Canada Macro Daily(Beta Mode)

BoC Stability Report Due as TSX Declines

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,412.10 | -0.70% |

| USD/CAD | 1.39 | +0.33% |

| EUR/CAD | 1.61 | +0.10% |

| WTI Crude | 91.26 | +2.91% |

| Natural Gas | 3.09 | +1.55% |

| Gold | 4,414.80 | -0.74% |

| Brent Crude | 94.85 | +0.59% |

| Bitcoin | 73,262.23 | -1.46% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

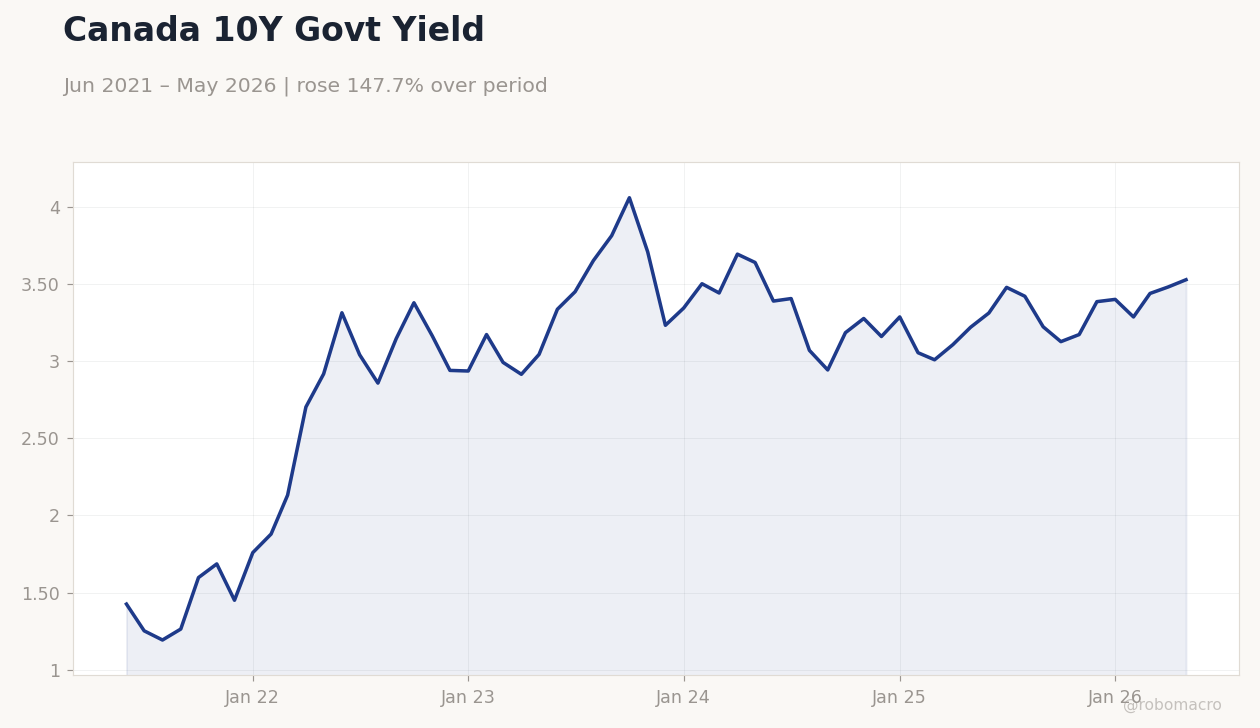

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Canada 10Y Govt Yield | Type: macro_line | Percent: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Canada 10Y Govt Yield | Type: macro_line | Percent: 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(5pt): 1.425,3.148,3.234,3.01,3.53

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Balance | -700m | -4,700m | 04:30 |

| BoC Financial Stability Report | - | - | 06:00 |

| Friday (2026-05-29) | |||

| GDP Growth Quarter-over-Quarter | -0.20 | - | 04:30 |

| GDP Growth Rate Annualized | -0.60 | 1.50 | 04:30 |

| GDP Month-over-Month | 0.20 | 0.10 | 04:30 |

| GDP Month-over-Month Prel | - | - | 04:30 |

- TSX falls 0.7% to 34,412 while USD/CAD climbs to 1.39 on yield shifts

- WTI crude jumps 2.91% to 91.26 amid Middle East supply risks

- BoC releases Financial Stability Report and current account data today

Yesterday's Recap

Canadian markets closed lower with the S&P/TSX Composite declining 0.70% to 34,412.10. USD/CAD advanced 0.33% to 1.39 while the 2-year government yield held at 2.25% and the 10-year yield rose to 3.53%. National Bank of Canada posted stronger Q2 2026 earnings driven by wealth management and net interest income.

Bank of Canada officials highlighted how structural labor market shifts, including a low-hire low-fire dynamic, are complicating policy assessments. No economic data releases occurred on May 27. Energy prices supported the broader commodity complex as natural gas rose 1.55% to 3.09.

Gold declined 0.74% to 4,414.80.

The Day Ahead

The Bank of Canada publishes its Financial Stability Report at 6:00 ET alongside the current account balance at 4:30 ET. Markets will assess any signals on financial system resilience and external balances. Tomorrow’s GDP prints include quarter-over-quarter growth, annualized rate, and monthly changes, all carrying high market impact.

The data will update views on the contraction seen in prior prints. OIS markets currently price limited near-term BoC easing given the 2.25% policy rate and 2.32% CPI level.

Other Economic Notes

National Bank of Canada’s capital markets segment showed slower momentum despite the headline profit beat. Royal Bank of Canada earnings remain in focus for capital markets revenue trends. The labor market’s reduced churn continues to weigh on productivity and competitiveness according to BoC analysis.

Ottawa’s extension of tariffs on Chinese EVs adds modest price pressure in the auto sector. No major shifts in US-Canada trade relations emerged overnight.

Global Macro News

Oil prices rose on renewed Middle East hostilities after US forces intercepted Iranian drones. WTI settled at 91.26 and Brent at 94.85, supporting CAD-linked assets. Bitcoin fell 1.46% to 73,262 amid broader risk-off flows.

Bank of Korea left rates unchanged citing Middle East uncertainty. Cross-border payment initiatives gained attention as the BoC joined BIS Project Agorá. <i>↓ p.2</i>