Canada Macro Daily(Beta Mode)

BoC Flags Low-Hire, Low-Fire Market Clouding Rate Path

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,653.90 | -0.20% |

| USD/CAD | 1.38 | +0.24% |

| EUR/CAD | 1.61 | +0.25% |

| WTI Crude | 90.66 | -3.44% |

| Natural Gas | 3.05 | +5.53% |

| Gold | 4,469.70 | -0.68% |

| Brent Crude | 94.26 | -5.34% |

| Bitcoin | 75,730.27 | -0.13% |

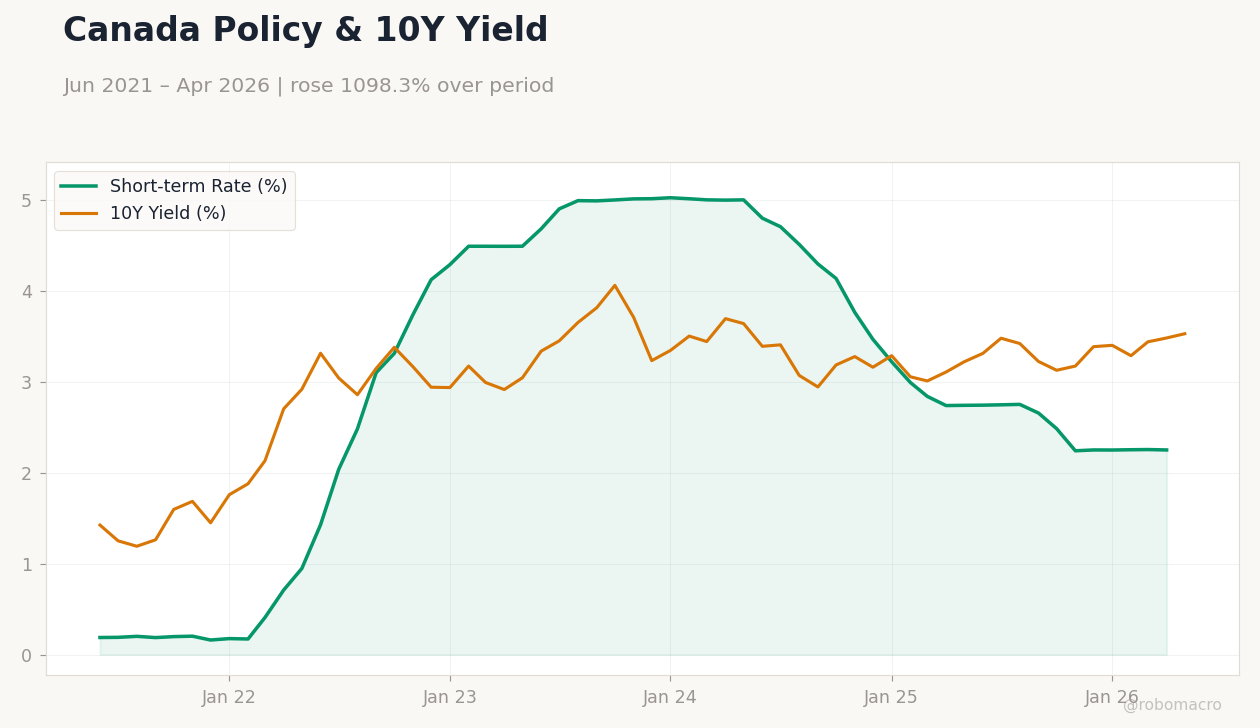

| Canada 2Y Govt Yield | 2.25% | -0.20% |

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

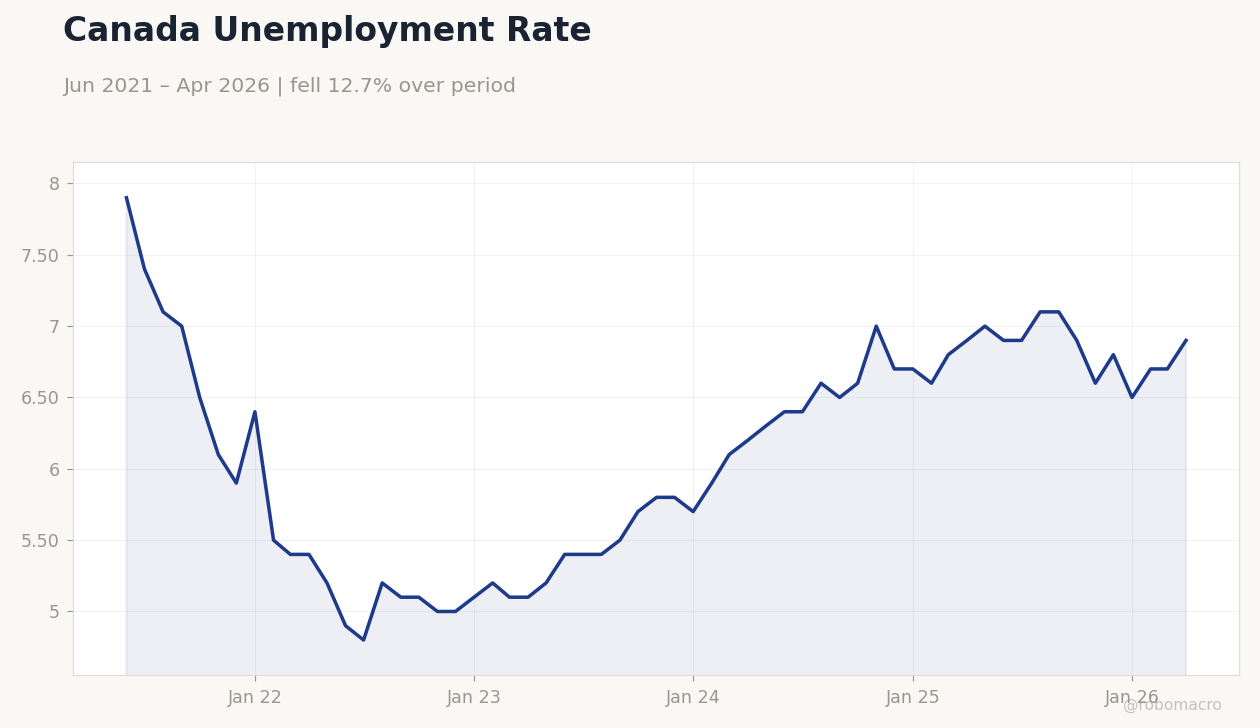

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.9 (2026-04-01) | Range: 4.8–7.9 | Trend(6pt): 7.9,5.2,5.7,6.7,6.7,6.9

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.9 (2026-04-01) | Range: 4.8–7.9 | Trend(6pt): 7.9,5.2,5.7,6.7,6.7,6.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Thursday (2026-05-28) | |||

| Current Account Balance | -700m | - | 04:30 |

| BoC Financial Stability Report | - | - | 06:00 |

| Friday (2026-05-29) | |||

| GDP Growth Quarter-over-Quarter | -0.20 | - | 04:30 |

| GDP Growth Rate Annualized | -0.60 | 1.50 | 04:30 |

| GDP Month-over-Month | 0.20 | 0.10 | 04:30 |

| GDP Month-over-Month Prel | - | - | 04:30 |

- Bank of Canada Deputy Governor Vincent highlighted a “low hiring-low firing” labor market that reduces dynamism and may blunt rate-cut transmission.

- S&P/TSX fell 0.20% to 34,653.90 while the 2-year yield matched the 2.25% policy rate and WTI crude dropped 3.44% to 90.66.

- Markets await the 28 May BoC Financial Stability Report and 29 May GDP prints that will shape expectations for further easing.

Yesterday's Recap

Canadian markets closed lower amid mixed yield moves and softer energy prices. The S&P/TSX declined 0.20% to 34,653.90 as value stocks underperformed. USD/CAD rose 0.24% to 1.38 while EUR/CAD gained 0.25% to 1.61.

The 2-year Government of Canada yield fell 0.20% to 2.25%, aligning with the Bank of Canada policy rate, whereas the 10-year yield climbed 1.34% to 3.53%. WTI crude fell 3.44% to 90.66 and Brent dropped 5.34% to 94.26; natural gas rose 5.53% to 3.05. Gold slipped 0.68% to 4,469.70.

No economic data were released on 26 May.

The Day Ahead

Attention turns to the 28 May Current Account Balance and the Bank of Canada Financial Stability Report at 06:00 ET. The report will detail risks from the evolving labor market and household debt. On 29 May, Statistics Canada releases Q1 GDP quarter-over-quarter, the annualized growth rate (consensus 1.5%), and monthly GDP.

A stronger-than-expected GDP print would further reduce odds of near-term easing. Markets will parse the Financial Stability Report for any signals on quantitative tightening pace.

Other Economic Notes

Canada’s CPI stood at 2.32% year-over-year in the latest reading, keeping real policy rates modestly positive. Structural labor-market shifts, including an aging population and reduced hiring-firing flows, are complicating the transmission of monetary policy. Housing starts rose in April, providing some support to rate-sensitive sectors, yet the broader recovery remains uneven.

Royalty increases announced by Alberta add a modest headwind for smaller energy producers.

Global Macro News

The ECB’s Isabel Schnabel signaled a possible June hike, supporting the euro against the Canadian dollar. Oil prices rebounded on Middle East supply concerns, lending some support to the loonie despite domestic data focus. The Indian rupee weakened against the US dollar on higher crude costs, illustrating broader EM pressure.

<i>↓ p.2</i>