Canada Macro Daily(Beta Mode)

BoC Flags Debt Risks in Stability Report

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,517.70 | +0.31% |

| USD/CAD | 1.38 | -0.31% |

| EUR/CAD | 1.61 | -0.06% |

| WTI Crude | 87.77 | -1.27% |

| Natural Gas | 3.33 | +1.40% |

| Gold | 4,561.90 | +1.39% |

| Brent Crude | 91.30 | -2.57% |

| Bitcoin | 73,359.72 | -0.24% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Current Account Balance | -1,000m | -4,700m | -7,200m |

| BoC Financial Stability Report | - | - | - |

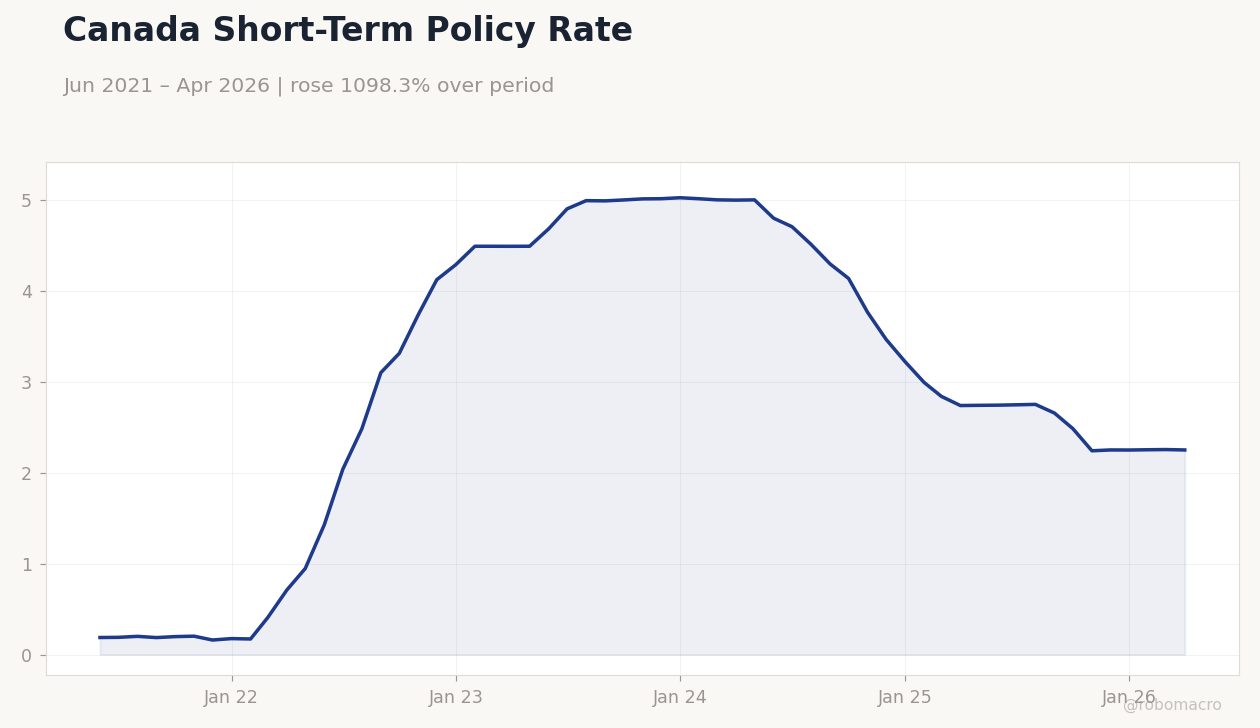

Canada Short-Term Policy Rate | Type: macro_line | Percent: 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1879,2.483,5.002,3.469,2.254,2.251

Canada Short-Term Policy Rate | Type: macro_line | Percent: 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1879,2.483,5.002,3.469,2.254,2.251

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | -0.20 | - | 04:30 |

| GDP Growth Rate Annualized | -0.60 | 1.50 | 04:30 |

| GDP Month-over-Month | 0.20 | 0 | 04:30 |

| GDP Month-over-Month Prel | - | - | 04:30 |

- Current account deficit widened sharply to C$7.2B in Q1 versus C$4.7B consensus

- BoC Financial Stability Report highlights system resilience alongside rising household vulnerabilities

- S&P/TSX gained 0.31% while USD/CAD fell 0.31% to 1.38 on the session

Yesterday's Recap

Canada’s Q1 current account balance printed at -C$7.2B, missing consensus by a wide margin and reflecting weaker goods and services balances. The Bank of Canada published its Financial Stability Report, stating the financial system remains solid yet faces growing risks from elevated household debt and potential external shocks. Markets digested the report with limited volatility.

The S&P/TSX closed 0.31% higher at 34,517.70, supported by financials. USD/CAD declined 0.31% to 1.38 as the Canadian dollar strengthened modestly. The 2-year Government of Canada yield fell 20 basis points to 2.25% while the 10-year yield rose 1.34% to 3.53%.

WTI crude settled lower at 87.77 amid mixed global oil moves.

The Day Ahead

Statistics Canada will release first-quarter GDP figures at 8:30 a.m. ET, including quarter-over-quarter, annualized, and monthly growth rates. Markets expect the annualized measure to rebound to 1.5% after the prior -0.6% print.

Month-over-month GDP is forecast at 0.0% versus the previous 0.2% gain. The data will provide the first comprehensive view of economic momentum following the soft Q4 outcome. No Bank of Canada speakers are scheduled.

Traders will watch for any revisions that could alter expectations around the timing of future policy adjustments.

Other Economic Notes

Royal Bank of Canada reported strong earnings across segments, lifting sentiment toward domestic banks. Dividend announcements from major lenders drew renewed attention to TSX financials. Household debt levels remain a focal point after the BoC explicitly flagged affordability strains in its stability assessment.

Broader credit conditions show modest tightening as lenders respond to higher-for-longer borrowing costs.

Global Macro News

Oil prices fluctuated on reports of progress toward a US-Iran ceasefire that could ease supply concerns in the Strait of Hormuz. WTI fell 1.27% to 87.77 while Brent dropped 2.57% to 91.30. Natural gas rose 1.40% to 3.33 on cooler North American weather forecasts.

<i>↓ p.2</i>