Canada Macro Daily(Beta Mode)

CPI Surges to 3.2%, BoC Holds Amid Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,927.40 | -0.21% |

| USD/CAD | 1.42 | +0.46% |

| EUR/CAD | 1.61 | -0.25% |

| WTI Crude | 71.47 | -2.38% |

| Natural Gas | 3.23 | +2.73% |

| Gold | 4,061.70 | -1.65% |

| Brent Crude | 75.22 | -2.41% |

| Bitcoin | 62,542.45 | -0.20% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

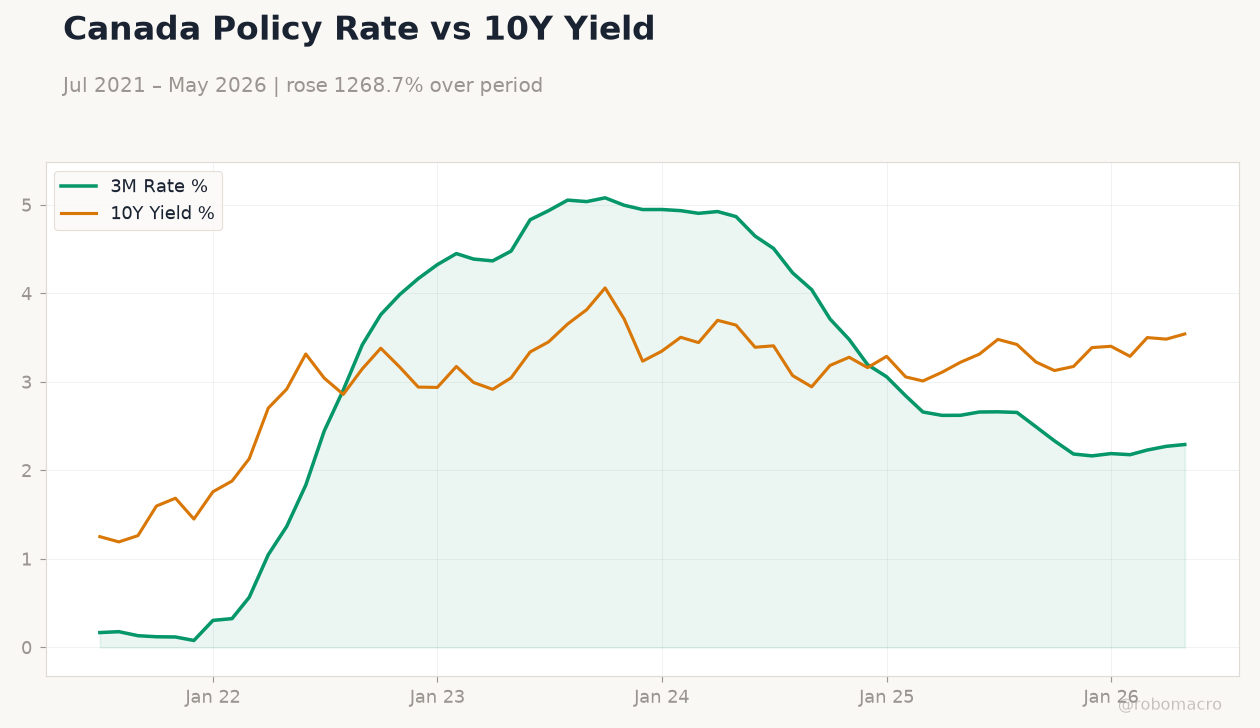

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Year-over-Year | 2.80 | 3 | 3.20 |

| Core Inflation Rate Year-over-Year | 2.10 | - | 2.20 |

| Inflation Rate Month-over-Month | 0.40 | 0.80 | 1 |

| BoC Gov Macklem Speech | - | - | - |

Canada Core CPI YoY | Type: macro_line | Core CPI YoY %: 2.957 (2026-05-01) | Range: 2.673–6.624 | Trend(6pt): 4.211,6.624,4.018,3.283,2.988,2.957

Canada Core CPI YoY | Type: macro_line | Core CPI YoY %: 2.957 (2026-05-01) | Range: 2.673–6.624 | Trend(6pt): 4.211,6.624,4.018,3.283,2.988,2.957

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Wednesday (2026-06-24) | |||

| BoC Rogers Speech | - | - | 03:15 |

- May CPI rose to 3.2% y/y, exceeding consensus and lifting CAD volatility.

- BoC policy rate steady at 2.24% with markets pricing limited near-term easing.

- TSX fell 0.21% while USD/CAD climbed 0.46% to 1.42 on oil weakness.

Yesterday's Recap

Canada’s May inflation data surprised to the upside, with headline CPI reaching 3.2% y/y against a 3% consensus and core CPI printing 2.2% y/y. Month-over-month CPI jumped 1.0%, well above expectations, prompting immediate repricing in front-end yields. The S&P/TSX closed 0.21% lower at 34,927.40 while USD/CAD rose 0.46% to 1.42 as falling WTI crude weighed on the currency.

Canada 2-year yields eased 0.50% to 2.24% but the 10-year yield climbed 1.67% to 3.54%. Governor Macklem highlighted moderate growth ahead and warned Canada could be sideswiped by widening global imbalances. No rate decision occurred, leaving the policy rate at the verified 2.24% level.

The Day Ahead

Senior Deputy Governor Rogers is scheduled to speak at 03:15 ET, with markets watching for any signals on inflation persistence. No other high-impact Canadian data releases are listed for the session. Traders will monitor oil and natural gas price action given their direct influence on CAD crosses.

Any dovish tilt in Rogers’ remarks could reopen modest easing bets for later in the year. Broader focus remains on how the recent CPI overshoot alters the BoC’s reaction function.

Other Economic Notes

Recent CPI strength has tempered expectations for near-term BoC cuts despite verified policy rate at 2.24%. Housing and retail indicators continue to point to subdued domestic demand. Energy sector capex remains supportive for WTI-linked revenues even as prices soften.

Labor-market data show resilience that aligns with Macklem’s moderate-growth outlook. Global trade tensions add downside risks to the export-oriented economy.

Global Macro News

WTI crude fell 2.38% to 71.47, pressuring CAD and widening the USD/CAD spread. Natural gas gained 2.73% to 3.23 amid shifting weather forecasts. Gold declined 1.65% to 4,061.70 as risk appetite improved elsewhere.

The euro weakened against CAD while Bitcoin edged 0.20% lower. US rate-hike bets intensified, amplifying pressure on the loonie through higher US yields. <i>↓ p.2</i>