporting consumer spending but raising questions on wage pressures. Rising oil prices are unlikely to strongly revive inflation, per banking estimates, easing some BoC concerns. Broader themes include sustainability efforts, as seen in Royal Bank's 2025 report, tying into green finance trends.

Calls for a "war on inflation" highlight political pressures on monetary policy.