Canada Macro Daily(Beta Mode)

Inflation Data Looms Over CAD Weakness

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,833.40 | -1.27% |

| USD/CAD | 1.37 | +0.14% |

| EUR/CAD | 1.60 | +0.00% |

| WTI Crude | 102.41 | -2.86% |

| Natural Gas | 3.04 | +2.64% |

| Gold | 4,540.20 | -0.34% |

| Brent Crude | 110.61 | +1.24% |

| Bitcoin | 77,118.39 | -0.40% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

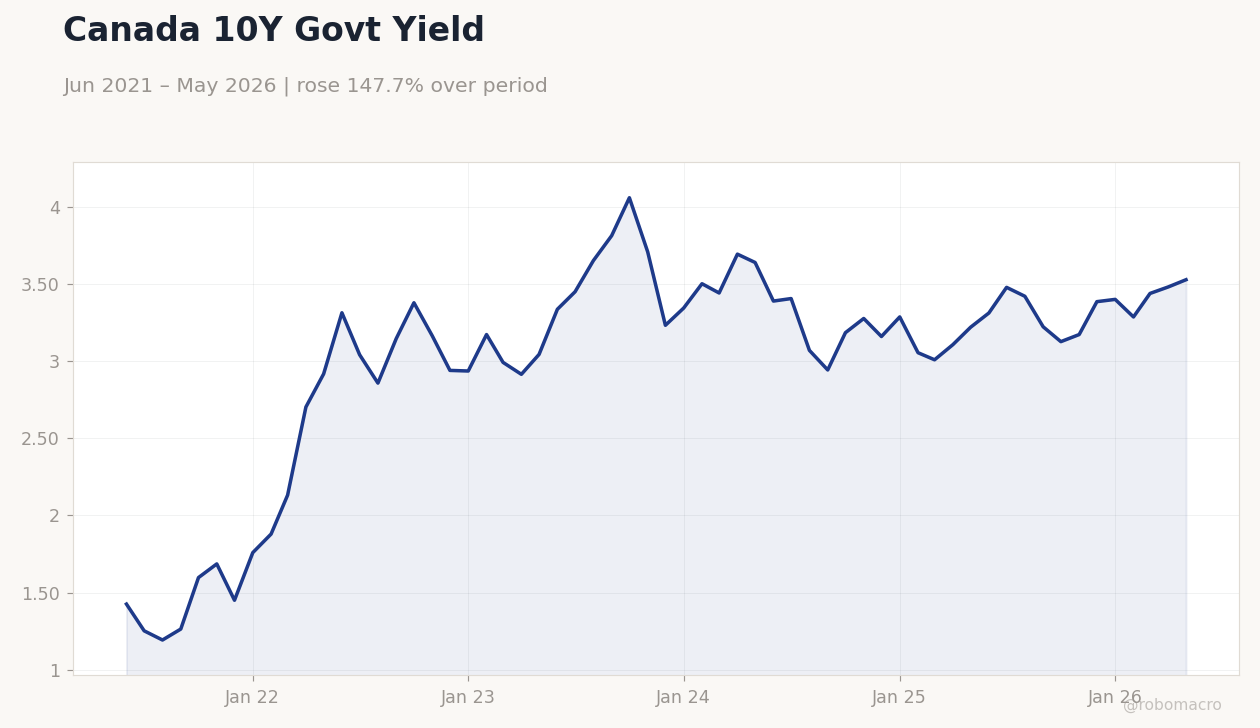

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Canada 10Y Govt Yield | Type: macro_line | Yield %: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Canada 10Y Govt Yield | Type: macro_line | Yield %: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-05-19) | |||

| Inflation Rate Year-over-Year | 2.40 | - | 04:30 |

| Core Inflation Rate Year-over-Year | 2.50 | - | 04:30 |

| Inflation Rate Month-over-Month | 0.90 | - | 04:30 |

| New Housing Price Index Month-over-Month | -0.20 | - | 04:30 |

| Friday (2026-05-22) | |||

| Retail Sales Excluding Autos Month-over-Month | 0.50 | - | 04:30 |

| Retail Sales Month-over-Month Final | 0.70 | - | 04:30 |

| Retail Sales Month-over-Month Prel | - | - | 04:30 |

- Key Canadian inflation data due tomorrow could shift BoC cut odds

- S&P/TSX falls 1.27% while USD/CAD rises to 1.37 on USD strength

- BoC holds policy rate at 2.25% and flags inflation sensitivity

Yesterday's Recap

Canadian markets closed lower with the S&P/TSX dropping 1.27% to 33,833.40 as energy and materials weighed on sentiment. USD/CAD advanced 0.14% to 1.37, extending its recent climb against a firmer greenback. WTI Crude declined 2.86% to 102.41 while Natural Gas rose 2.64% to 3.04.

Gold eased 0.34% to 4,540.20. The Canada 2-year yield fell 0.20% to 2.25% but the 10-year yield climbed 1.34% to 3.53%. No major economic releases occurred on May 17, leaving price action driven by global risk sentiment and commodity swings.

CAD losses remained contained by supportive oil prices.

The Day Ahead

Markets will focus on the May 19 inflation release at 04:30 ET. The CPI year-over-year print, core measure, month-over-month change and New Housing Price Index will arrive together. A hotter-than-expected outcome would reduce June cut probabilities and lift front-end yields.

Retail sales data scheduled for May 22 will follow, offering insight into consumer resilience. USD/CAD and Government of Canada bonds will likely see the largest moves.

Other Economic Notes

Oil-sands output rose faster than expected in Alberta and Saskatchewan, supporting export revenues. CMHC housing starts declined to 225k annualized, confirming a gradual cooling in residential construction. Ottawa extended the temporary tariff rebate on U.S.

steel imports through Q3, easing cost pressures for domestic manufacturers. Infrastructure spending continues to underpin select TSX sectors despite higher borrowing costs. Broader growth remains anchored by energy exports amid global supply concerns.

Global Macro News

U.S. dollar strength pushed several commodity currencies lower, including the Canadian dollar near one-month lows. Rising oil prices provided partial support for CAD but failed to reverse the broader USD/CAD uptrend.

Global risk-off flows lifted safe-haven demand and pressured equities outside North America. Fed policy expectations and potential U.S. tariff adjustments continue to influence cross-border capital flows.

<i>↓ p.2</i>