Canada Macro Daily(Beta Mode)

Jobs Beat Eases Canadian Recession Fears

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,663.99 | +0.73% |

| USD/CAD | 1.39 | +0.22% |

| EUR/CAD | 1.61 | -0.34% |

| WTI Crude | 90.71 | +0.19% |

| Natural Gas | 3.14 | -2.76% |

| Gold | 4,358.60 | +0.50% |

| Brent Crude | 93.92 | +0.89% |

| Bitcoin | 63,440.80 | +0.32% |

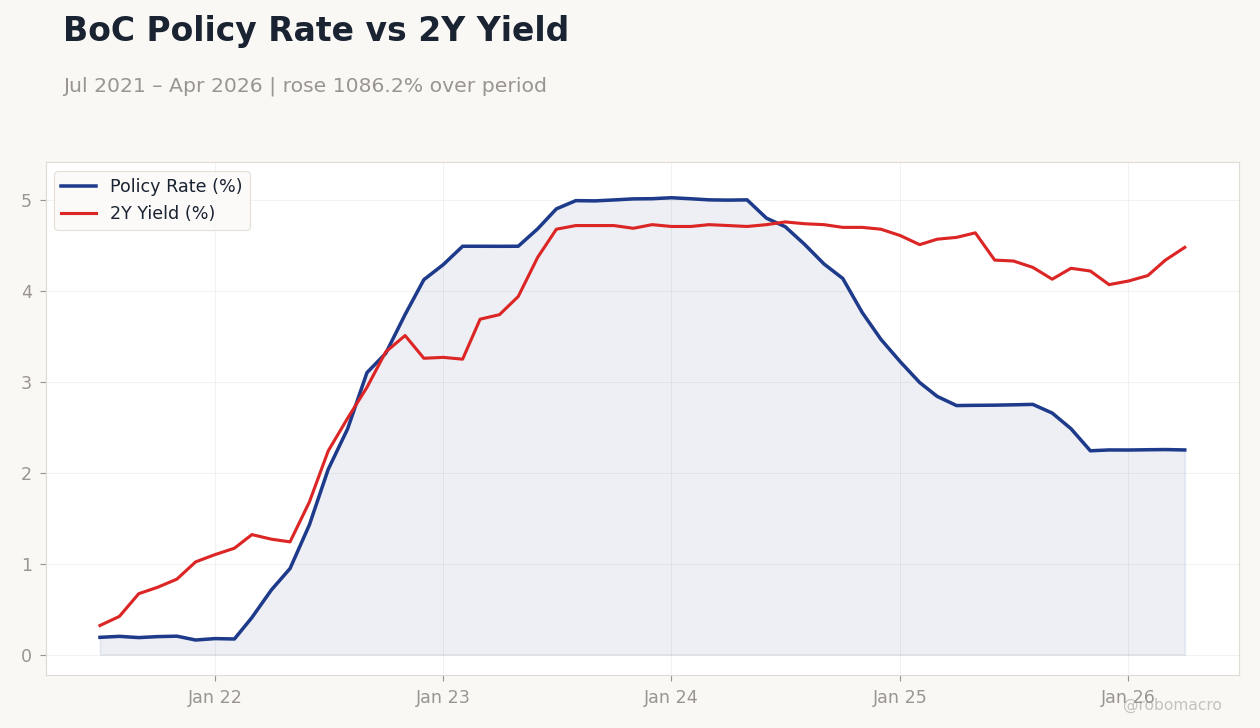

| Canada 2Y Govt Yield | 2.25% | -0.20% |

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

BoC Policy Rate vs 2Y Yield | Type: macro_line | Policy Rate (%): 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.251 | 2Y Yield (%): 4.48 (2026-04-01) | Range: 0.32–4.76 | Trend(6pt): 0.32,2.94,4.69,4.61,4.34,4.48

BoC Policy Rate vs 2Y Yield | Type: macro_line | Policy Rate (%): 2.251 (2026-04-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.251 | 2Y Yield (%): 4.48 (2026-04-01) | Range: 0.32–4.76 | Trend(6pt): 0.32,2.94,4.69,4.61,4.34,4.48

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-09) | |||

| Trade Balance | 1,780m | 1,900m | 04:30 |

| Wednesday (2026-06-10) | |||

| BoC Interest Rate Decision | 2.25 | 2.25 | 05:45 |

| BoC Press Conference | - | - | 06:30 |

- Canada adds 88,000 jobs in May, unemployment falls to 6.6%

- Markets price BoC hold at 2.25% ahead of Wednesday decision

- TSX rises 0.73% while USD/CAD climbs to 1.39 on yield moves

Yesterday's Recap

Canadian equity and currency markets advanced after the surprise May employment gain of 88,000 jobs dropped the unemployment rate to 6.6%. The S&P/TSX Composite closed at 34,663.99, up 0.73%, supported by energy and materials sectors. USD/CAD rose 0.22% to 1.39 while the 2-year Government of Canada yield fell 0.20% to 2.25%.

Natural gas prices dropped 2.76% to 3.14 amid mild weather forecasts. Gold advanced 0.50% to 4,358.60 on safe-haven demand. Brent crude gained 0.89% to 93.92, reinforcing CAD support through higher oil revenues.

No major data releases occurred on 7 June, leaving the jobs print as the dominant driver of price action.

The Day Ahead

Statistics Canada will release the May trade balance at 04:30 ET on 9 June, with consensus pointing to a C$1.9 billion surplus. Attention then shifts to the Bank of Canada interest rate decision and press conference on 10 June. Economists widely expect the policy rate to remain at 2.25%.

Markets will scrutinize Governor Macklem’s guidance for any shift in the easing timeline. The release coincides with fresh CPI data that showed 2.32% year-over-year inflation in March, keeping price stability in focus.

Other Economic Notes

Ottawa launched a C$25 billion fund to counter pressure from a weak loonie and elevated yields. Housing starts continued to soften, extending the supply-side drag on growth. Alberta oil-sands producers flagged Q1 cash-flow shortfalls that may prompt further capex reductions.

Broader discussions on USMCA auto rules remain procedural and carry limited near-term tariff risk for Canadian exporters.

Global Macro News

Oil prices rose despite softer China demand signals, with WTI at 90.71. Trump reiterated support for a new Fed chair while continuing to push for lower U.S. rates, adding volatility to global yield curves.

Canadian dollar crosses remained sensitive to widening Canada-U.S. yield differentials. NATO innovation fund talks advanced without Canadian participation, limiting direct fiscal implications.

<i>↓ p.2</i>