Canada Macro Daily(Beta Mode)

Housing Starts Beat Bolsters Hawkish BoC View

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 35,389.60 | +0.32% |

| USD/CAD | 1.40 | +0.12% |

| EUR/CAD | 1.62 | +0.12% |

| WTI Crude | 75.79 | -0.34% |

| Natural Gas | 3.21 | -0.86% |

| Gold | 4,339.40 | +0.20% |

| Brent Crude | 79.65 | +0.87% |

| Bitcoin | 64,682.91 | -1.40% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Housing Starts Level | 278,400 | 255,100 | 261,400 |

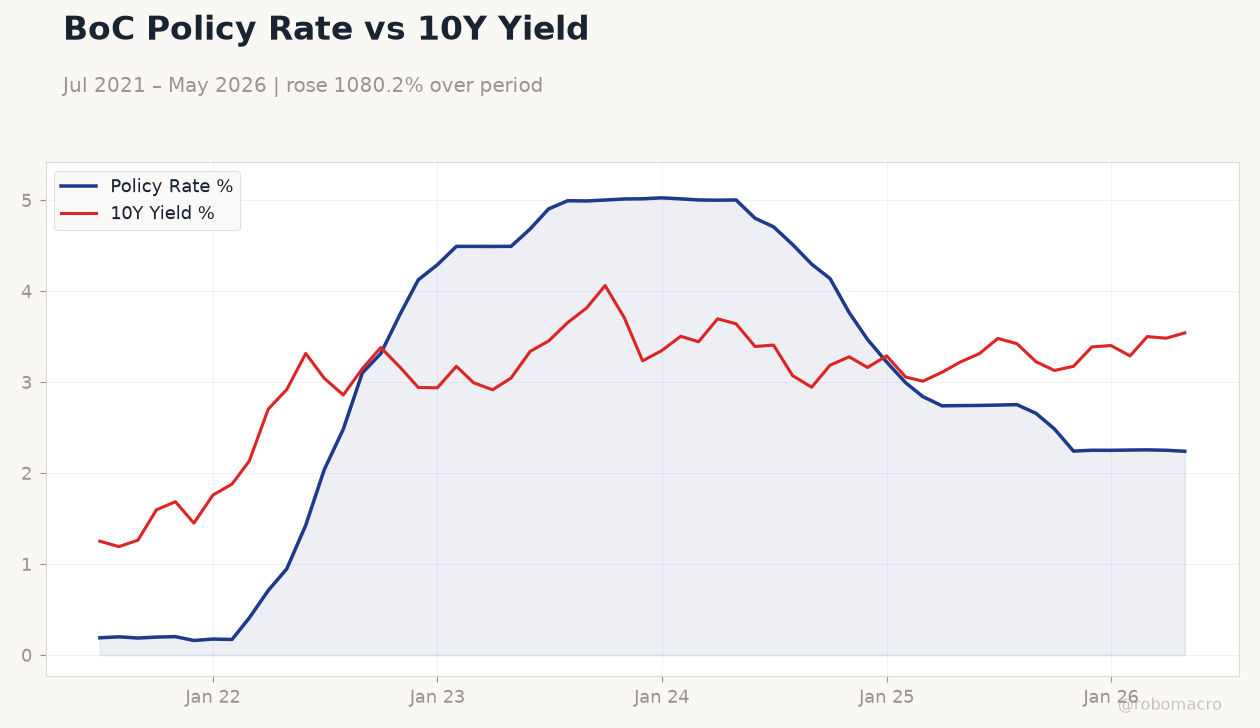

BoC Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

BoC Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| New Housing Price Index Month-over-Month | -0.40 | -0.10 | 04:30 |

| Friday (2026-06-19) | |||

| Retail Sales Excluding Autos Month-over-Month | 1.40 | 0.70 | 04:30 |

| Retail Sales Month-over-Month Final | 0.90 | 0.60 | 04:30 |

| Retail Sales Month-over-Month Prel | 0.60 | - | 04:30 |

- Canada housing starts rose to 261,400 in May, beating consensus forecasts and reinforcing a hawkish BoC stance.

- Bank of Canada held its policy rate at 2.24% as inflation risks persist around the 2.32% CPI reading.

- S&P/TSX gained 0.32% while USD/CAD edged higher to 1.40 amid mixed energy prices.

Yesterday's Recap

May housing starts came in at 261,400, above the 255,100 consensus and signaling resilient construction activity despite higher borrowing costs. The beat aligned with recent commentary that the economy is not clearly in recession, supporting the Bank of Canada’s decision to leave rates unchanged. The S&P/TSX closed 0.32% higher at 35,389.60, led by modest gains in materials.

USD/CAD rose 0.12% to 1.40 as the loonie faced mild pressure from softer oil prices, while the Canada 2-year yield fell 0.50% to 2.24% and the 10-year yield climbed 1.67% to 3.54%. Market pricing continues to reflect limited near-term easing expectations following the data.

The Day Ahead

Statistics Canada will release the New Housing Price Index for May at 8:30 ET, with consensus calling for a 0.1% monthly decline after April’s 0.4% drop. Attention will then shift to Friday’s retail sales figures, including the ex-autos component, which are expected to show moderation from prior strength. Bank of Canada speakers are absent from the calendar, leaving markets to focus on incoming data for clues on the timing of any policy shift.

A soft housing price print could temper recent hawkish sentiment priced into CAD crosses.

Other Economic Notes

Persistent shelter cost pressures and uneven goods deflation keep core inflation measures near target, complicating the Bank of Canada’s communication around the appropriate path for rates. Housing market resilience contrasts with softening retail momentum, highlighting divergent sectoral trends that policymakers must weigh. Energy export revenues remain sensitive to global oil price swings, adding volatility to the CAD outlook even as domestic demand shows signs of stabilization.

Global Macro News

WTI crude fell 0.34% to 75.79 while Brent rose 0.87% to 79.65, reflecting uneven supply recovery expectations after recent geopolitical developments. Natural gas declined 0.86% amid mild weather forecasts that could curb North American demand. The broader USD remained supported against G10 peers as Fed speakers signaled steady policy, lifting USD/CAD.

<i>↓ p.2</i>