Canada Macro Daily(Beta Mode)

BoC Holds at 2.25% Amid Weak Growth

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,855.50 | +0.53% |

| USD/CAD | 1.39 | -0.05% |

| EUR/CAD | 1.61 | -0.04% |

| WTI Crude | 86.32 | -1.58% |

| Natural Gas | 3.12 | +1.13% |

| Gold | 4,207.10 | +2.86% |

| Brent Crude | 89.10 | -1.42% |

| Bitcoin | 63,514.71 | -0.07% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

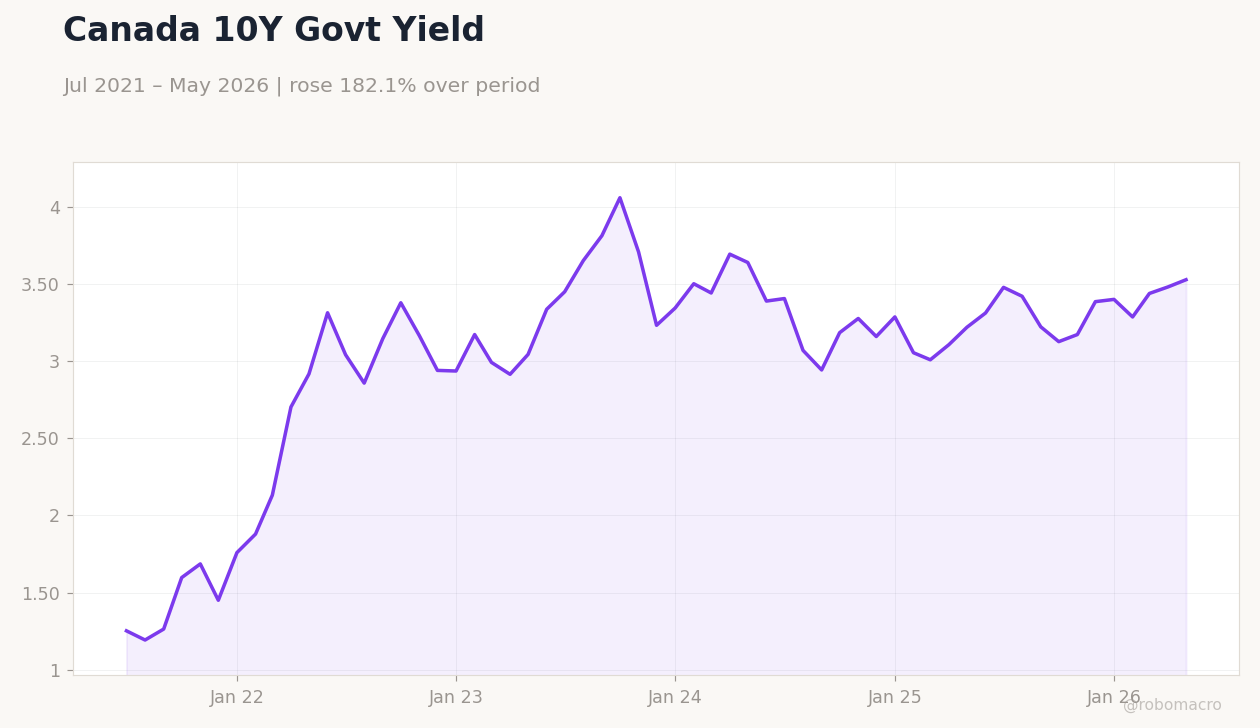

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Trade Balance | 1,750m | 2,600m | 2,720m |

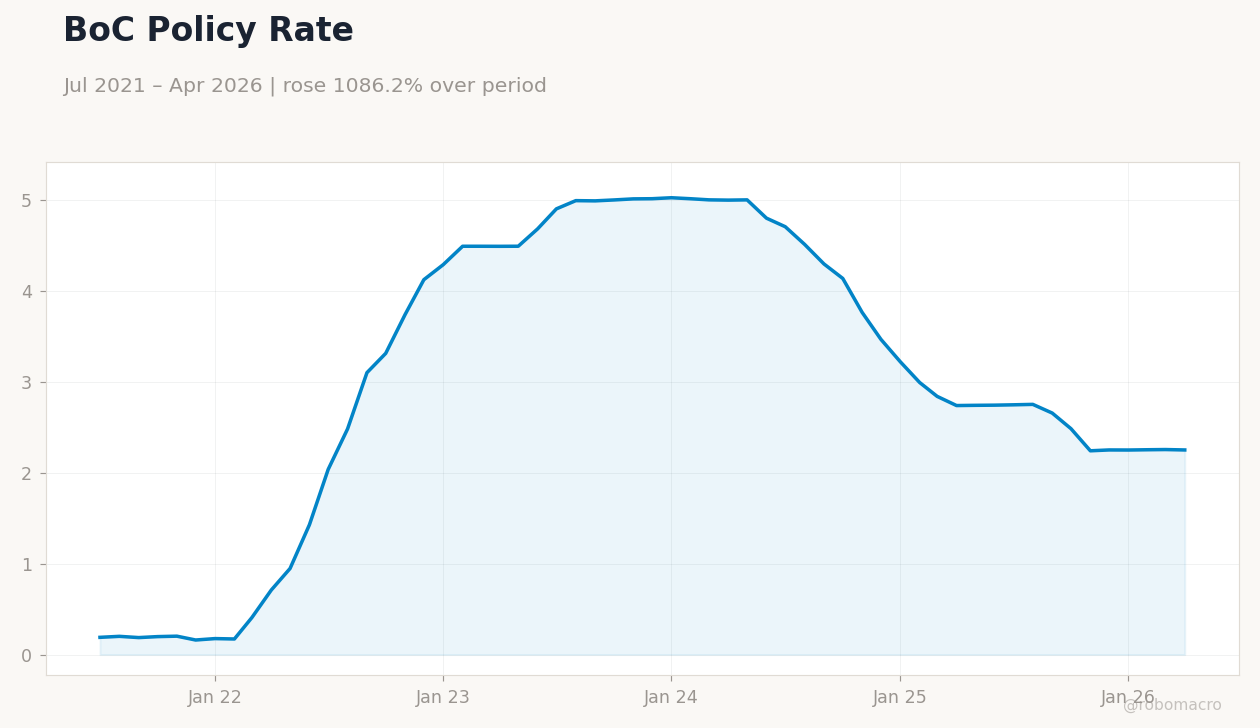

| BoC Interest Rate Decision | 2.25 | 2.25 | 2.25 |

| BoC Press Conference | - | - | - |

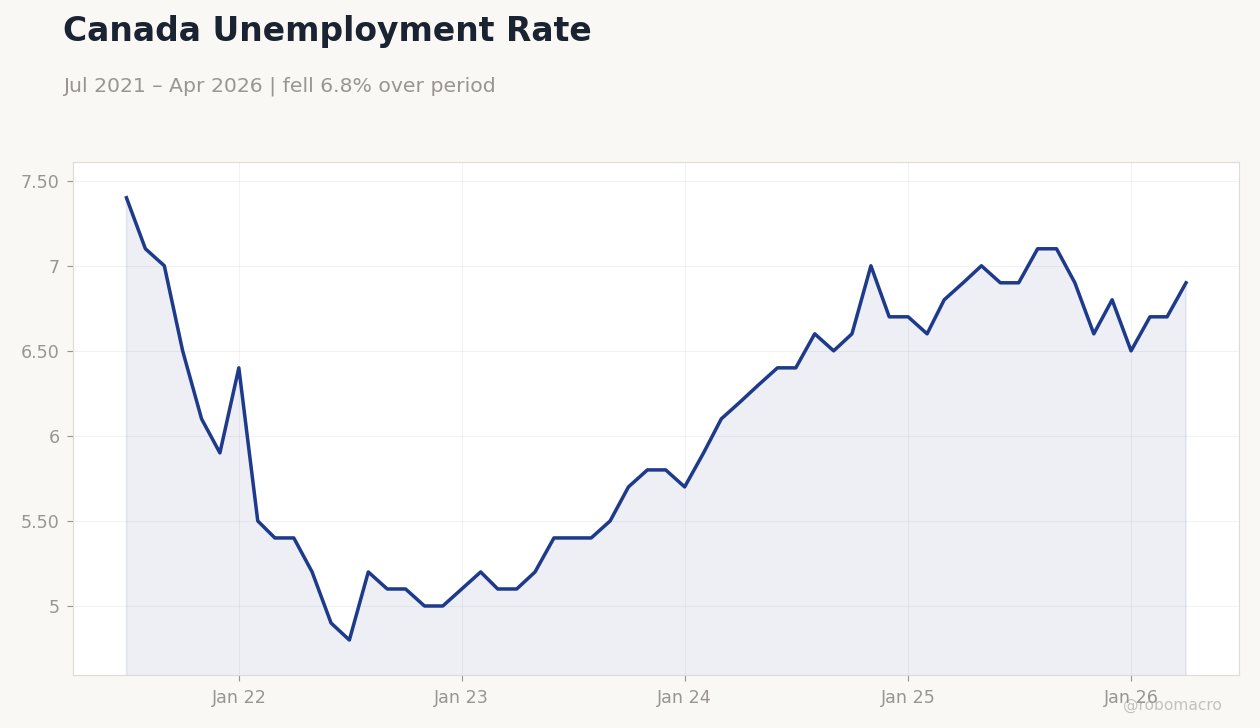

Canada Unemployment Rate | Type: macro_line | %: 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Canada Unemployment Rate | Type: macro_line | %: 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Bank of Canada keeps policy rate unchanged at 2.25 percent

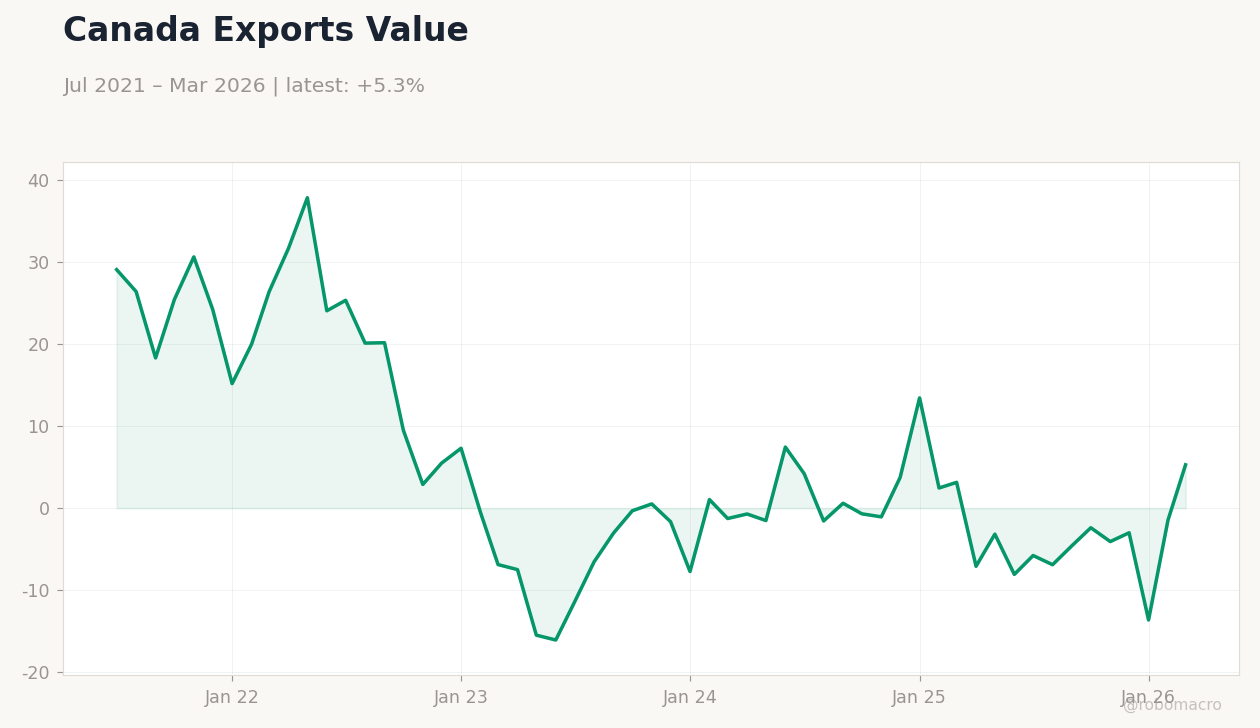

- Trade surplus expands to CAD 2.72 billion, beating forecasts

- TSX advances 0.53 percent while CAD firms modestly against USD

Yesterday's Recap

The Bank of Canada left its target rate at 2.25 percent, matching consensus and prior levels, after the committee assessed persistent inflation pressures against subdued domestic demand. The accompanying press conference highlighted risks that elevated services prices could keep core measures sticky even as headline CPI sits at 2.32 percent. Trade data released the prior day showed a CAD 2.72 billion surplus, exceeding the CAD 2.60 billion consensus and reversing the earlier CAD 1.75 billion print on stronger exports.

Equity markets responded positively, lifting the S&P/TSX 0.53 percent to 34,855.50. The Canadian dollar edged 0.05 percent firmer to 1.39 versus the USD while the 2-year Government of Canada yield fell 20 basis points to 2.25 percent. Oil prices declined more than 1.4 percent, trimming energy-sector gains, whereas gold surged 2.86 percent to 4,207.10 amid safe-haven flows.

The Day Ahead

No major Canadian data releases are scheduled for the next two sessions, leaving markets to digest the Bank of Canada’s latest signals. Attention will turn to any follow-up speeches by Governing Council members for clarification on the inflation-growth trade-off. Global developments, particularly oil-price volatility tied to Middle East tensions, will likely influence CAD crosses and TSX energy weights.

Fixed-income desks will monitor 10-year yields after yesterday’s rise to 3.53 percent. Traders also await any incremental updates on quantitative tightening pace ahead of month-end liquidity operations.

Other Economic Notes

Weak real GDP prints and soft retail sales have kept growth concerns elevated, limiting the Bank of Canada’s room to ease despite the policy rate already sitting at 2.25 percent. Inflation at 2.32 percent continues to reflect shelter and services components that have proven slower to moderate. Energy export revenues remain sensitive to WTI and Brent swings, with yesterday’s price drop weighing on near-term fiscal projections.

The combination of steady policy and soft activity data leaves the Canadian dollar range-bound near 1.39 against the greenback.

Global Macro News

The European Central Bank raised its deposit rate 25 basis points, tightening global financial conditions and supporting the euro against commodity currencies including the CAD. <i>↓ p.2</i>