Canada Macro Daily(Beta Mode)

BoC Holds Patient Stance Amid Soft CPI

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,724.80 | +0.74% |

| USD/CAD | 1.38 | +0.04% |

| EUR/CAD | 1.61 | +0.00% |

| WTI Crude | 92.43 | -4.32% |

| Natural Gas | 3.06 | +5.26% |

| Gold | 4,523.90 | +0.06% |

| Brent Crude | 95.81 | -7.47% |

| Bitcoin | 77,142.00 | -0.18% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

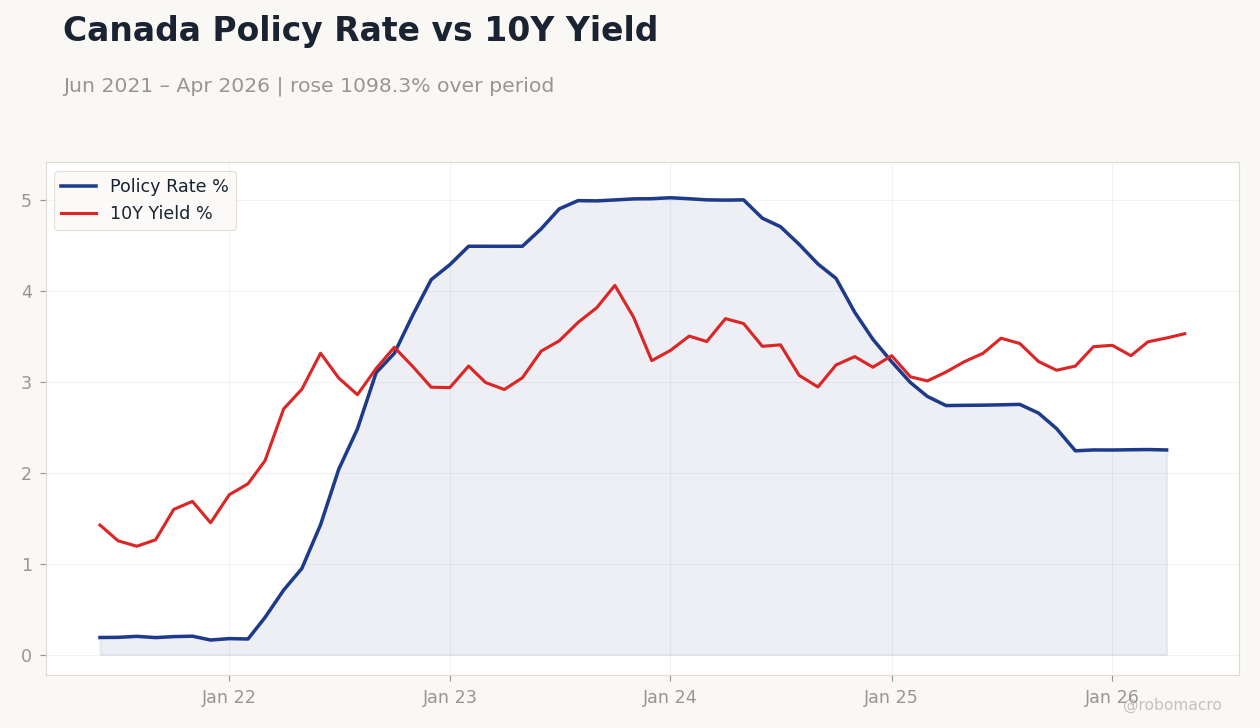

Canada Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1879,2.483,5.002,3.469,2.254,2.251 | 10Y Yield %: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Canada Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1879,2.483,5.002,3.469,2.254,2.251 | 10Y Yield %: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-28) | |||

| Current Account Balance | -700m | - | 04:30 |

| BoC Financial Stability Report | - | - | 06:00 |

| Friday (2026-05-29) | |||

| GDP Growth Quarter-over-Quarter | -0.20 | - | 04:30 |

| GDP Growth Rate Annualized | -0.60 | 1.50 | 04:30 |

| GDP Month-over-Month | 0.20 | 0.10 | 04:30 |

| GDP Month-over-Month Prel | - | - | 04:30 |

- TSX holds near records as banks report amid oil slide

- CAD weakens versus USD as Brent drops 7.47%

- BoC signals no rush to cut rates with CPI at 2.32%

Yesterday's Recap

Canadian equities advanced modestly with the S&P/TSX rising 0.74% to 34,724.80 as major banks posted results. The loonie eased slightly against the dollar with USD/CAD at 1.38 after a 0.04% gain. Energy prices fell sharply, with WTI crude declining 4.32% to 92.43 and Brent dropping 7.47% to 95.81, weighing on resource-linked names.

Canada 2-year yields eased 0.20% to 2.25% while the 10-year yield climbed 1.34% to 3.53%. Gold held steady near 4,523.90 and natural gas jumped 5.26% to 3.06. Market participants noted limited follow-through from oil volatility into broader risk assets.

The Day Ahead

Attention turns to the Bank of Canada Financial Stability Report on Thursday, which will assess household debt and housing risks. Current account data will follow the same morning. Friday brings first-quarter GDP figures, with consensus expecting 1.5% annualized growth after a prior contraction of 0.6%.

Month-over-month GDP is projected at 0.1%. Markets will parse any signals on growth resilience ahead of the next policy decision. No major speeches are scheduled before the weekend.

Other Economic Notes

Canada’s auto sector continues to face production cuts and softening demand. Youth unemployment remains elevated, raising questions about minimum wage effects on entry-level hiring. Banks reported contained loan losses despite higher rates, supporting equity valuations.

Dividend stocks on the TSX have drawn inflows as investors seek income in a slow-growth setting. National Bank earnings estimates sit at C$3.13 per share for the coming quarter.

Global Macro News

The ECB’s Isabel Schnabel called for a June rate hike even if Middle East tensions ease quickly. Oil prices retreated on hopes of an Iran-related supply deal, capping CAD support. The euro gained modestly on the loonie as risk appetite softened.

HSBC noted that oil rebounds provide only limited lift to the Canadian dollar. Broader equity markets held firm, with TSX dividend names outperforming in a narrow range. Global bond yields rose on persistent inflation concerns outside North America.

Canadian exporters face headwinds from softer European growth prospects.