Canada Macro Daily(Beta Mode)

BoC Hold Looms, GDP Beats

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,904.10 | -0.03% |

| USD/CAD | 1.36 | -0.62% |

| EUR/CAD | 1.60 | -0.13% |

| WTI Crude | 94.67 | +0.29% |

| Natural Gas | 2.75 | +9.08% |

| Gold | 4,720.80 | -0.03% |

| Brent Crude | 99.66 | -5.38% |

| Bitcoin | 77,816.02 | -1.07% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

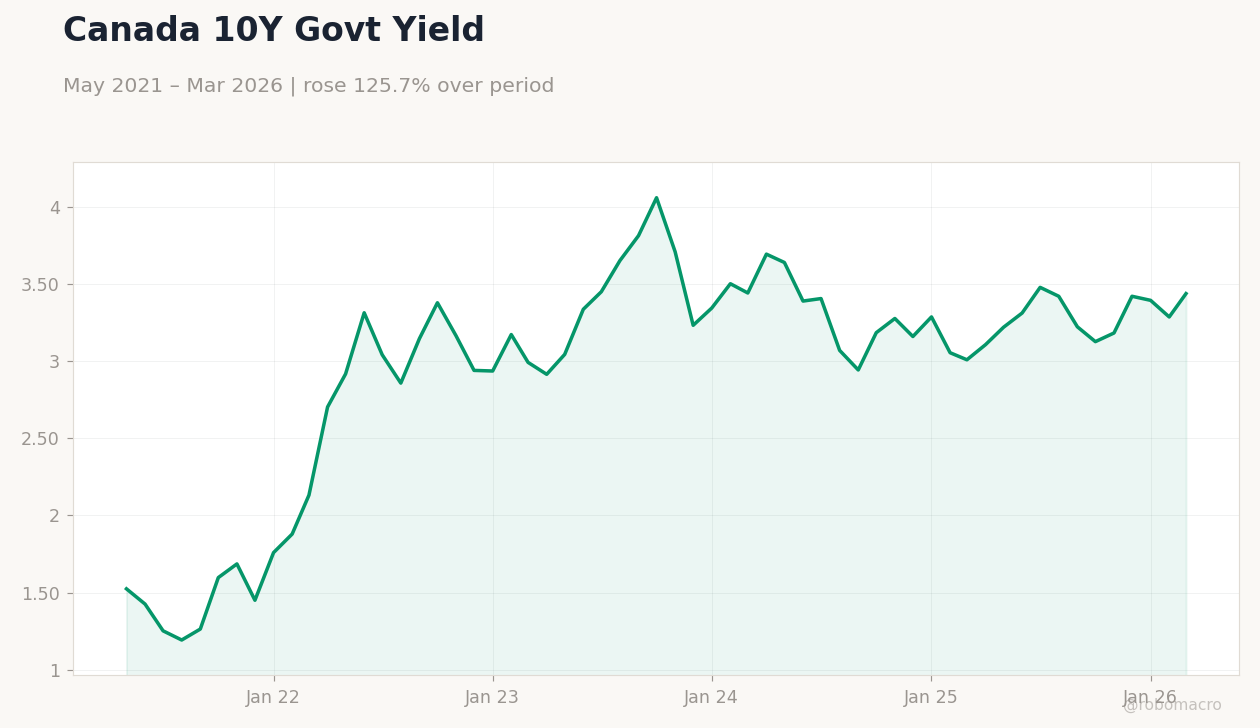

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

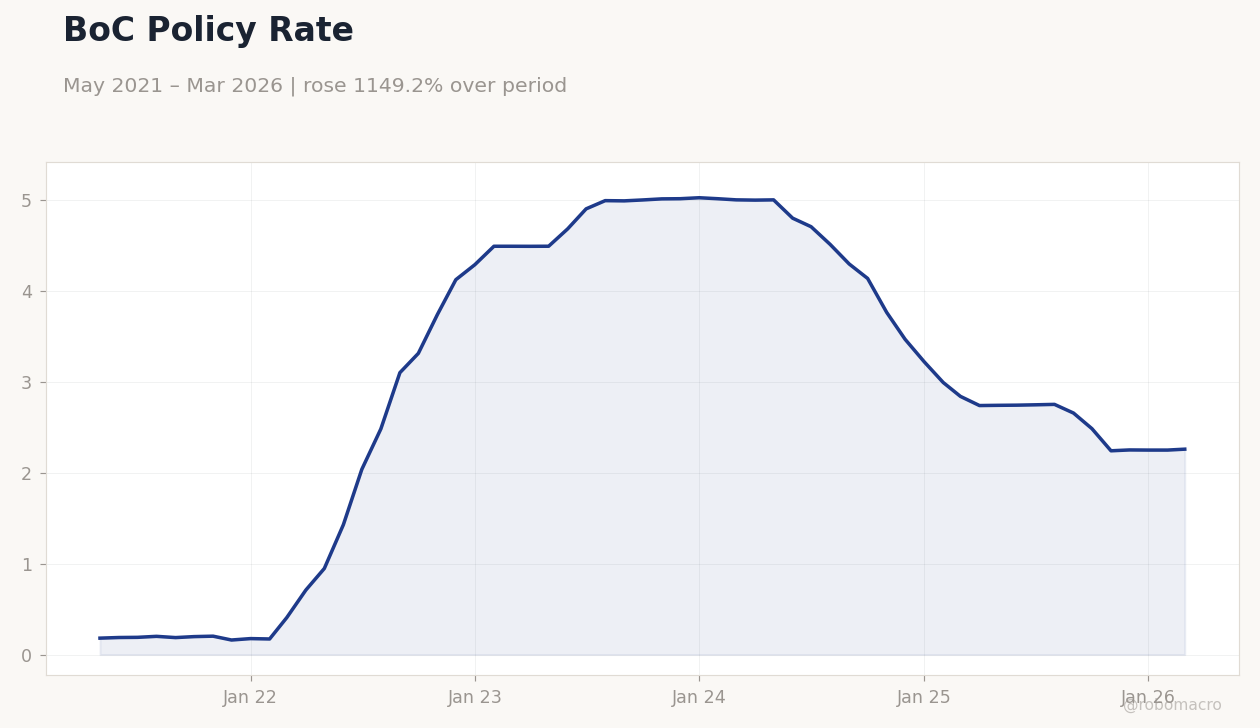

BoC Policy Rate | Type: macro_line | Policy Rate %: 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

BoC Policy Rate | Type: macro_line | Policy Rate %: 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-04-29) | |||

| BoC Interest Rate Decision | 2.25 | 2.25 | 05:45 |

| BoC Monetary Policy Report | - | - | 05:45 |

| BoC Press Conference | - | - | 06:30 |

| Thursday (2026-04-30) | |||

| GDP Month-over-Month | 0.10 | 0.20 | 04:30 |

| GDP Month-over-Month Prel | - | - | 04:30 |

- Bank of Canada expected to maintain rates at 2.25% amid oil-driven inflation pressures.

- Canadian GDP surprises higher, supporting CAD strength on resilient oil prices.

- Markets mixed with TSX flat, yields rising, and energy commodities volatile.

Yesterday's Recap

Canadian markets showed resilience yesterday with the S&P/TSX closing at 33,904.10, down a marginal 0.03% amid mixed sector performance. USD/CAD fell 0.62% to 1.36, bolstered by advancing oil prices despite global demand concerns. Canada 10Y government yields climbed 4.61% to 3.44%, reflecting inflation expectations from energy shocks, while the 2Y yield rose 0.44% to 2.26%.

WTI Crude gained 0.29% to 94.67, but Brent Crude dropped 5.38% to 99.66, highlighting divergent supply dynamics. Natural Gas surged 9.08% to 2.75 on demand forecasts, aiding energy-linked equities. Gold held steady at 4,720.80 with a 0.03% dip, and Bitcoin declined 1.07% to 77,816.02 amid broader risk aversion.

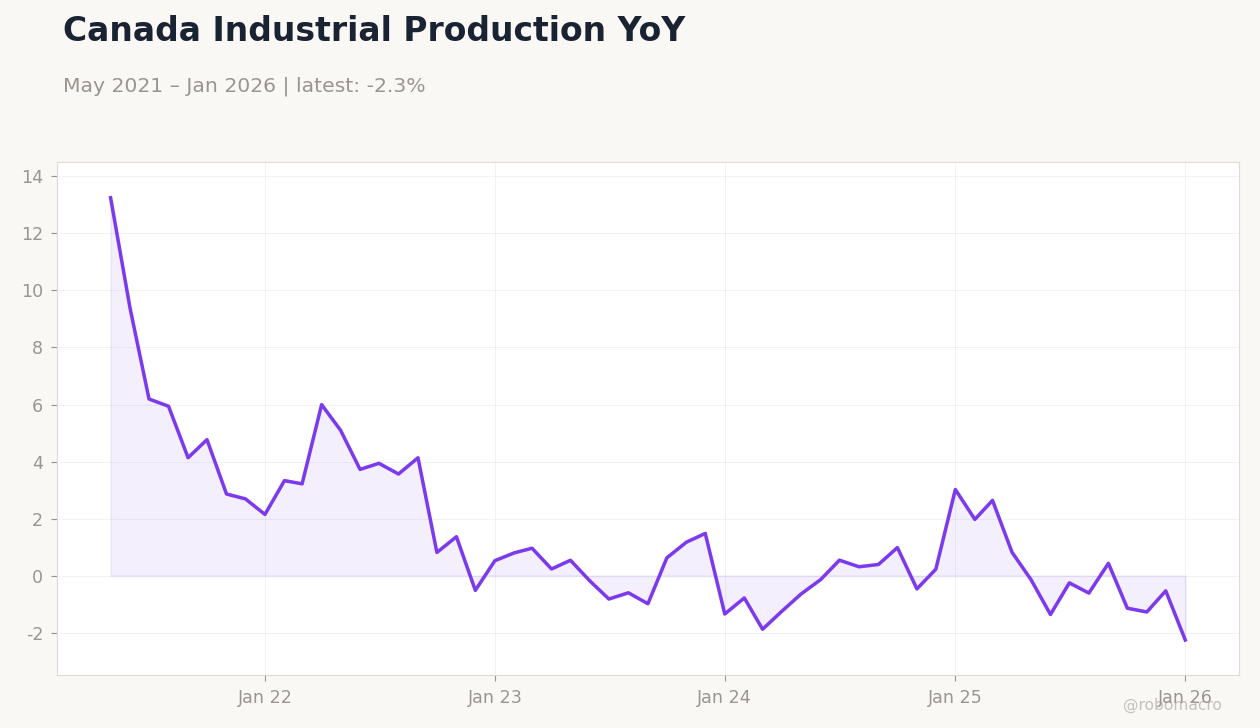

Recent GDP data edged higher than forecasts, beating consensus and easing recession worries, though no major data releases occurred yesterday.

The Day Ahead

Attention turns to Wednesday's Bank of Canada interest rate decision at 05:45 ET, with consensus expecting a hold at 2.25% amid war-driven inflation. The BoC Monetary Policy Report, released concurrently, will provide updated economic projections and inflation outlooks. A press conference at 06:30 ET follows, where Governor Macklem may elaborate on forward guidance.

Thursday brings GDP month-over-month at 04:30 ET, with consensus at 0.2% following the prior 0.1%. Preliminary GDP figures will also emerge, offering early insights into Q2 momentum. These events could sway CAD crosses and bond yields significantly.

Other Economic Notes

Broader themes include persistent energy price volatility, with stalled US-Iran talks boosting oil and supporting CAD resilience. US tariff threats on Canadian autos, as highlighted by Carney, underscore the need for diversified trade to mitigate economic reliance. Housing affordability strains continue, though recent sales upticks signal modest recovery amid high rates.

Global Macro News

Global oil prices jumped as US-Iran peace talks stalled, directly benefiting Canada's energy exports and pressuring inflation metrics. (cont...)