Canada Macro Daily(Beta Mode)

Inflation Edges Up, BoC Appoints Deputies

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,360.00 | +0.04% |

| USD/CAD | 1.37 | +0.03% |

| EUR/CAD | 1.61 | -0.14% |

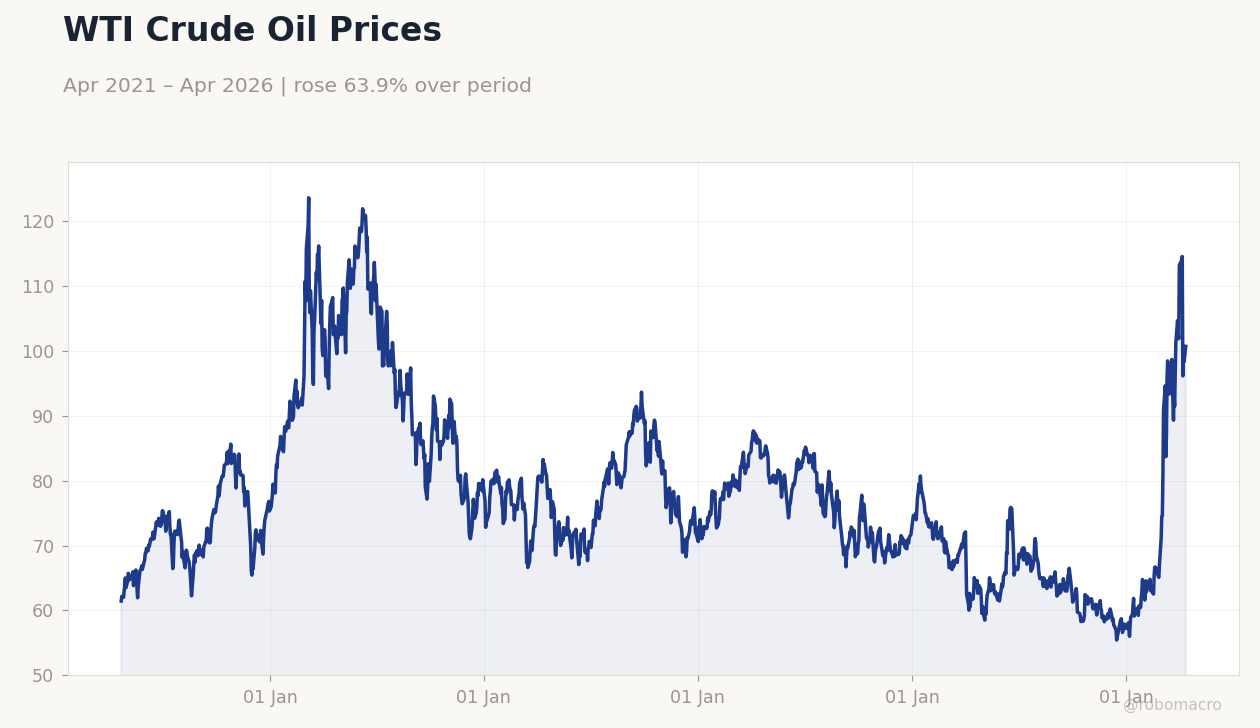

| WTI Crude | 87.27 | -2.61% |

| Natural Gas | 2.67 | -0.67% |

| Gold | 4,803.30 | -0.07% |

| Brent Crude | 90.50 | -5.22% |

| Bitcoin | 76,642.01 | +1.01% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

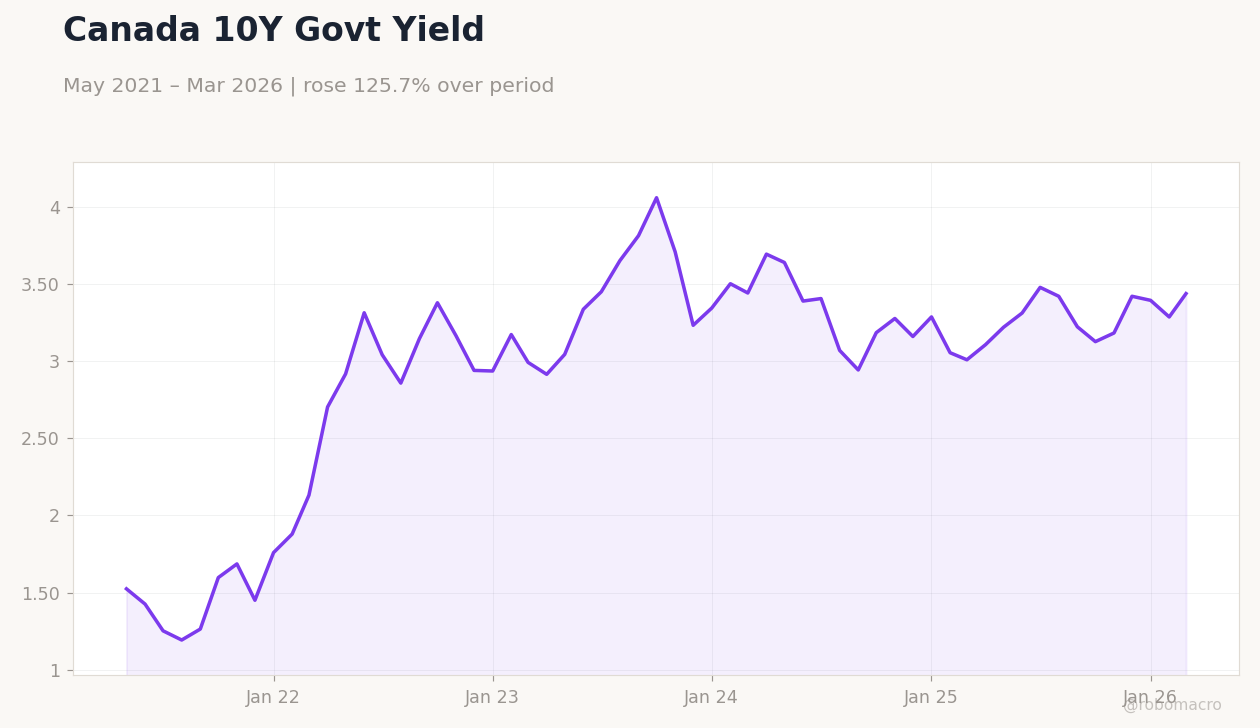

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.80 | 2.50 | 2.40 |

| Core Inflation Rate Year-over-Year | 2.30 | - | 2.50 |

| Inflation Rate Month-over-Month | 0.50 | 1 | 0.90 |

| BoC Business Outlook Survey | - | - | "" |

| BoC Survey of Consumer Expectations | - | - | "" |

WTI Crude Oil Prices | Type: macro_line | WTI USD/bbl: 100.7 (2026-04-13) | Range: 55.44–123.6 | Trend(6pt): 61.45,104.5,83.7,77.27,98.34,100.7

WTI Crude Oil Prices | Type: macro_line | WTI USD/bbl: 100.7 (2026-04-13) | Range: 55.44–123.6 | Trend(6pt): 61.45,104.5,83.7,77.27,98.34,100.7

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-22) | |||

| New Housing Price Index Month-over-Month | 0.30 | 0.20 | 04:30 |

| Friday (2026-04-24) | |||

| Retail Sales Excluding Autos Month-over-Month | 0.80 | 0.80 | 04:30 |

| Retail Sales Month-over-Month Final | 1.10 | 0.90 | 04:30 |

| Retail Sales Month-over-Month Prel | 0.90 | - | 04:30 |

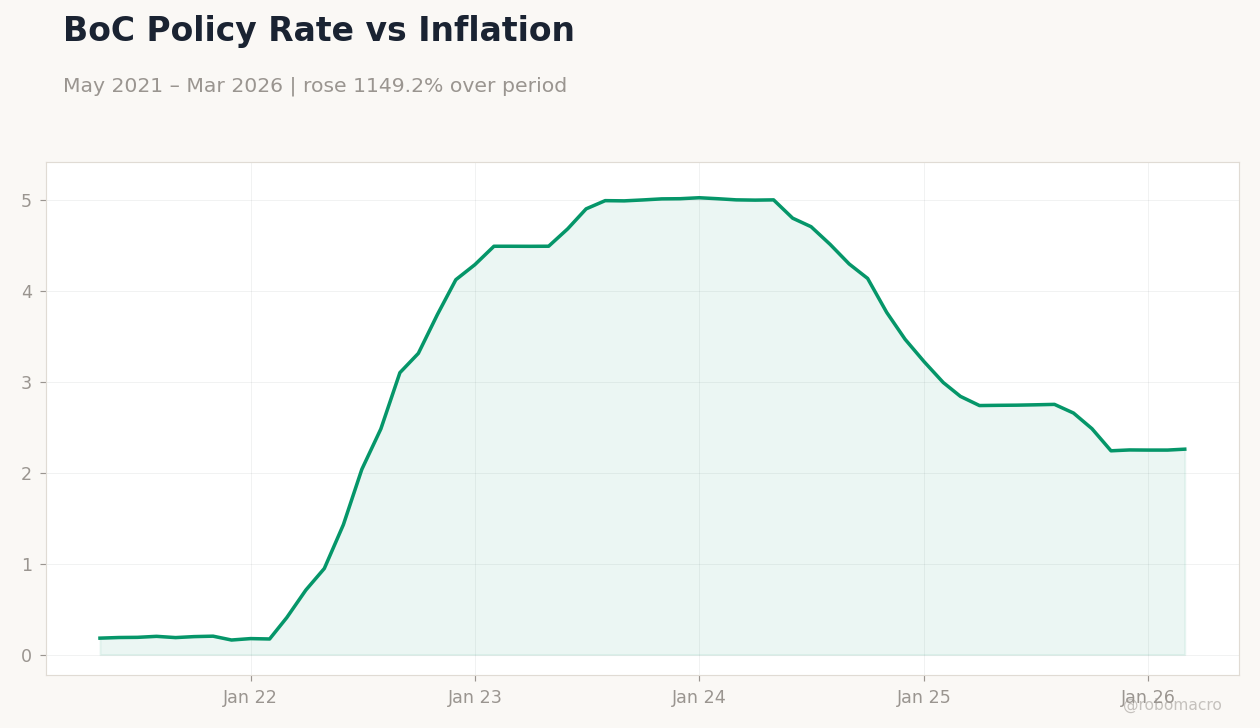

- Canadian inflation climbed to 2.4% YoY in March, slightly missing consensus but driven by energy price spikes from global tensions.

- Bank of Canada named Gosselin and Vincent as deputy governors, emphasizing internal policy focus and continuity.

- Markets mixed: TSX slightly up, CAD stable, yields higher amid inflation data and oil volatility.

Yesterday's Recap

Canadian March inflation data revealed the headline rate rising to 2.4% YoY, just below the 2.5% consensus but up from February's 1.8%, propelled by energy costs linked to Strait of Hormuz disruptions. Core inflation increased to 2.5% YoY from 2.3%, while the monthly rate came in at 0.9%, under the 1% consensus but above February's 0.5%. The Bank of Canada issued its Business Outlook Survey and Survey of Consumer Expectations, indicating ongoing wage pressures and tempered business optimism due to elevated borrowing costs.

Markets showed modest responses: the S&P/TSX closed at 34,360.00 with a +0.04% gain, bolstered by financials yet dragged by energy losses. USD/CAD rose +0.03% to 1.37, and Canada 10Y yields surged +4.61% to 3.44%, signaling expectations for postponed rate cuts. WTI crude declined -2.61% to 87.27 and Brent fell -5.22% to 90.50, despite geopolitical uncertainties.

Gold remained nearly flat at 4,803.30 with a -0.07% change, balancing safe-haven appeal against dollar firmness.

The Day Ahead

Tomorrow features the March New Housing Price Index at 04:30 ET, with consensus for a 0.2% MoM increase from February's 0.3%, which may indicate easing in the housing market. No significant Canadian data releases today, giving markets time to process recent inflation numbers and international oil developments. On Friday, retail sales figures arrive at 04:30 ET, including ex-autos MoM at a consensus of 0.8% and overall MoM final at 0.9%, offering insights into consumer trends.

The BoC has no planned events, though commentary on the new deputy governors could surface. Attention will also turn to US indicators for potential impacts on CAD pairs.

Other Economic Notes

Key themes encompass energy-fueled inflation straining households, with ex-BoC Governor Carney advocating less dependence on US trade amid tariff risks. Housing trends are crucial, as upcoming price index data might underscore affordability issues despite steady sales. Recession odds are estimated at 30% by a former governor, linked to productivity lags and global shocks.