Canada Macro Daily(Beta Mode)

Canada Enters Technical Recession

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,769.10 | +0.73% |

| USD/CAD | 1.38 | +0.35% |

| EUR/CAD | 1.61 | -0.14% |

| WTI Crude | 90.40 | +3.48% |

| Natural Gas | 3.30 | +0.30% |

| Gold | 4,539.50 | -0.46% |

| Brent Crude | 93.64 | +1.73% |

| Bitcoin | 72,034.01 | -2.10% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

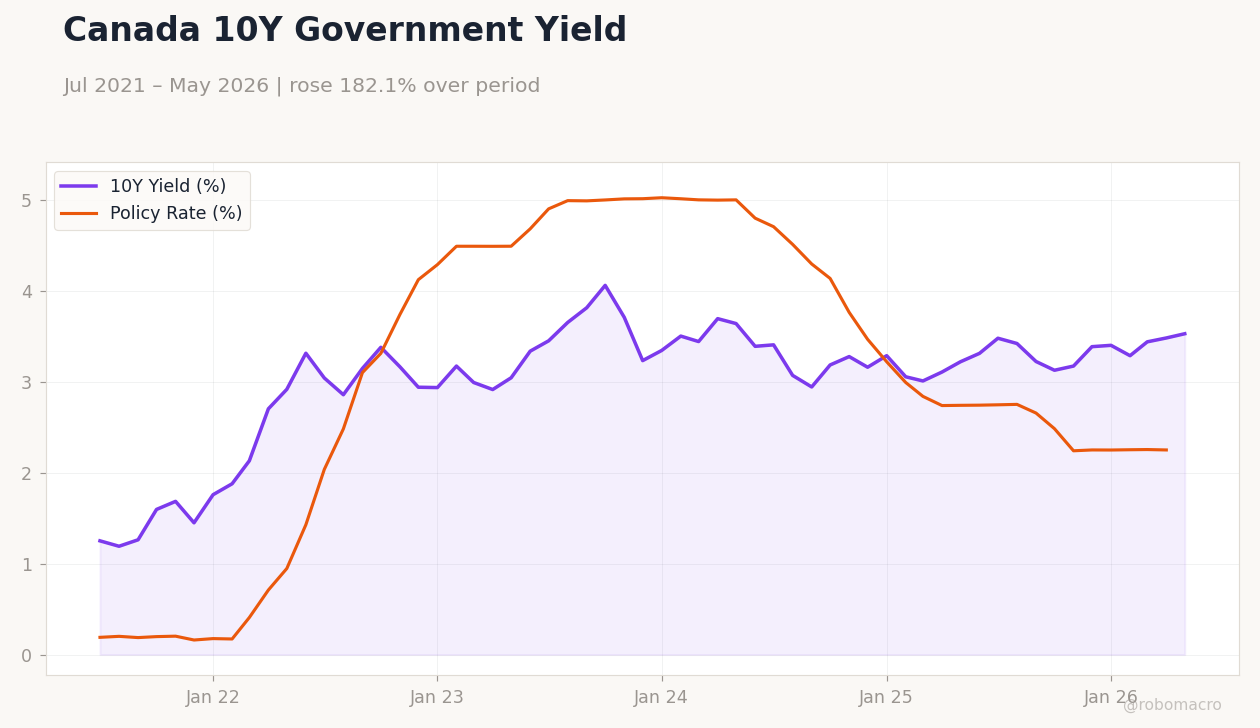

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Canada Unemployment Rate | Type: macro_line | Unemployment Rate (%): 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Index | 53.30 | - | 05:30 |

| Friday (2026-06-05) | |||

| Headline Unemployment Rate | 6.90 | 6.90 | 04:30 |

| Employment Change | -17,700 | 10,200 | 04:30 |

| Full-Time Employment Change | -46,700 | - | 04:30 |

| Labor Force Participation | 65 | - | 04:30 |

| Part-Time Employment Change | 29,000 | - | 04:30 |

| Ivey PMI Seasonally Adjusted | 57.70 | 55 | 06:00 |

- Q1 GDP contraction confirms technical recession with two quarters of declines amid tariff uncertainty.

- S&P/TSX rises 0.73% while USD/CAD strengthens 0.35% as oil prices climb.

- BoC holds policy rate at 2.25% with markets reassessing cut odds after weak growth data.

Yesterday's Recap

Canada reported Q1 GDP contraction of 0.1% annualized, marking two consecutive quarters of negative growth and confirming a technical recession. Markets digested the surprise data release with no major economic indicators scheduled for May 31. The S&P/TSX Composite advanced 0.73% to 34,769.10, supported by energy sector gains.

USD/CAD climbed to 1.38, up 0.35%, as firmer US dollar offset recovering oil prices. Canada 2-year yields fell 0.20% to 2.25% while 10-year yields rose 1.34% to 3.53%. WTI crude jumped 3.48% to 90.40 amid OPEC+ signals.

Economists noted the stall but downplayed immediate recession risks given resilient exports.

The Day Ahead

Canada S&P Global Manufacturing PMI releases at 5:30 ET today with prior reading at 53.3. Attention turns to Friday's high-impact labor report showing expected unemployment rate steady at 6.9% and employment change forecast at +10,200. Ivey PMI seasonally adjusted is also due Friday with consensus at 55.0.

No Bank of Canada speakers or minutes are scheduled this week. Markets will monitor US ISM manufacturing for spillover effects on CAD crosses and BoC policy expectations.

Other Economic Notes

Tariff uncertainty has increased downside risks to growth according to recent Bank of Canada commentary. Housing starts rose modestly in April while existing home sales stayed flat. Alberta energy regulator approved new oil-sands projects adding capacity by 2028.

Broader themes center on whether the technical recession will shift BoC focus toward earlier easing despite CPI at 2.32%.

Global Macro News

US Treasury yields climbed on firmer Fed rate hike bets and geopolitical tensions supporting the dollar. Brent crude advanced 1.73% to 93.64 while natural gas edged higher 0.30%. Bitcoin fell 2.10% to 72,034 amid risk-off flows.

EUR/CAD eased 0.14% to 1.61 as German retail sales data supported the euro. <i>↓ p.2</i>