Canada Macro Daily(Beta Mode)

BoC Holds Amid Oil, Trade Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,318.40 | -0.79% |

| USD/CAD | 1.37 | -0.15% |

| EUR/CAD | 1.60 | +0.38% |

| WTI Crude | 103.81 | -2.87% |

| Natural Gas | 2.62 | -1.06% |

| Gold | 4,650.40 | +2.31% |

| Brent Crude | 100.85 | -14.56% |

| Bitcoin | 76,077.04 | +0.40% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

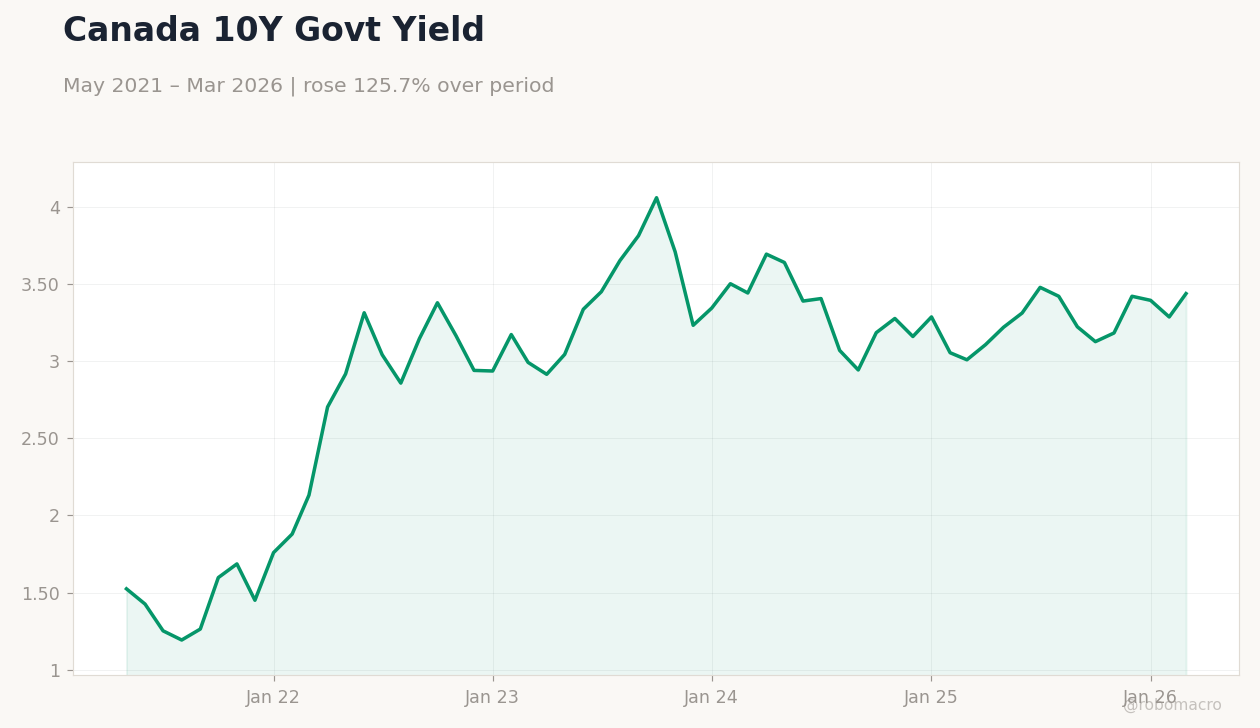

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

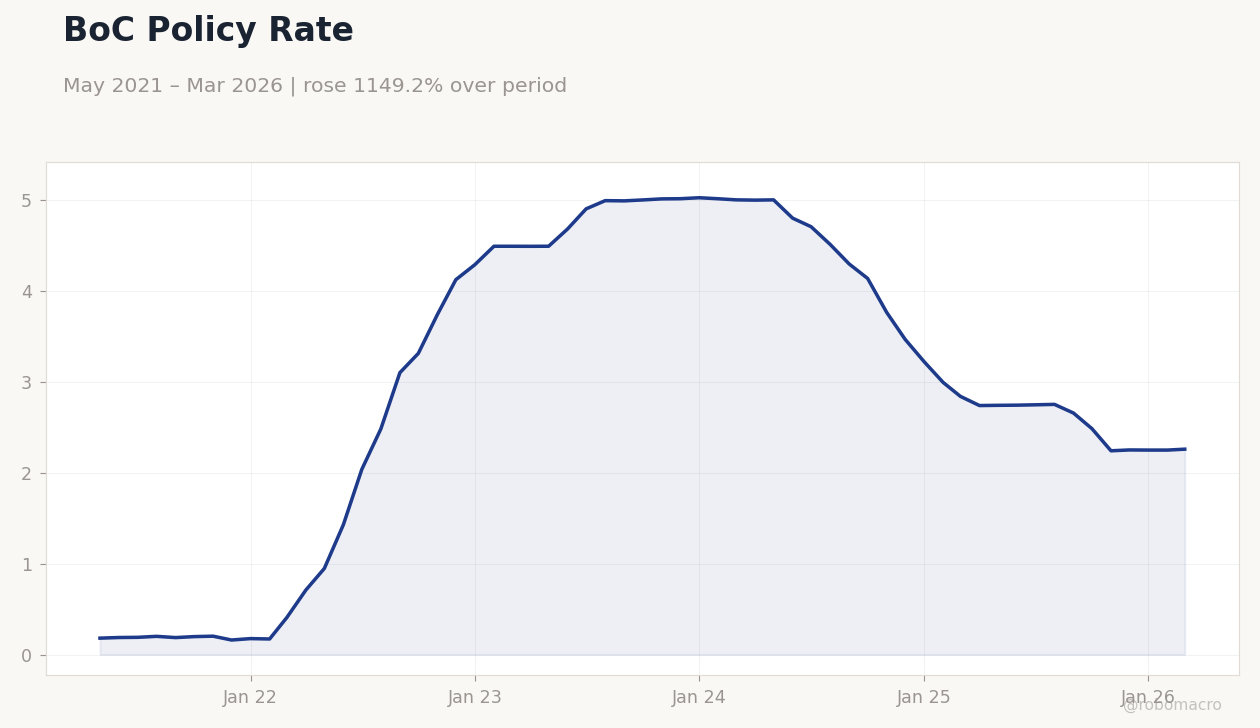

| BoC Interest Rate Decision | 2.25 | 2.25 | 2.25 |

| BoC Monetary Policy Report | - | - | - |

| BoC Press Conference | - | - | - |

BoC Policy Rate | Type: macro_line | Short-term Interest Rate (%): 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

BoC Policy Rate | Type: macro_line | Short-term Interest Rate (%): 2.26 (2026-03-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1809,2.037,4.992,3.765,2.25,2.26

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Month-over-Month | 0.10 | 0.20 | 04:30 |

| GDP Month-over-Month Prel | 0.20 | - | 04:30 |

- Bank of Canada maintains key rate at 2.25%, citing balanced risks from oil shocks and trade tensions.

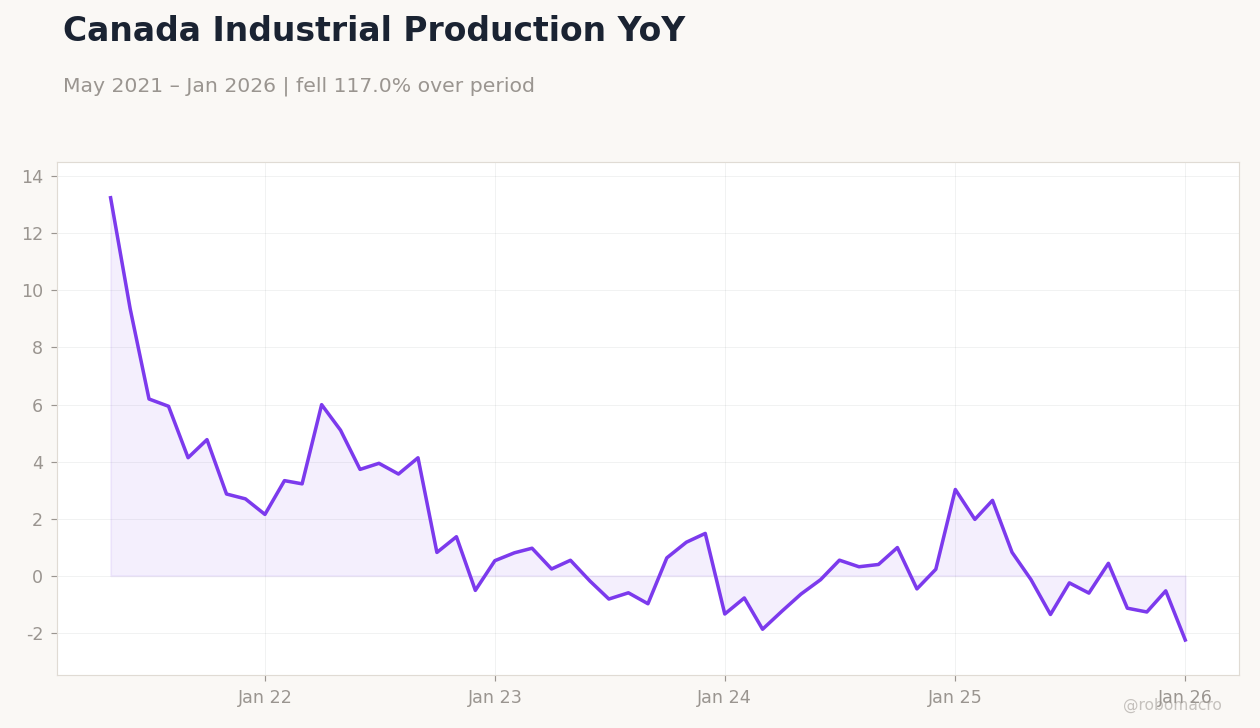

- Housing slump and potential condo glut weigh on growth outlook in Monetary Policy Report.

- Markets mixed: TSX dips 0.79%, CAD strengthens slightly, yields rise on rate hold.

Yesterday's Recap

The Bank of Canada held its key interest rate steady at 2.25%, aligning with consensus expectations, as the Governing Council emphasized a patient approach amid evolving economic risks. The Monetary Policy Report highlighted a downgrade to housing activity, warning of a small condo glut that could curb overall growth. During the press conference, officials noted that high oil prices might necessitate future rate hikes to combat inflation, while U.S.

trade uncertainties could prompt cuts. Canadian equities softened, with the S&P/TSX closing down 0.79% at 33,318.40, pressured by energy sector declines amid falling crude prices. USD/CAD edged lower by 0.15% to 1.37, supported by CAD resilience despite global oil volatility, while EUR/CAD rose 0.38% to 1.60.

Government bond yields climbed, with the 10-year up 4.61% to 3.44% and the 2-year up 0.44% to 2.26%, reflecting diminished expectations for near-term easing. Commodity moves were stark, with WTI crude dropping 2.87% to 103.81 and Brent plunging 14.56% to 100.85, offsetting gold's 2.31% gain to 4,650.40.

The Day Ahead

Attention turns to the 4:30 ET release of March GDP month-over-month, with consensus at 0.2% following February's 0.1%, potentially signaling continued economic resilience if it beats estimates. A preliminary GDP month-over-month figure will also be reported, building on the prior 0.2%, offering early insights into Q1 momentum. These data points could influence Bank of Canada rate expectations, especially if they indicate softening growth amid housing weakness.

No major events are scheduled for tomorrow, keeping focus on today's releases for CAD and TSX direction. Markets may also watch for any spillover from global oil dynamics, given Canada's energy exposure.

Other Economic Notes

Broader themes include persistent housing market challenges, with the Bank of Canada noting muted activity that could drag on GDP growth. Energy sector volatility remains a key driver, as elevated oil prices from geopolitical tensions support exports but risk fueling inflation. Trade relations with the U.S.

add uncertainty, potentially impacting manufacturing and investment.