Canada Macro Daily(Beta Mode)

BoC Urges Calm Over Technical Recession Risk

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,734.90 | -0.10% |

| USD/CAD | 1.38 | +0.37% |

| EUR/CAD | 1.61 | +0.38% |

| WTI Crude | 91.05 | -1.20% |

| Natural Gas | 3.19 | +0.50% |

| Gold | 4,560.10 | +1.90% |

| Brent Crude | 93.85 | -1.19% |

| Bitcoin | 69,422.75 | -2.66% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

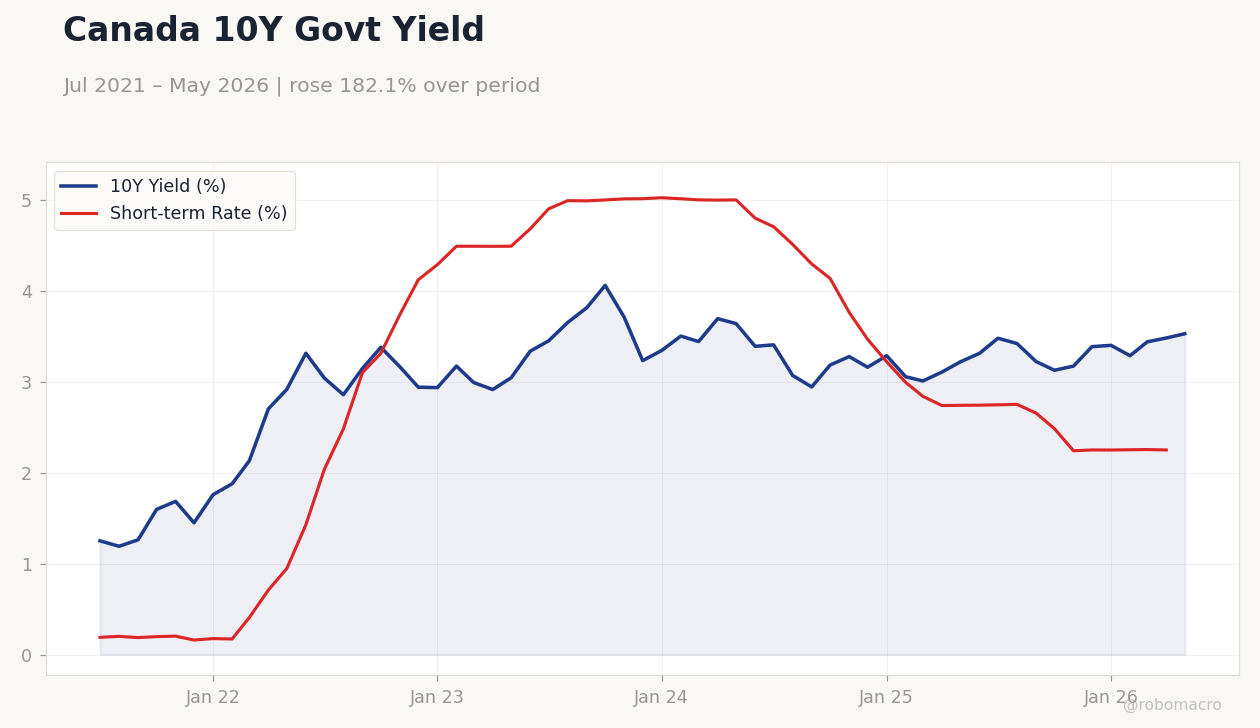

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Index | 53.30 | - | 52.90 |

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield (%): 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.441,3.53 | Short-term Rate (%): 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.251

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield (%): 3.53 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.441,3.53 | Short-term Rate (%): 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.251

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Friday (2026-06-05) | |||

| Headline Unemployment Rate | 6.90 | 6.90 | 04:30 |

| Employment Change | -17,700 | 10,200 | 04:30 |

| Full-Time Employment Change | -46,700 | - | 04:30 |

| Labor Force Participation | 65 | - | 04:30 |

| Part-Time Employment Change | 29,000 | - | 04:30 |

| Ivey PMI Seasonally Adjusted | 57.70 | 55 | 06:00 |

- Manufacturing PMI slips to 52.9 from 53.3 on June 1

- BoC cautions against recession reading of Q1 GDP stall

- TSX falls 0.10% while USD/CAD rises 0.37% to 1.38

Yesterday's Recap

Statistics Canada’s S&P Global Manufacturing PMI fell to 52.9 in May, extending the prior month’s 53.3 print and signaling slower factory expansion. Markets digested the release alongside BoC statements that explicitly warned against treating the Q1 GDP contraction as conclusive evidence of recession. The S&P/TSX closed 0.10% lower at 34,734.90 while the 2-year Government of Canada yield held at 2.25%.

USD/CAD climbed 0.37% to 1.38 as WTI crude dropped 1.20% to $91.05. The 10-year yield rose 1.34% to 3.53% and gold advanced 1.90% to $4,560.10. Senior Deputy Governor Carolyn Rogers stressed that GDP figures alone should not drive policy conclusions.

The Day Ahead

Attention turns to Friday’s labor-force survey, where the unemployment rate is expected to remain at 6.9% and net employment is forecast to rise 10,200 after last month’s 17,700 decline. The Ivey PMI is projected to ease to 55.0 from 57.7. Markets will also monitor any additional BoC speeches for further guidance on how officials weigh the technical recession label.

Energy prices and USD/CAD moves will remain sensitive to incoming U.S. data that could influence cross rates.

Other Economic Notes

Headline CPI stands at 2.32% year-over-year, keeping the policy rate at 2.25% in restrictive territory. Natural gas prices edged 0.50% higher to $3.19, providing modest support to western Canadian producers. Equity investors continue to favor value banks on the TSX amid stable domestic yields.

The combination of softer PMI and steady inflation leaves the Bank of Canada with limited room to signal near-term easing.

Global Macro News

Brent crude fell 1.19% to $93.85, capping CAD support from the energy complex. Bitcoin declined 2.66% to $69,422.75, reflecting broader risk-off sentiment that weighed on Canadian cyclicals. EUR/CAD rose 0.38% to 1.61 as euro-area data showed modest improvement.

Canadian dollar weakness against the USD was driven by firmer U.S. yields and the domestic growth scare. Oil-price volatility remains the dominant external factor for both CAD crosses and the TSX energy sector.