Canada Macro Daily(Beta Mode)

Trade Surplus Beats, Oil Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,566.90 | -0.21% |

| USD/CAD | 1.36 | +0.24% |

| EUR/CAD | 1.60 | +0.64% |

| WTI Crude | 90.40 | -11.61% |

| Natural Gas | 2.71 | -2.83% |

| Gold | 4,717.40 | +3.55% |

| Brent Crude | 98.08 | -10.73% |

| Bitcoin | 82,713.15 | +2.21% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoC Macklem Speech | - | - | - |

| BoC Rogers Speech | - | - | - |

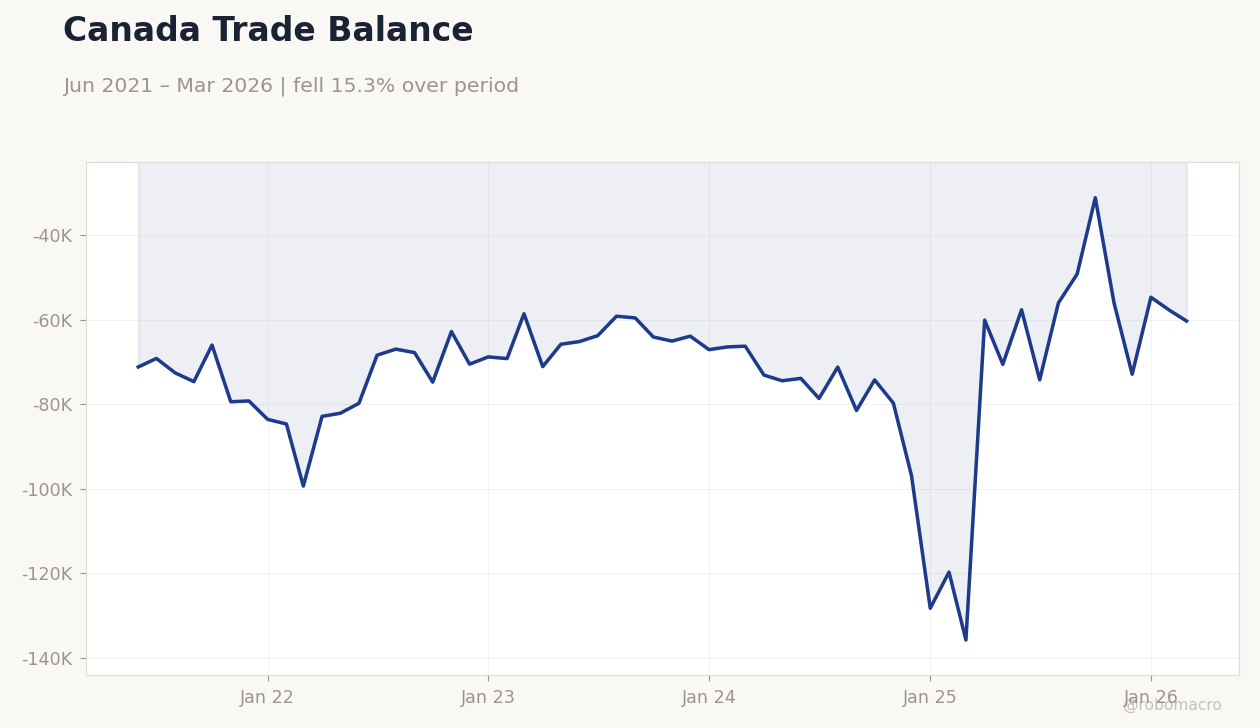

| Trade Balance | -5,110m | -2,900m | 1,780m |

Canada Trade Balance | Type: macro_line | Trade Balance (CAD): -6.031e+04 (2026-03-01) | Range: -1.359e+05–-3.11e+04 | Trend(6pt): -7.119e+04,-6.696e+04,-6.41e+04,-9.695e+04,-5.778e+04,-6.031e+04

Canada Trade Balance | Type: macro_line | Trade Balance (CAD): -6.031e+04 (2026-03-01) | Range: -1.359e+05–-3.11e+04 | Trend(6pt): -7.119e+04,-6.696e+04,-6.41e+04,-9.695e+04,-5.778e+04,-6.031e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ivey PMI Seasonally Adjusted | 49.70 | 49.90 | 06:00 |

| Friday (2026-05-08) | |||

| Headline Unemployment Rate | 6.70 | 6.70 | 04:30 |

| Employment Change | 14,100 | 20,000 | 04:30 |

| Full-Time Employment Change | -1,100 | - | 04:30 |

| Labor Force Participation | 64.90 | - | 04:30 |

| Part-Time Employment Change | 15,200 | - | 04:30 |

- Canada's trade balance swung to a surprise surplus of C$1.78 billion in March, beating consensus expectations amid stronger exports.

- Bank of Canada officials Macklem and Rogers delivered speeches, emphasizing vigilance on inflation and housing amid oil price volatility.

- Markets reacted with TSX dipping 0.21%, CAD weakening, and bond yields rising as oil prices fell sharply on Middle East peace hopes.

Yesterday's Recap

Canada's March trade balance surprised with a C$1.78 billion surplus, far exceeding the consensus forecast of a C$2.9 billion deficit and reversing the prior C$5.11 billion shortfall, driven by robust energy exports despite global volatility. The S&P/TSX Composite closed at 33,566.90, down 0.21%, as energy sector losses offset gains in financials. USD/CAD rose 0.24% to 1.36, reflecting CAD weakness from falling oil prices, while EUR/CAD climbed 0.64% to 1.60.

WTI Crude plunged 11.61% to $90.40 and Brent Crude dropped 10.73% to $98.08, pressured by hopes for Middle East de-escalation. Natural Gas fell 2.83% to $2.71, adding to commodity headwinds. Canada 10-year government bond yields surged 4.61% to 3.44%, signaling reduced rate-cut bets, while the 2-year yield edged up 0.44% to 2.26%.

Gold rallied 3.55% to $4,717.40 as a safe haven, and Bitcoin gained 2.21% to $82,713.15 amid broader risk sentiment.

The Day Ahead

Today's key release is the April Ivey PMI seasonally adjusted at 6:00 ET, with consensus at 49.9 following March's 49.7, potentially signaling manufacturing sentiment amid trade improvements. Markets will watch for any expansion above 50, which could bolster CAD and TSX equities. No events are scheduled for tomorrow, providing a brief respite before Friday's labor data.

Friday brings the headline unemployment rate at 4:30 ET, consensus steady at 6.7% from previous 6.7%, alongside employment change expected at 20,000 versus prior 14,100. Full-time and part-time employment changes, plus labor force participation at 64.9% previously, will offer insights into job market resilience. These figures could influence Bank of Canada rate expectations, especially if they indicate cooling wage pressures.

Other Economic Notes

Broader themes highlight Canada's uneven trade outlook, with the surprise surplus underscoring export strength in energy but vulnerability to oil price swings from geopolitical tensions. Housing markets remain hot, as noted in BoC monitoring, with early warning signs amid rate stability potentially fueling affordability concerns. Innovation in payments, like Visa and Wealthsimple's stablecoin pilot, points to evolving financial infrastructure that could enhance cross-border efficiency.