Canada Macro Daily(Beta Mode)

CPI Data Looms Over Steady BoC Policy

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,968.90 | -0.00% |

| USD/CAD | 1.42 | +0.22% |

| EUR/CAD | 1.62 | +0.19% |

| WTI Crude | 75.41 | -1.55% |

| Natural Gas | 3.29 | +1.89% |

| Gold | 4,222.20 | -0.04% |

| Brent Crude | 79.28 | -0.71% |

| Bitcoin | 64,561.92 | +2.09% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

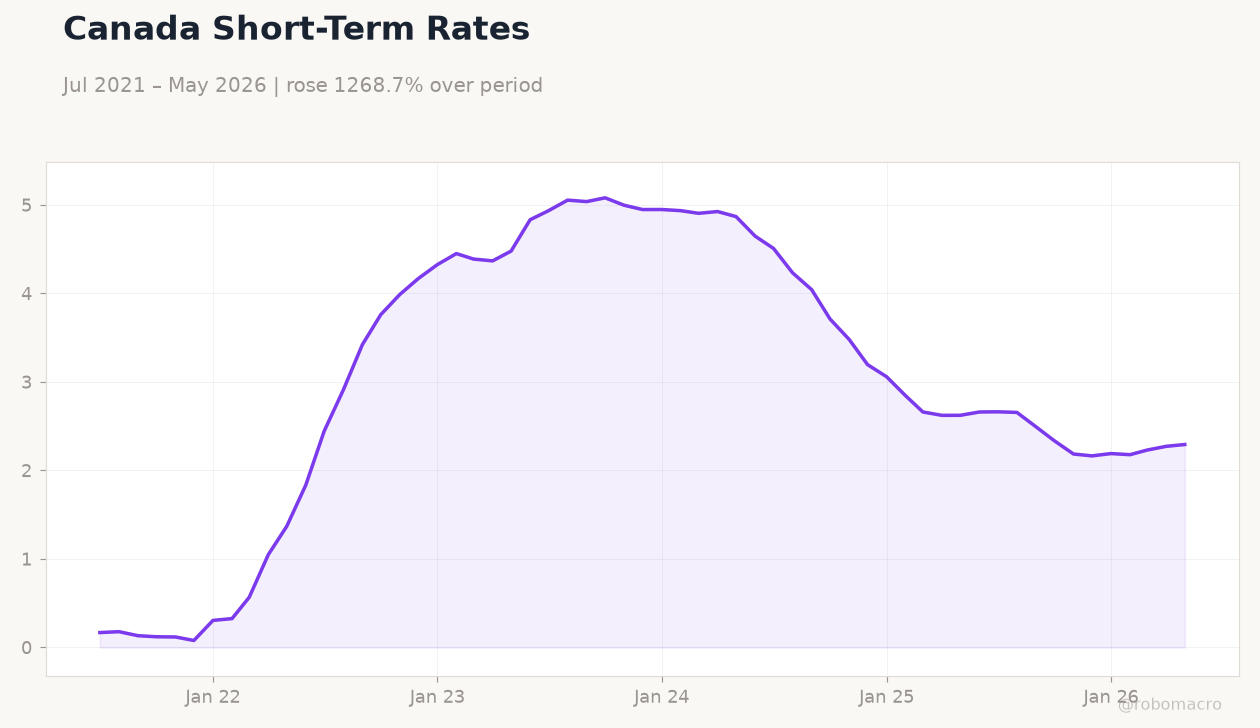

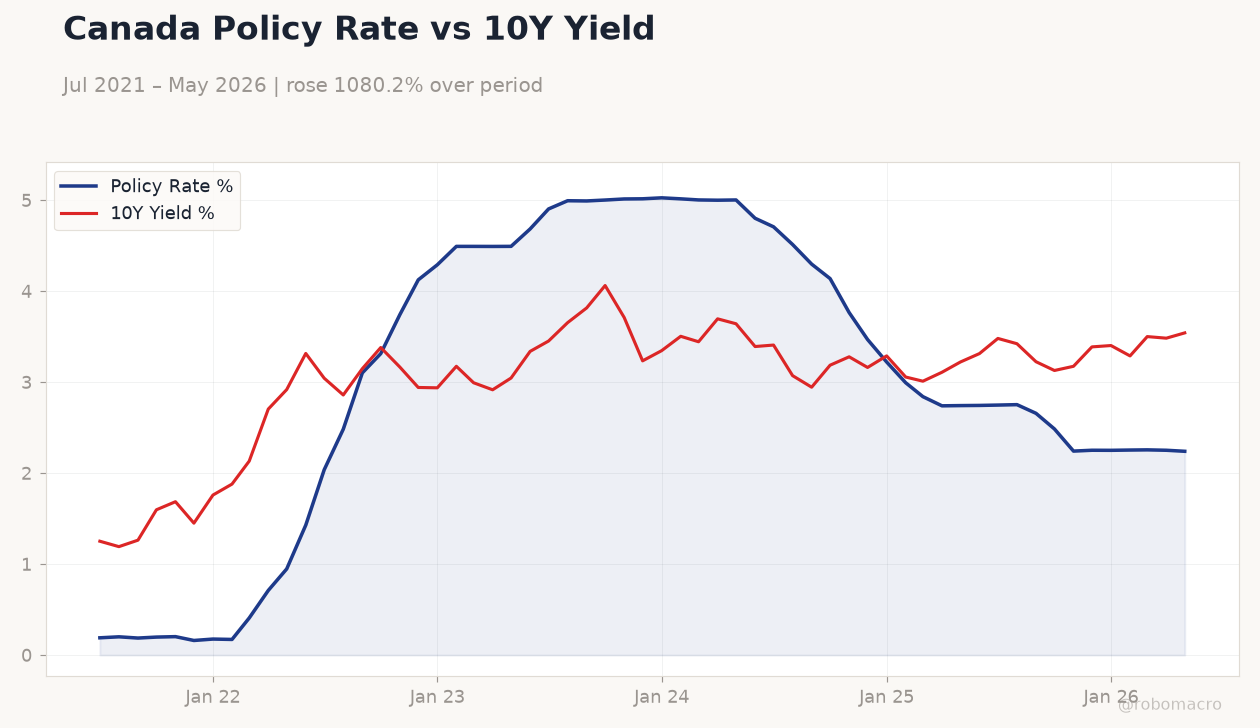

Canada Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

Canada Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.80 | 3 | 04:30 |

| Core Inflation Rate Year-over-Year | 2.10 | - | 04:30 |

| Inflation Rate Month-over-Month | 0.40 | 0.80 | 04:30 |

| Tuesday (2026-06-23) | |||

| BoC Gov Macklem Speech | - | - | 15:59 |

- Canada CPI YoY expected at 3.0% versus prior 2.8%, with month-over-month rising to 0.8%.

- S&P/TSX closed flat at 34,968.90 while USD/CAD climbed 0.22% to 1.42 amid softer oil.

- BoC policy rate remains at 2.24% with no immediate change signaled before Macklem speech.

Yesterday's Recap

Markets digested the absence of data releases on June 21 with limited movement across Canadian assets. The S&P/TSX ended unchanged at 34,968.90 as energy and financials offset modest gains elsewhere. USD/CAD advanced 0.22% to 1.42, reflecting broad U.S.

dollar strength and a 1.55% drop in WTI crude to 75.41. Canada 2-year yields eased 0.50% to 2.24% while the 10-year yield rose 1.67% to 3.54%. Natural gas gained 1.89% to 3.29 and gold held near 4,222.20.

Reports highlighted ongoing demographic pressures weighing on household formation and consumption. Traders positioned ahead of today’s inflation release with little conviction in either direction.

The Day Ahead

Statistics Canada releases May CPI at 04:30 ET with year-over-year expected to print at 3.0% and core measures also due. Month-over-month inflation is forecast at 0.8% after 0.4% prior. BoC Governor Tiff Macklem speaks at 15:59 ET on June 23, providing the first public comments since the latest hold decision.

Markets will parse any signals on the timing of future easing amid mixed growth data. Energy prices and CAD crosses will react to the inflation outcome and Macklem tone. No other high-impact Canadian releases appear on the immediate calendar.

Other Economic Notes

TD Economics noted Canada avoided a dire outlook despite recent GDP contraction, citing resilient domestic demand. A 10% temporary tariff on imported canned vegetables took effect to shield local producers and processors. Demographic trends continue to constrain labor-force growth and housing demand.

Retail sales weakness and softer oil prices added to downside risks for near-term activity. Broader fiscal support remains limited as Ottawa focuses on tariff mitigation rather than new stimulus.

Global Macro News

U.S. AI-related capital spending continues to lift core inflation measures and may keep global rates higher for longer. Oil prices eased on reports of potential Iran ceasefire, pressuring CAD and Canadian energy equities.

<i>↓ p.2</i>