Canada Macro Daily(Beta Mode)

Soft CPI Miss Eases BoC Hike Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 33,741.20 | -0.27% |

| USD/CAD | 1.38 | +0.12% |

| EUR/CAD | 1.60 | -0.31% |

| WTI Crude | 102.08 | -5.28% |

| Natural Gas | 3.11 | -0.13% |

| Gold | 4,502.30 | -0.09% |

| Brent Crude | 108.69 | -2.33% |

| Bitcoin | 77,346.60 | +0.78% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.40 | 3.10 | 2.80 |

| Core Inflation Rate Year-over-Year | 2.50 | - | 2.10 |

| Inflation Rate Month-over-Month | 0.90 | 0.70 | 0.40 |

| New Housing Price Index Month-over-Month | -0.20 | 0 | -0.40 |

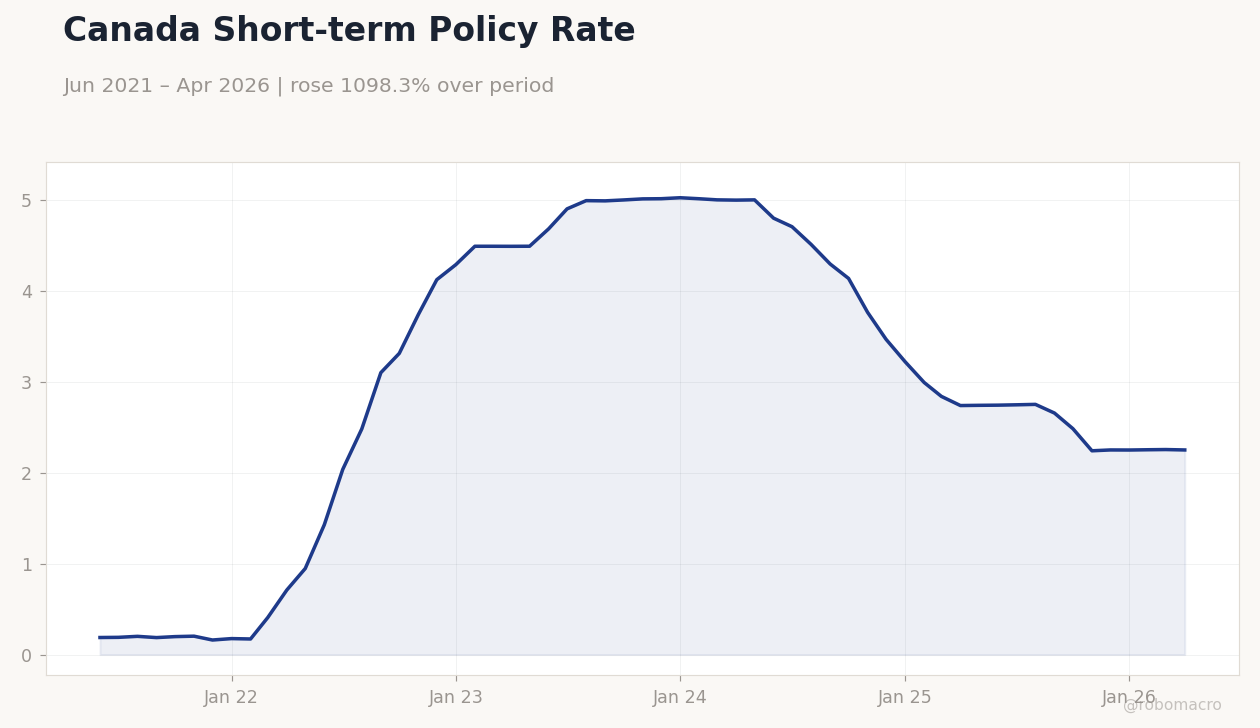

Canada Short-term Policy Rate | Type: macro_line | %: 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1879,2.483,5.002,3.469,2.254,2.251

Canada Short-term Policy Rate | Type: macro_line | %: 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1879,2.483,5.002,3.469,2.254,2.251

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-05-22) | |||

| Retail Sales Excluding Autos Month-over-Month | 0.50 | 0.90 | 04:30 |

| Retail Sales Month-over-Month Final | 0.70 | 0.60 | 04:30 |

| Retail Sales Month-over-Month Prel | - | - | 04:30 |

| Senior Loan Officer Survey | - | - | 06:30 |

- Canada April CPI rises 2.8% y/y, below 3.1% consensus

- CAD slips to five-week low as hike odds fade

- TSX declines 0.27% while WTI crude drops 5.28%

Yesterday's Recap

Statistics Canada released April inflation figures showing the headline CPI at 2.8% y/y against a 3.1% consensus, while core CPI printed at 2.1% y/y. The month-over-month rate came in at 0.4%, missing forecasts, and the new housing price index fell 0.4% m/m. Markets responded with USD/CAD advancing 0.12% to 1.38, pushing the loonie to a five-week low.

The S&P/TSX Composite slipped 0.27% to 33,741.20 as WTI crude tumbled 5.28% to 102.08. Canada 2-year yields declined 20 basis points to 2.25%, while the 10-year yield rose 1.34% to 3.53%. The data reinforced views that the Bank of Canada faces little pressure to hike rates.

The Day Ahead

Focus shifts to Friday’s retail sales release, with consensus pointing to a 0.6% m/m gain in the final print and 0.9% in ex-autos sales. The senior loan officer survey at 06:30 ET will detail credit tightening trends across business and household segments. No high-impact Canadian data are scheduled for today or tomorrow.

Traders will watch USD/CAD and energy futures for any reversal signals ahead of the weekend. Broader global risk sentiment may influence CAD crosses in thin trading.

Other Economic Notes

Alberta oil-sands producers posted strong Q1 cash flows that support sustained capital spending despite softer global prices. Housing market weakness persists, with existing-home sales down 3.2% m/m in April and adding pressure for new supply measures. Ottawa extended the U.S.–Canada softwood-lumber agreement for another year, removing one near-term trade friction.

Higher-for-longer rates continue to favor select TSX financial and utility names.

Global Macro News

Sharp declines in WTI and Brent crude weighed on Canadian energy exports and related equities. The U.S. dollar retained safe-haven demand, capping CAD recovery despite the domestic data miss.

Trade-war risks between major economies threaten to dampen Canadian growth prospects into 2026. Oil windfalls provide partial offset but cannot fully counter external demand shocks. Global central-bank divergence keeps Canadian yields sensitive to U.S.

<i>↓ p.2</i>