Canada Macro Daily(Beta Mode)

Inflation Misses, Yields Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,912.90 | -0.12% |

| USD/CAD | 1.37 | +0.09% |

| EUR/CAD | 1.60 | +0.18% |

| WTI Crude | 93.85 | -2.09% |

| Natural Gas | 2.68 | +2.45% |

| Gold | 4,730.00 | +0.53% |

| Brent Crude | 97.72 | -7.00% |

| Bitcoin | 78,302.83 | +0.04% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

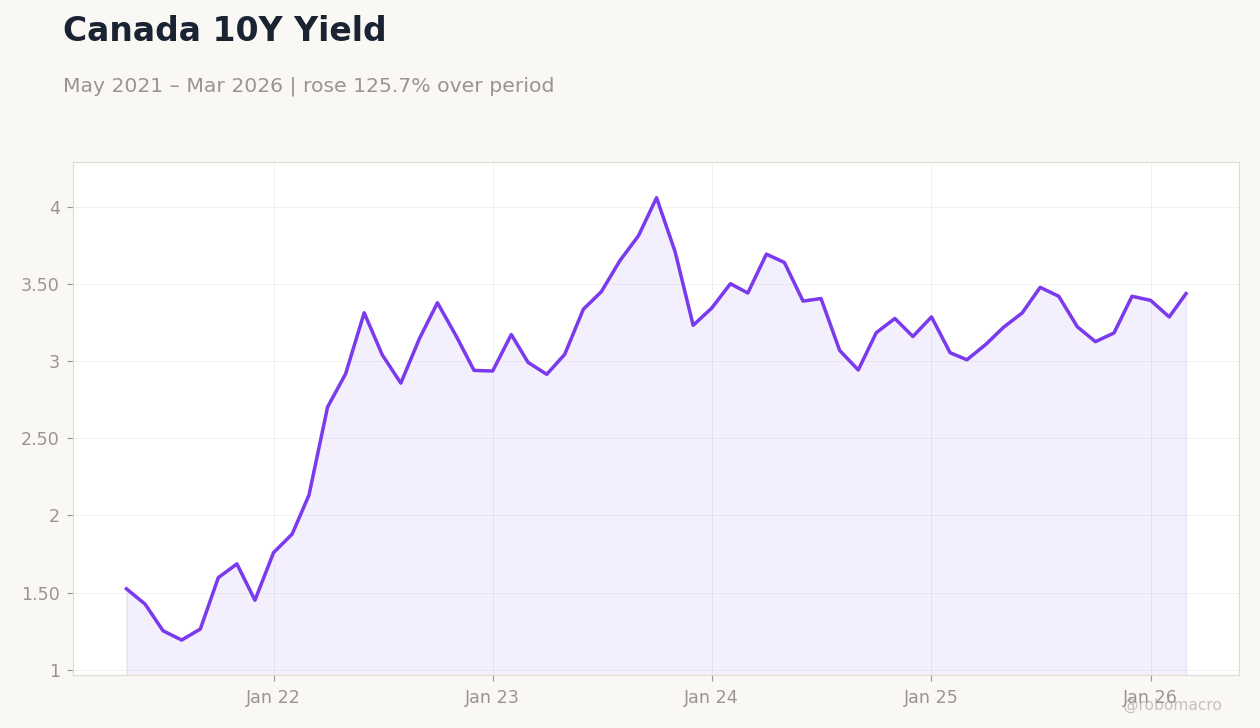

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 1.80 | 2.50 | 2.40 |

| Core Inflation Rate Year-over-Year | 2.30 | - | 2.50 |

| Inflation Rate Month-over-Month | 0.50 | 1 | 0.90 |

| BoC Business Outlook Survey | - | - | "" |

| BoC Survey of Consumer Expectations | - | - | "" |

| New Housing Price Index Month-over-Month | 0.30 | 0.20 | -0.20 |

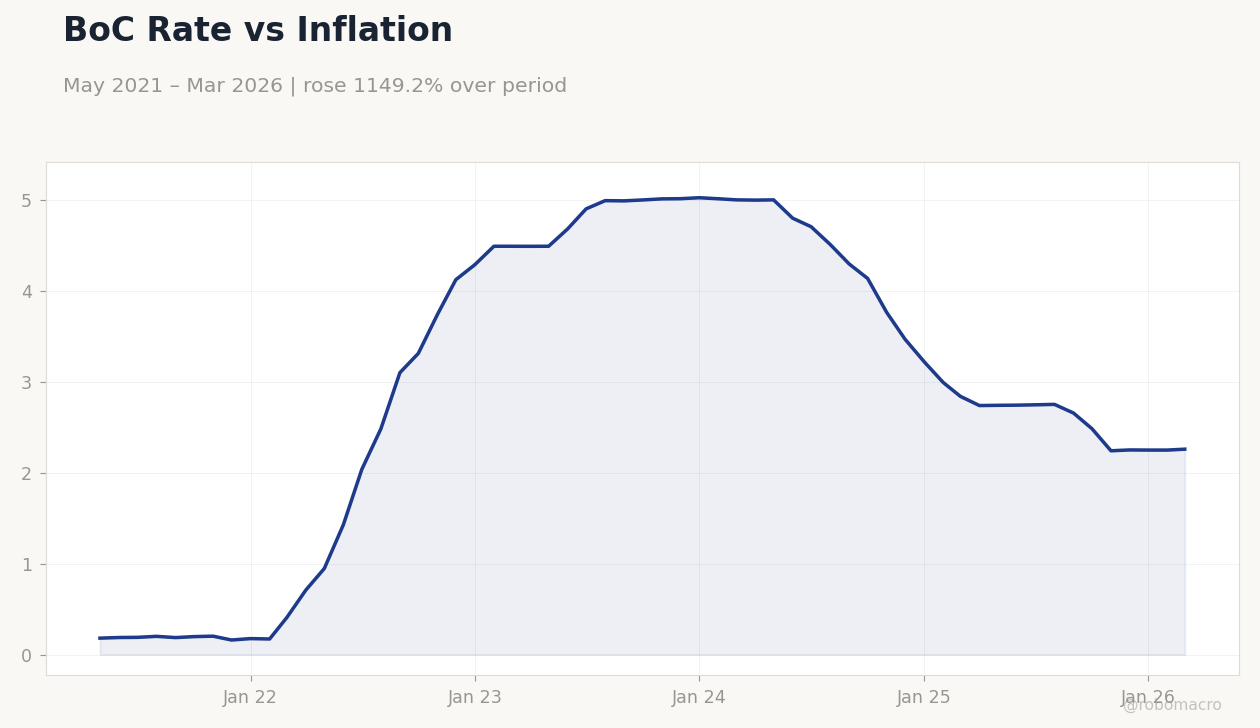

BoC Rate vs Inflation | Type: macro_line | Policy Rate %: 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

BoC Rate vs Inflation | Type: macro_line | Policy Rate %: 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Retail Sales Excluding Autos Month-over-Month | 0.80 | 0.80 | 04:30 |

| Retail Sales Month-over-Month Final | 1.10 | 0.90 | 04:30 |

| Retail Sales Month-over-Month Prel | 0.90 | - | 04:30 |

- Canadian inflation eased to 2.4% YoY, below 2.5% consensus, with core up to 2.5%; housing prices fell 0.2% MoM unexpectedly.

- TSX slipped 0.12% on mixed commodities: WTI down 2.09%, natural gas up 2.45%; CAD weakened vs USD.

- BoC surveys out without surprises; markets await retail sales amid global energy tensions.

Yesterday's Recap

Canadian inflation for March hit 2.4% YoY, missing the 2.5% consensus but above prior 1.8%, led by easing gasoline prices. Core inflation rose to 2.5% YoY from 2.3%, while MoM inflation was 0.9% vs expected 1.0%. New Housing Price Index dropped 0.2% MoM, against forecasts of 0.2% gain and prior 0.3%, indicating real estate cooling.

BoC Business Outlook Survey and Survey of Consumer Expectations released without notable details or market moves. S&P/TSX ended down 0.12% at 33,912.90, dragged by energy as WTI crude fell 2.09% to 93.85 and Brent dropped 7.00% to 97.72. USD/CAD rose 0.09% to 1.37 on USD safe-haven flows; Canada 10Y yields surged 4.61% to 3.44%, signaling bets on sustained rates.

Gold gained 0.53% to 4,730.00 amid volatility.

The Day Ahead

February retail sales due at 4:30 ET, with final MoM consensus at 0.9% after preliminary 0.9%, and ex-autos at 0.8% matching prior. These may shape BoC cut odds if they signal weakening spending under high rates. No events tomorrow, so focus on global data like US PMIs.

CAD pairs could react; strong sales might bolster the loonie vs firm USD. Energy markets sensitive to Middle East news, potentially swaying TSX oil stocks. Data could adjust June cut pricing if softness shows.

Other Economic Notes

Canada faces US trade risks, with Carney advising less US reliance amid tariffs on dairy and autos. Housing weakness, via price index decline, flags builder caution and prairie correction risks. RBC warned on salmon investments, reigniting debates; Quebec economists joined BoC circle, possibly adding views.

Stock tips highlight buys before BoC updates, while energy notes gasoline-driven inflation dip.

Global Macro News

Middle East tensions, including Hormuz risks and Iran war effects, lifted USD safe-haven demand, pressuring CAD despite oil gains. US Fed rate cut signals on stalling growth initially eased Canadian yields, but 10Y jump to 3.44% shows policy divergence. Producer prices rose from conflicts, aiding USD and offsetting CAD oil support.

(cont...)