Canada Macro Daily(Beta Mode)

BoC Holds at 2.25% as Housing Starts Loom

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,937.90 | +0.77% |

| USD/CAD | 1.40 | +0.03% |

| EUR/CAD | 1.62 | +0.32% |

| WTI Crude | 80.15 | -5.57% |

| Natural Gas | 3.05 | -2.28% |

| Gold | 4,362.70 | +3.50% |

| Brent Crude | 82.86 | -5.12% |

| Bitcoin | 66,167.12 | +0.70% |

| Canada 2Y Govt Yield | 2.25% | -0.20% |

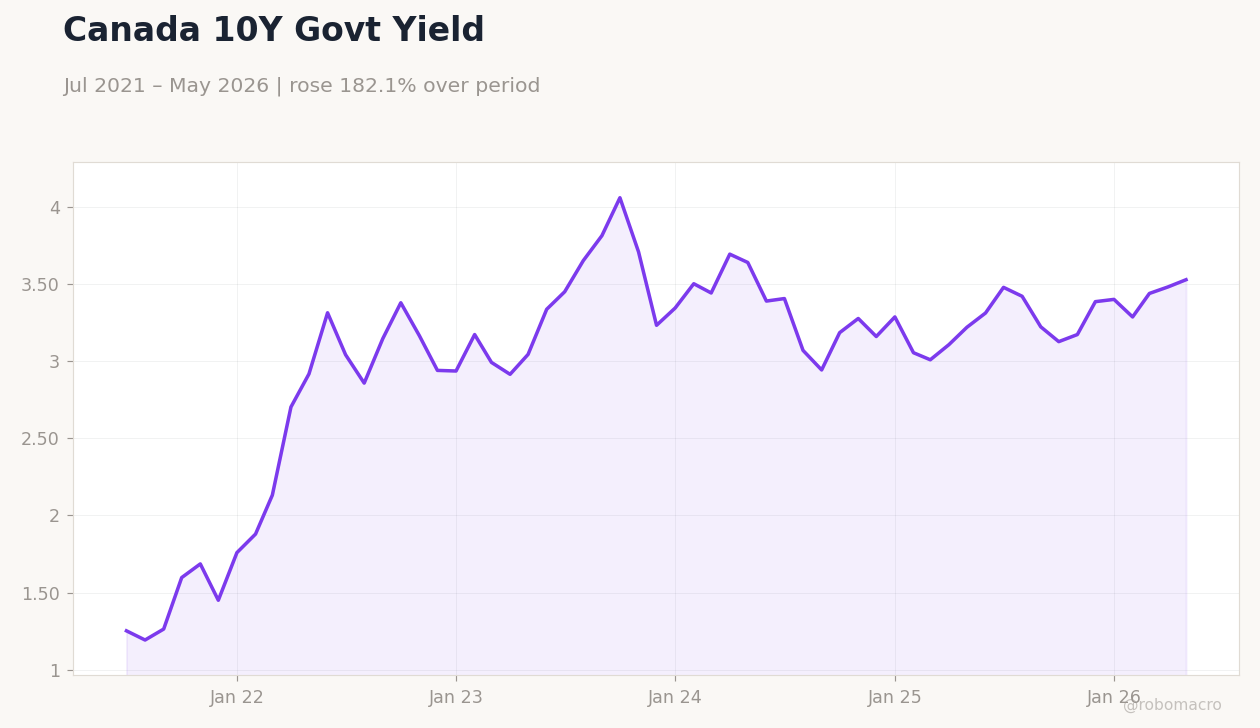

| Canada 10Y Govt Yield | 3.53% | +1.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

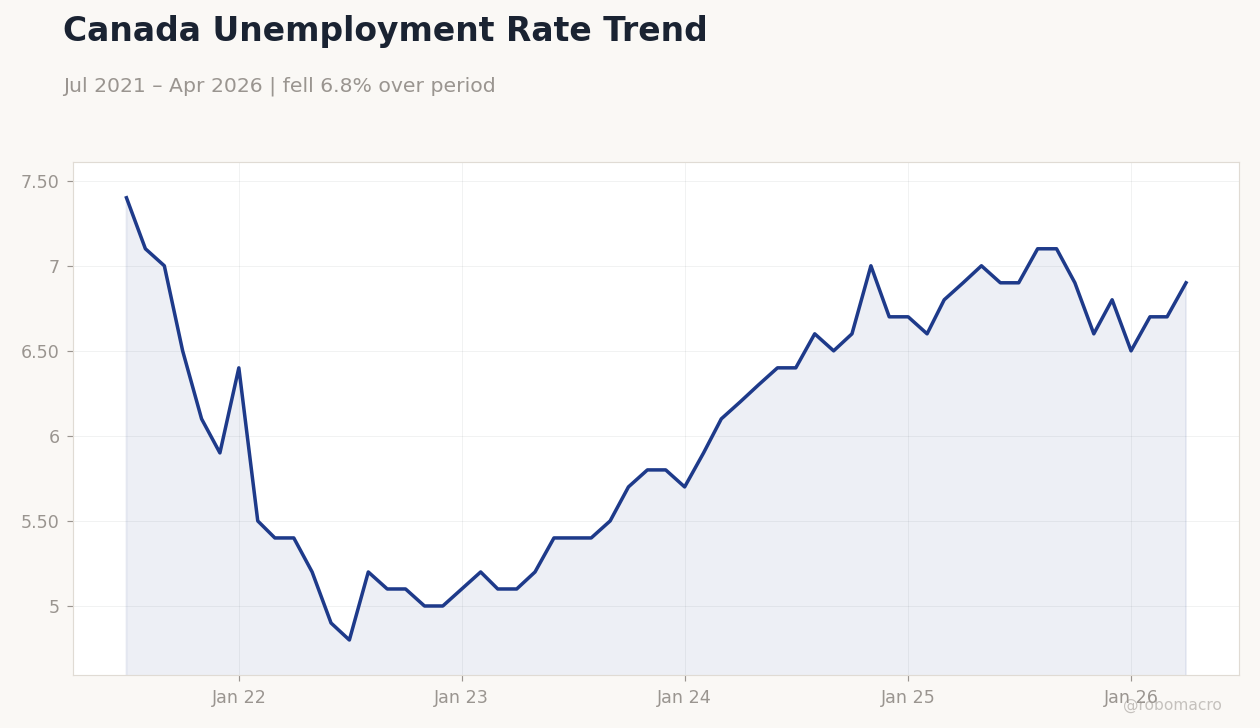

Canada Unemployment Rate Trend | Type: macro_line | Unemployment Rate (%): 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Canada Unemployment Rate Trend | Type: macro_line | Unemployment Rate (%): 6.9 (2026-04-01) | Range: 4.8–7.4 | Trend(6pt): 7.4,5.1,5.8,6.7,6.7,6.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Housing Starts Level | 279,300 | - | 04:15 |

| Wednesday (2026-06-17) | |||

| New Housing Price Index Month-over-Month | -0.40 | - | 04:30 |

| Friday (2026-06-19) | |||

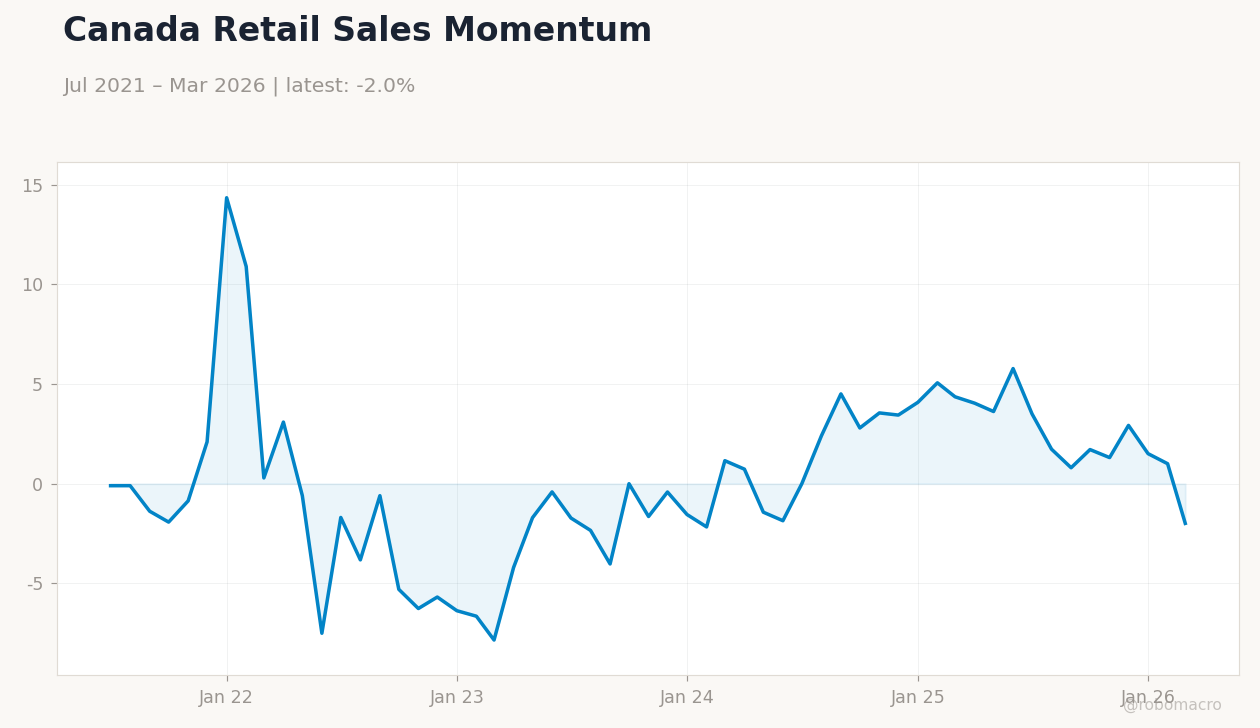

| Retail Sales Excluding Autos Month-over-Month | 1.40 | - | 04:30 |

| Retail Sales Month-over-Month Final | 0.90 | 0.60 | 04:30 |

| Retail Sales Month-over-Month Prel | 0.60 | - | 04:30 |

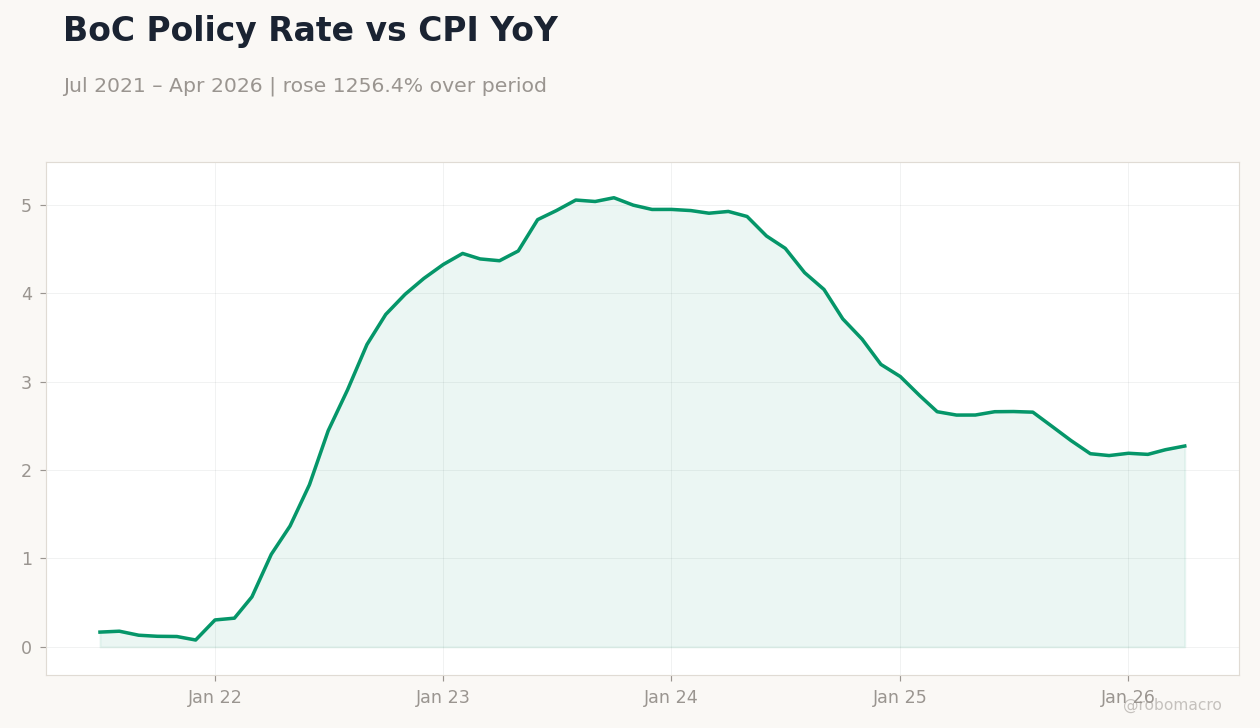

- Bank of Canada maintains policy rate at 2.25% with inflation risks elevated.

- S&P/TSX rises 0.77% while WTI crude falls 5.57% on geopolitical easing.

- USD/CAD edges up 0.03% to 1.40 as 10-year yields climb 1.34% to 3.53%.

Yesterday's Recap

Markets digested the Bank of Canada’s decision to hold the policy rate at 2.25% for the fifth consecutive meeting. The committee highlighted persistent inflation risks despite CPI YoY at 2.32%. S&P/TSX advanced 0.77% to 34,937.90, supported by financials and energy names.

WTI crude dropped sharply to 80.15 amid reports of a US-Iran peace deal that eased supply concerns. Gold surged 3.50% to 4,362.70 as investors sought haven assets. Canada 2-year yields fell 0.20% to 2.25% while the 10-year rose to 3.53%.

USD/CAD settled at 1.40 with limited movement ahead of today’s housing data.

The Day Ahead

Housing Starts Level releases at 04:15 ET with medium impact and no consensus forecast. Traders will assess whether the print confirms ongoing weakness in residential construction. No Bank of Canada speakers or policy minutes are scheduled.

Markets will also monitor retail sales revisions due later in the week for consumption signals. OIS pricing continues to embed limited near-term rate moves. Focus remains on any commentary that clarifies the inflation outlook.

Other Economic Notes

Recent job gains and falling unemployment have tempered recession fears but GDP per capita trends remain weak. Housing affordability pressures persist as mortgage rates stay elevated following the BoC hold. Energy producers face margin compression from lower crude prices despite stable natural gas at 3.05.

Broader trade alignment with US tariffs on Chinese EVs keeps external risks contained. Equity outperformance in banks reflects resilient domestic lending conditions.

Global Macro News

Oil prices plunged after confirmation of a US-Iran peace deal set for signing on June 19. Brent crude fell 5.12% to 82.86, reducing Canada’s terms-of-trade tailwinds. The US dollar retreat supported CAD crosses despite lower energy values.

Bitcoin gained 0.70% to 66,167.12 alongside risk-on equity flows. <i>↓ p.2</i>