Canada Macro Daily(Beta Mode)

Housing Starts Beat Bolsters Hawkish BoC View

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | nan | +nan% |

| USD/CAD | 1.40 | +0.35% |

| EUR/CAD | 1.62 | +0.29% |

| WTI Crude | 76.91 | -4.76% |

| Natural Gas | 3.15 | +0.19% |

| Gold | 4,365.30 | +0.86% |

| Brent Crude | 80.37 | -3.37% |

| Bitcoin | 66,596.05 | +0.46% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

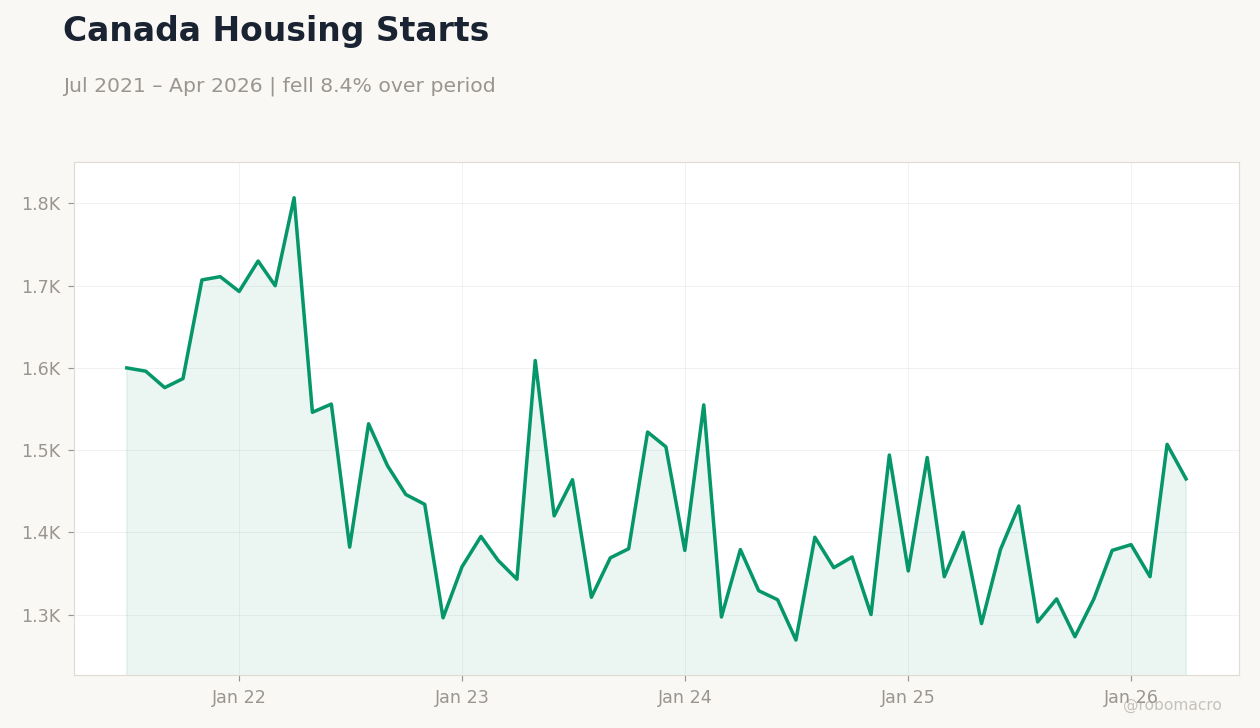

| Housing Starts Level | 278,400 | 255,100 | 261,400 |

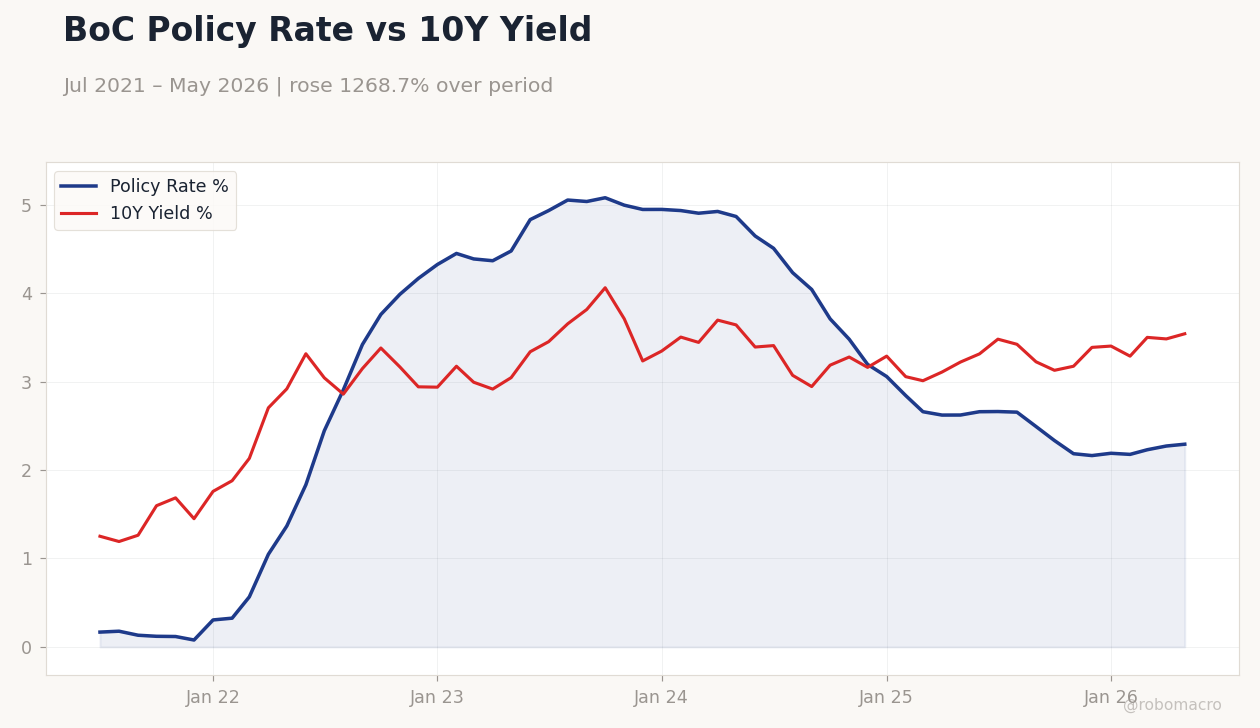

BoC Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.292 (2026-05-01) | Range: 0.078–5.08 | Trend(6pt): 0.1675,3.42,4.996,3.058,2.23,2.292 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

BoC Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.292 (2026-05-01) | Range: 0.078–5.08 | Trend(6pt): 0.1675,3.42,4.996,3.058,2.23,2.292 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-17) | |||

| New Housing Price Index Month-over-Month | -0.40 | -0.10 | 04:30 |

| Friday (2026-06-19) | |||

| Retail Sales Excluding Autos Month-over-Month | 1.40 | 0.80 | 04:30 |

| Retail Sales Month-over-Month Final | 0.90 | 0.60 | 04:30 |

| Retail Sales Month-over-Month Prel | 0.60 | - | 04:30 |

- Housing starts rose to 261400 in May, beating consensus and reinforcing a hawkish BoC tilt.

- USD/CAD climbed 0.35% to 1.40 while WTI crude fell 4.76% to 76.91 on geopolitical easing.

- Canada 10-year yield rose 1.67% to 3.54% as markets priced limited near-term easing.

Yesterday's Recap

Statistics Canada reported May housing starts at 261400, above the 255100 consensus though below the prior 278400 print. The beat aligned with stronger wholesale sales data released earlier in the month. USD/CAD advanced to 1.40 while EUR/CAD gained 0.29% to 1.62.

WTI crude dropped sharply to 76.91 and Brent fell to 80.37 amid reports of a US-Iran peace framework. The S&P/TSX showed no material change while the Canada 2-year yield eased 0.50% to 2.24%. Gold rose 0.86% to 4365.30 as investors adjusted inflation hedges.

Natural gas edged 0.19% higher to 3.15.

The Day Ahead

The New Housing Price Index for May is due tomorrow at 04:30 ET, with consensus calling for a 0.1% decline after April’s 0.4% drop. Retail sales excluding autos and headline retail sales prints follow on Friday, both expected to moderate from prior gains. Markets will watch whether softer housing prices offset the recent starts surprise.

No Bank of Canada speakers are scheduled through the week. Traders will also monitor any updates on the timing of the next Monetary Policy Report.

Other Economic Notes

Wholesale sales exceeded forecasts last month, supporting the view that domestic demand remains resilient despite elevated borrowing costs. Existing-home sales continued to slide, extending the correction in resale activity. Alberta oil production rose 3.1% month-over-month, providing a modest offset to weaker global crude prices.

Tariff adjustments on US dairy imports effective July 1 are unlikely to alter near-term inflation dynamics.

Global Macro News

A US-Iran peace agreement sent oil prices lower across benchmarks, weighing on Canada’s energy export outlook. The US dollar retreated against most majors as safe-haven demand faded. Canadian dollar crosses benefited modestly from the broad USD pullback despite softer crude.

Australian central bank held its cash rate at 4.35%, mirroring the BoC’s cautious stance. <i>↓ p.2</i>