Canada Macro Daily(Beta Mode)

PMI Surges, Trade Swings to Surplus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,981.80 | +1.24% |

| USD/CAD | 1.36 | +0.17% |

| EUR/CAD | 1.59 | +0.09% |

| WTI Crude | 91.69 | -3.57% |

| Natural Gas | 2.72 | -0.48% |

| Gold | 4,741.90 | +1.28% |

| Brent Crude | 97.91 | -3.32% |

| Bitcoin | 80,975.43 | -0.56% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

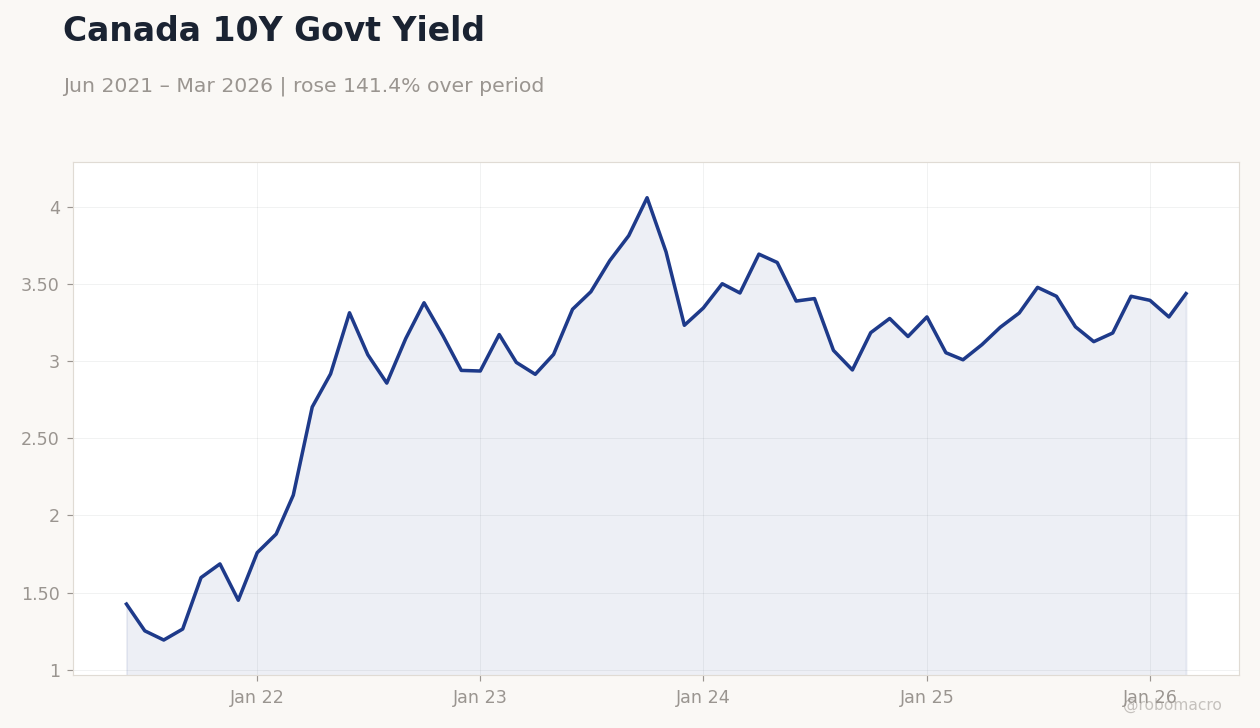

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoC Macklem Speech | - | - | - |

| BoC Rogers Speech | - | - | - |

| Trade Balance | -5,110m | -2,900m | 1,780m |

| Ivey PMI Seasonally Adjusted | 49.70 | 49.90 | 57.70 |

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.44 (2026-03-01) | Range: 1.192–4.062 | Trend(6pt): 1.425,2.859,4.062,3.162,3.288,3.44

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.44 (2026-03-01) | Range: 1.192–4.062 | Trend(6pt): 1.425,2.859,4.062,3.162,3.288,3.44

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-08) | |||

| Headline Unemployment Rate | 6.70 | 6.70 | 04:30 |

| Employment Change | 14,100 | 20,000 | 04:30 |

| Full-Time Employment Change | -1,100 | - | 04:30 |

| Labor Force Participation | 64.90 | - | 04:30 |

| Part-Time Employment Change | 15,200 | - | 04:30 |

- Ivey PMI jumped to 57.7 in April, beating consensus of 49.9 and signaling business expansion.

- March trade balance posted C$1.78 billion surplus, far above expected C$-2.9 billion deficit.

- TSX rose 1.24% on energy gains; CAD edged weaker despite data beats.

Yesterday's Recap

Canada's Ivey PMI for April rose sharply to 57.7 from 49.7, exceeding the consensus of 49.9 and indicating expansion in business activity. The March trade balance shifted to a C$1.78 billion surplus, against a forecasted C$-2.9 billion deficit and prior C$-5.11 billion, boosted by strong exports in energy and machinery. This supports Q1 GDP outlook.

S&P/TSX Composite advanced 1.24% to 33,981.80, driven by energy and materials sectors amid oil volatility. USD/CAD increased 0.17% to 1.36, and EUR/CAD rose 0.09% to 1.59, showing slight CAD softening on global flows. Canada 10-year government yield climbed 4.61% to 3.44%, aligning with U.S.

moves and central bank signals. WTI crude declined 3.57% to 91.69, weighed by Middle East peace hopes, while gold gained 1.28% to 4,741.90 on safe-haven buying. Natural gas fell 0.48% to 2.72, and Bitcoin dropped 0.56% to 80,975.43.

Earlier BoC speeches by Macklem and Rogers occurred, focusing on policy framework.

The Day Ahead

No major events today. Friday's labor data includes headline unemployment rate expected at 6.7%, matching prior, and employment change forecasted at 20,000. Full-time employment may improve from prior -1,100, with part-time from 15,200 and labor force participation from 64.9%.

These metrics could shape BoC easing views, especially alongside recent PMI and trade strength. Stronger jobs might firm yields and CAD.

Other Economic Notes

Canada's GDP showed steady growth in February, led by manufacturing, despite housing weakness. The critical minerals sector is re-rating due to structural demand shifts, aiding resource stocks. ESG efforts, such as Lactalis Canada's 2025 report, highlight industry collaboration for sustainable growth.

Bank of Canada notes shifting maritime trade positions, potentially impacting exports. These factors point to economic resilience amid global changes.