Canada Macro Daily(Beta Mode)

Housing Starts Beat, Retail Sales Loom

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,969.30 | -0.44% |

| USD/CAD | 1.42 | +0.37% |

| EUR/CAD | 1.62 | -0.04% |

| WTI Crude | 76.08 | -0.68% |

| Natural Gas | 3.22 | -0.25% |

| Gold | 4,161.00 | -1.49% |

| Brent Crude | 79.91 | +0.08% |

| Bitcoin | 62,578.26 | -0.51% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Housing Starts Level | 278,400 | 255,100 | 261,400 |

| New Housing Price Index Month-over-Month | -0.40 | -0.10 | -0.30 |

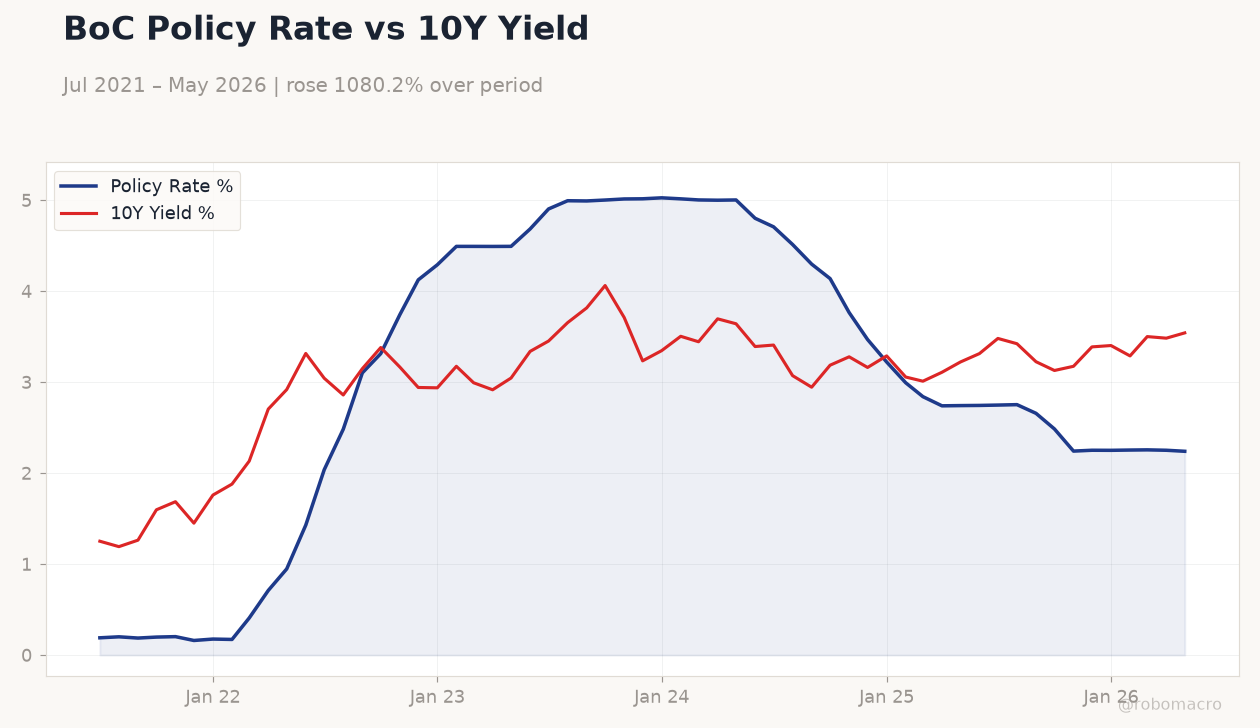

BoC Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

BoC Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Retail Sales Excluding Autos Month-over-Month | 1.40 | 0.70 | 04:30 |

| Retail Sales Month-over-Month Final | 0.90 | 0.60 | 04:30 |

| Retail Sales Month-over-Month Prel | 0.60 | - | 04:30 |

- Housing starts rose to 261,400 in May, beating consensus of 255,100, while new housing prices fell 0.3% month-over-month.

- S&P/TSX declined 0.44% to 34,969.30 as USD/CAD rose 0.37% to 1.42 amid softer energy prices.

- Bank of Canada policy rate stands at 2.24% with CPI at 2.32% year-over-year, signaling steady policy amid demographic pressures.

Yesterday's Recap

Canadian housing starts reached 261,400 in May, exceeding the 255,100 consensus and signaling modest construction resilience despite higher borrowing costs. The new housing price index declined 0.3% month-over-month, steeper than the -0.1% consensus forecast and extending the prior -0.4% drop. Equity markets closed lower with the S&P/TSX falling 0.44% to 34,969.30 while the Canadian dollar weakened, pushing USD/CAD to 1.42.

Government bond yields diverged as the 2-year yield slipped 0.50% to 2.24% and the 10-year yield climbed 1.67% to 3.54%. WTI crude fell 0.68% to 76.08 and natural gas eased 0.25% to 3.22, weighing on energy-linked sectors. Broader risk sentiment remained cautious ahead of today's retail sales prints.

The Day Ahead

Statistics Canada will release May retail sales excluding autos at 4:30 ET, with consensus pointing to a 0.7% month-over-month gain after April's 1.4% rise. Headline retail sales are expected to advance 0.6% on a final basis following the preliminary 0.6% print. Markets will parse these figures for evidence of consumer resilience ahead of the next Bank of Canada decision.

No major speeches are scheduled, leaving data as the primary domestic driver. Traders will also monitor cross-border flows given ongoing US trade policy uncertainty.

Other Economic Notes

Canada's economy faces a demographic recession as population aging and slower immigration weigh on labor supply and housing demand. Recent Bank of Canada analysis highlights persistent financing constraints for Indigenous-owned businesses, limiting broader credit expansion. Government bond curves steepened modestly, reflecting expectations that inflation at 2.32% will remain contained without aggressive tightening.

Energy export revenues face headwinds from lower oil prices despite stable Brent at 79.91.

Global Macro News

A US-Iran accord reopening the Strait of Hormuz drove oil prices lower, with WTI dropping to 76.08 and pressuring the Canadian dollar. <i>↓ p.2</i>