Canada Macro Daily(Beta Mode)

BoC Holds at 2.25% as Growth Falters

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,151.30 | -0.76% |

| USD/CAD | 1.40 | +0.17% |

| EUR/CAD | 1.61 | +0.03% |

| WTI Crude | 89.18 | -0.94% |

| Natural Gas | 3.11 | -2.26% |

| Gold | 4,110.00 | +0.04% |

| Brent Crude | 92.18 | -0.99% |

| Bitcoin | 63,080.27 | +2.65% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

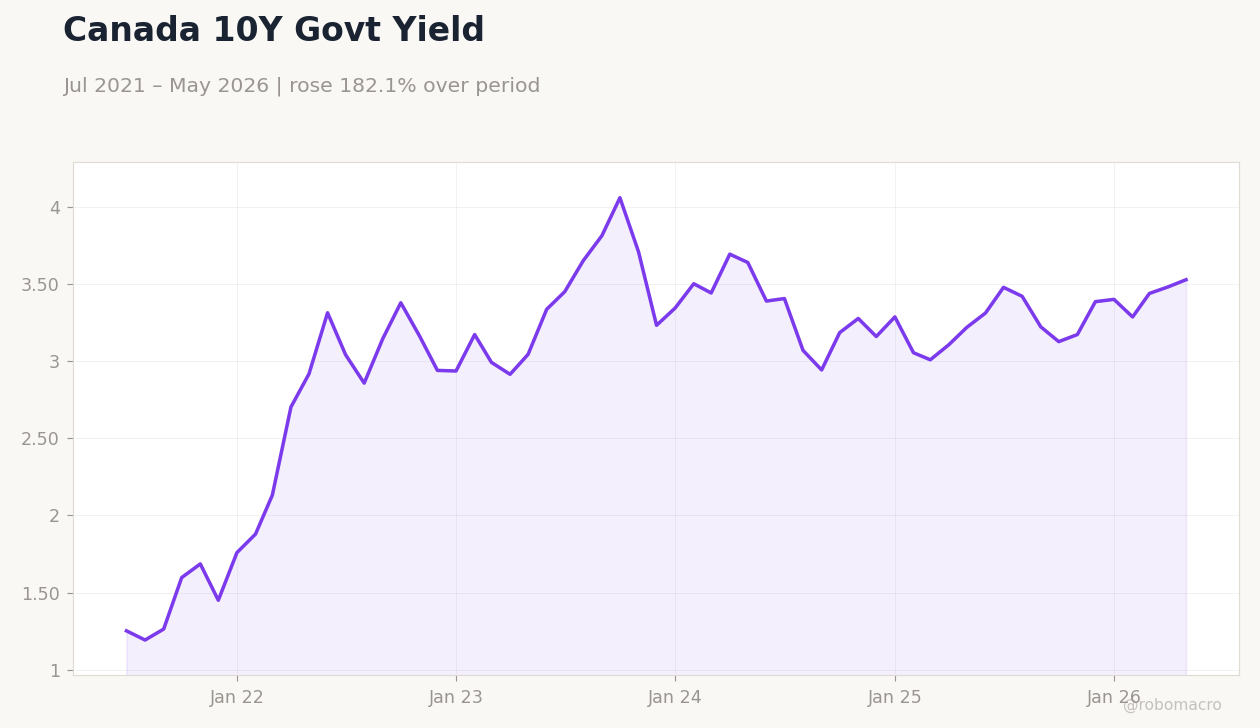

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 1,750m | 2,600m | 2,720m |

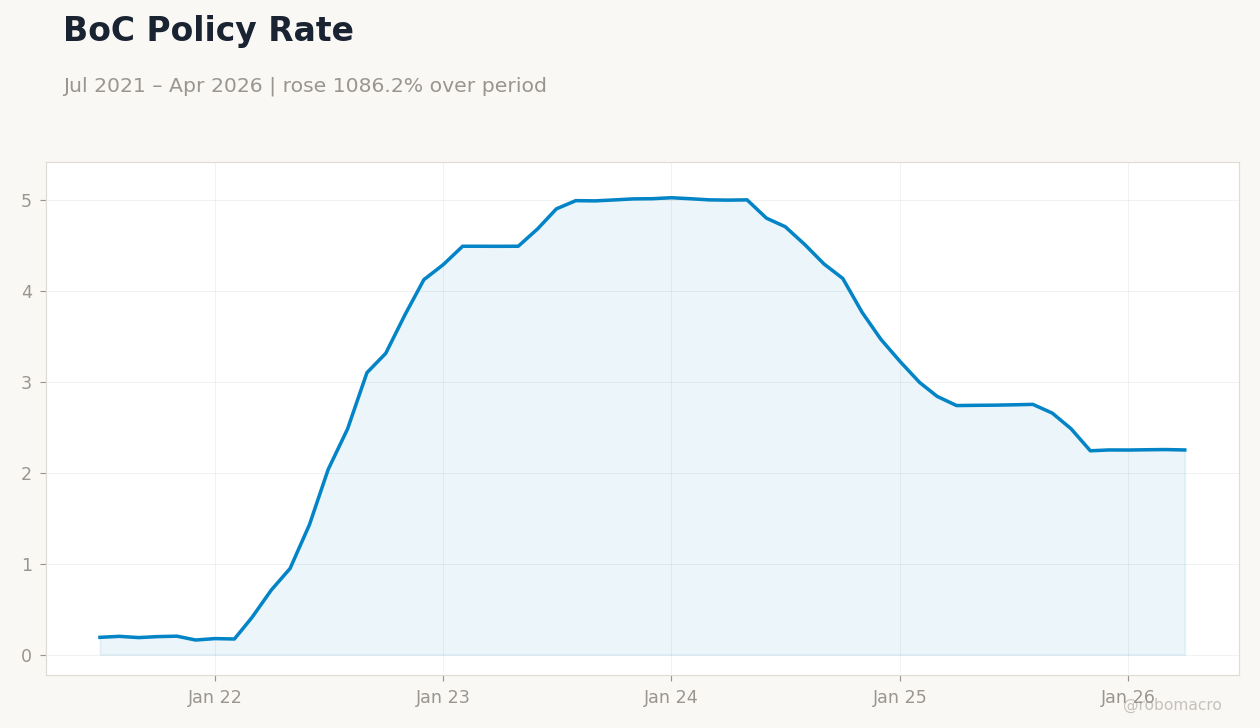

| BoC Interest Rate Decision | 2.25 | 2.25 | 2.25 |

| BoC Press Conference | - | - | - |

Canada Unemployment Rate | Type: macro_line | Unemployment %: 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Canada Unemployment Rate | Type: macro_line | Unemployment %: 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- BoC holds policy rate at 2.25% and flags weaker-than-expected growth without declaring recession

- Trade balance beats consensus at C$2.72 billion while TSX drops 0.76%

- 2-year yields fall to 2.25% as markets price steady policy amid soft domestic data

Yesterday's Recap

The Bank of Canada kept its benchmark rate at 2.25% for the fifth straight meeting, matching the prior level and consensus forecast. Governor Tiff Macklem stated the economy was weaker than expected yet stopped short of labeling conditions a recession. Trade balance data printed at C$2.72 billion, exceeding the C$2.60 billion consensus.

The S&P/TSX Composite fell 0.76% to 34,151.30 as energy shares lagged. Canada’s 2-year government yield declined 20 basis points to 2.25% while the 10-year yield rose to 3.53%. USD/CAD climbed 0.17% to 1.40 on the day.

WTI crude slipped 0.94% to $89.18, adding pressure to resource-linked equities.

The Day Ahead

No high-impact Canadian data releases are scheduled for the next two sessions. Market focus will remain on digestion of the BoC’s latest forward guidance and any follow-up comments from officials. Traders will monitor energy price swings for their effect on CAD crosses and provincial revenues.

Attention is also turning to the next CPI print due later this month, given the 2.32% year-over-year reading recorded in March. Thin calendars typically amplify reactions to any unexpected global oil or rate signals.

Other Economic Notes

Persistent weakness in domestic demand continues to complicate the inflation outlook despite the 2.32% CPI level. Technical recession risks flagged by external analysts add to the policy trade-off between supporting growth and guarding against renewed price pressures. Government of Canada bond curves reflect expectations of prolonged stability in the policy rate.

Energy export revenues remain a key swing factor for both fiscal balances and the external accounts.

Global Macro News

Escalating Middle East tensions lifted safe-haven flows into the Canadian dollar even as the BoC held rates. Brent crude fell nearly 1% to $92.18 on optimism over potential Iran-US de-escalation. Gold held steady near $4,110, offering limited support to the TSX’s materials sector.

<i>↓ p.2</i>