Canada Macro Daily(Beta Mode)

BoC Survey Out, Yields Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,290.73 | +0.44% |

| USD/CAD | 1.37 | +0.14% |

| EUR/CAD | 1.61 | -0.23% |

| WTI Crude | 101.93 | +3.94% |

| Natural Gas | 2.83 | -2.78% |

| Gold | 4,724.70 | +0.13% |

| Brent Crude | 107.24 | +2.91% |

| Bitcoin | 80,450.36 | -1.56% |

| Canada 2Y Govt Yield | 2.26% | +0.44% |

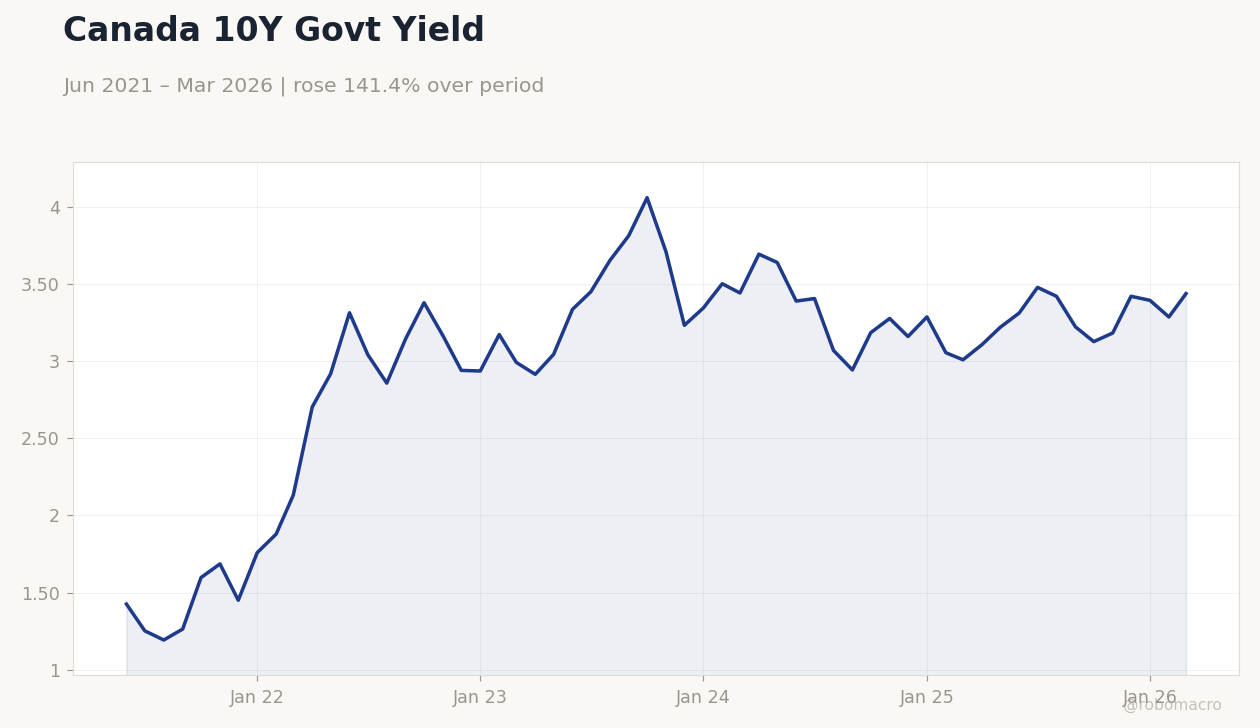

| Canada 10Y Govt Yield | 3.44% | +4.61% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoC Market Participants Survey | - | - | "" |

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.44 (2026-03-01) | Range: 1.192–4.062 | Trend(6pt): 1.425,2.859,4.062,3.162,3.288,3.44

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.44 (2026-03-01) | Range: 1.192–4.062 | Trend(6pt): 1.425,2.859,4.062,3.162,3.288,3.44

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-15) | |||

| Housing Starts Level | 235,900 | 242,500 | 08:15 |

| Tuesday (2026-05-19) | |||

| Inflation Rate Year-over-Year | 2.40 | - | 08:30 |

| Core Inflation Rate Year-over-Year | 2.50 | - | 08:30 |

| Inflation Rate Month-over-Month | 0.90 | - | 08:30 |

| New Housing Price Index Month-over-Month | -0.20 | - | 08:30 |

- BoC Market Participants Survey shows mixed views on economy and policy.

- TSX up modestly on energy strength; CAD softens vs USD.

- Oil prices jump, lifting commodity sectors amid global tensions.

Yesterday's Recap

The Bank of Canada released its quarterly Market Participants Survey on May 11 at 10:30 ET, compiling insights from financial market participants on economic conditions and outlook, with no specific consensus or actual data reported. Canadian stocks rose slightly, as the S&P/TSX Composite ended at 34,290.73, gaining 0.44%, supported by energy firms on higher oil prices. USD/CAD increased 0.14% to 1.37, pressured by a stronger U.S.

dollar, while EUR/CAD fell 0.23% to 1.61. Bond yields advanced, with the Canada 10Y yield up 4.61% to 3.44% and the 2Y yield rising 0.44% to 2.26%, reflecting adjusted rate bets. WTI Crude climbed 3.94% to 101.93, and Brent Crude gained 2.91% to 107.24, driven by supply worries.

Natural Gas dropped 2.78% to 2.83, Gold rose 0.13% to 4,724.70, and Bitcoin fell 1.56% to 80,450.36.

The Day Ahead

No significant Canadian economic data is set for May 12, offering a lull after the prior day's survey. Focus turns to later releases, including Housing Starts on May 15 at 08:15 ET, forecasted at 242,500 against a previous 235,900. On May 19 at 08:30 ET, inflation figures are due: YoY Inflation Rate after 2.4% prior, Core Inflation YoY following 2.5%, MoM Inflation after 0.9%, and New Housing Price Index MoM succeeding -0.2%.

Markets could react to international developments, affecting CAD pairs and equity mood. No BoC events or statements are planned today.

Other Economic Notes

Ongoing Canadian themes feature housing sector strains, highlighted by forthcoming starts and price data amid high interest rates. Energy markets are key, with oil fluctuations aiding exports but complicating inflation management. U.S.-Canada trade talks on dairy and autos persist without progress, which may influence manufacturing and exchange rates.

Global Macro News

Oil benchmarks advanced sharply, with WTI and Brent rises enhancing Canada's export position and bolstering TSX energy shares. U.S.-Iran frictions, per reports, fueled crude gains, indirectly aiding CAD via commodities despite USD strength. Declines in PFAS chemicals in Canadian seabird eggs signal regulatory progress, possibly shaping resource policies.

<i>↓ p.2</i>