Canada Macro Daily(Beta Mode)

Soft CPI Gives BoC Breathing Room

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,409.50 | +0.73% |

| USD/CAD | 1.38 | +0.38% |

| EUR/CAD | 1.60 | +0.14% |

| WTI Crude | 97.48 | +1.17% |

| Natural Gas | 3.11 | +2.92% |

| Gold | 4,520.20 | -0.43% |

| Brent Crude | 104.37 | +1.74% |

| Bitcoin | 77,443.18 | -0.12% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

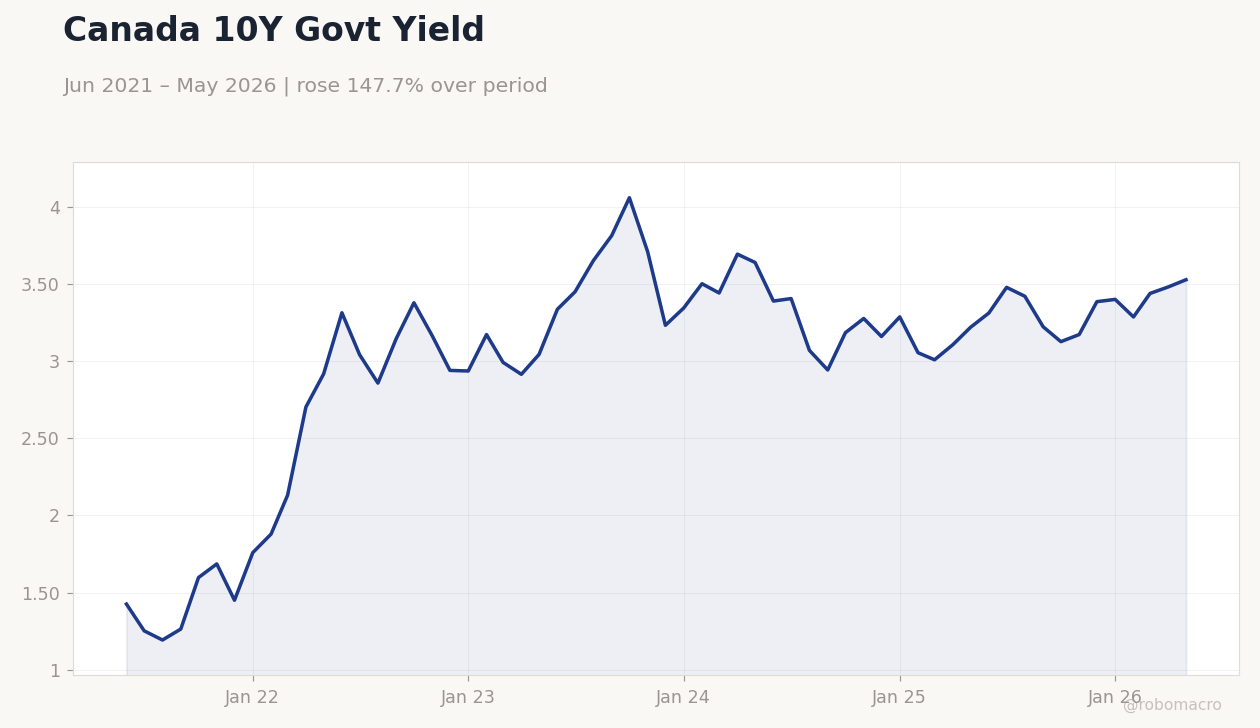

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.40 | 3.10 | 2.80 |

| Core Inflation Rate Year-over-Year | 2.50 | - | 2.10 |

| Inflation Rate Month-over-Month | 0.90 | 0.70 | 0.40 |

| New Housing Price Index Month-over-Month | -0.20 | 0 | -0.40 |

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Retail Sales Excluding Autos Month-over-Month | 0.50 | 0.90 | 04:30 |

| Retail Sales Month-over-Month Final | 0.70 | 0.60 | 04:30 |

| Retail Sales Month-over-Month Prel | - | - | 04:30 |

| Senior Loan Officer Survey | - | - | 06:30 |

- April CPI rose 2.8% y/y, below consensus, easing near-term BoC hike pressure

- S&P/TSX gained 0.73% while USD/CAD climbed 0.38% to 1.38 on softer inflation

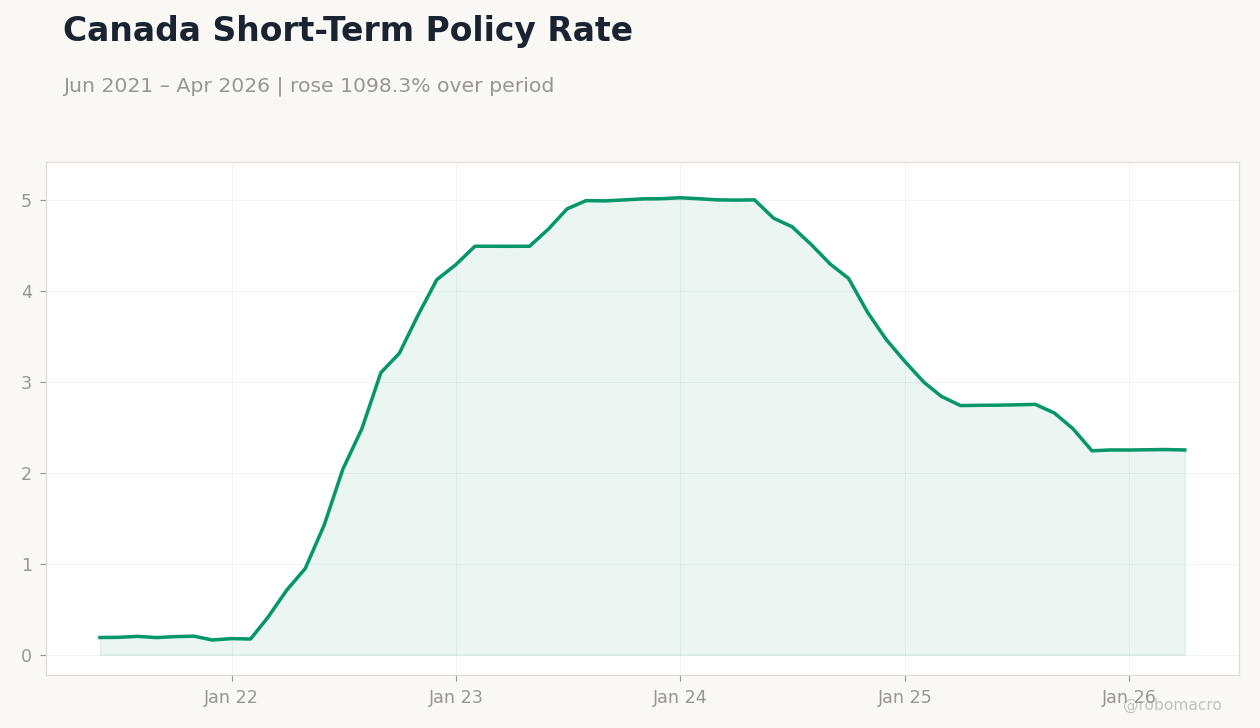

- Canada 2-year yield held at 2.25% as markets priced steady policy through summer

Yesterday's Recap

April CPI came in at 2.8% y/y versus 3.1% expected, with core measures at 2.1% and month-over-month inflation at just 0.4%. New housing prices fell 0.4% m/m, extending the recent softening trend. The S&P/TSX rose 0.73% to 34,409.50, led by energy and materials as WTI crude climbed 1.17% to 97.48.

USD/CAD advanced 0.38% to 1.38 while the Canada 2-year government yield stayed at 2.25%. The 10-year yield rose 1.34% to 3.53%. Natural gas jumped 2.92% to 3.11 amid cooler weather forecasts.

Markets interpreted the data as giving the Bank of Canada room to stay on hold.

The Day Ahead

Retail sales excluding autos are due at 04:30 ET with a 0.9% consensus gain after last month’s 0.5% rise. Final and preliminary retail sales figures will follow at the same time. The Senior Loan Officer Survey releases at 06:30 ET and may highlight tighter credit conditions.

No Bank of Canada speakers are scheduled. Traders will watch whether stronger sales data push back July cut odds already priced near 70%. CAD and front-end yields are expected to react most to the retail print.

Other Economic Notes

Energy producers reported solid Q1 cash flows that continue to support the TSX weighting in oil and gas. Housing starts remain above 240k annualized, offering limited relief on affordability. Ottawa’s alignment with U.S.

tariffs on Chinese EVs keeps bilateral trade risks contained. Broader commodity strength, especially in crude and natural gas, is lifting provincial fiscal outlooks in Alberta and Saskatchewan. Markets remain focused on whether persistent energy prices offset softer core inflation readings.

Global Macro News

Hopes for US-Iran diplomatic progress weighed on oil prices earlier in the week before a rebound lifted WTI above 97. The Canadian dollar slipped to a five-week low near 1.3750 as softer domestic CPI coincided with fading Middle East risk premium. Commerzbank noted that cooling inflation has reduced immediate BoC tightening expectations.

<i>↓ p.2</i>