Canada Macro Daily(Beta Mode)

BoC Holds Steady After CPI Overshoot

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,736.10 | -0.55% |

| USD/CAD | 1.42 | +0.25% |

| EUR/CAD | 1.61 | -0.14% |

| WTI Crude | 69.71 | -0.90% |

| Natural Gas | 3.31 | +2.86% |

| Gold | 3,991.60 | +0.03% |

| Brent Crude | 73.26 | -0.65% |

| Bitcoin | 61,231.52 | +0.39% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

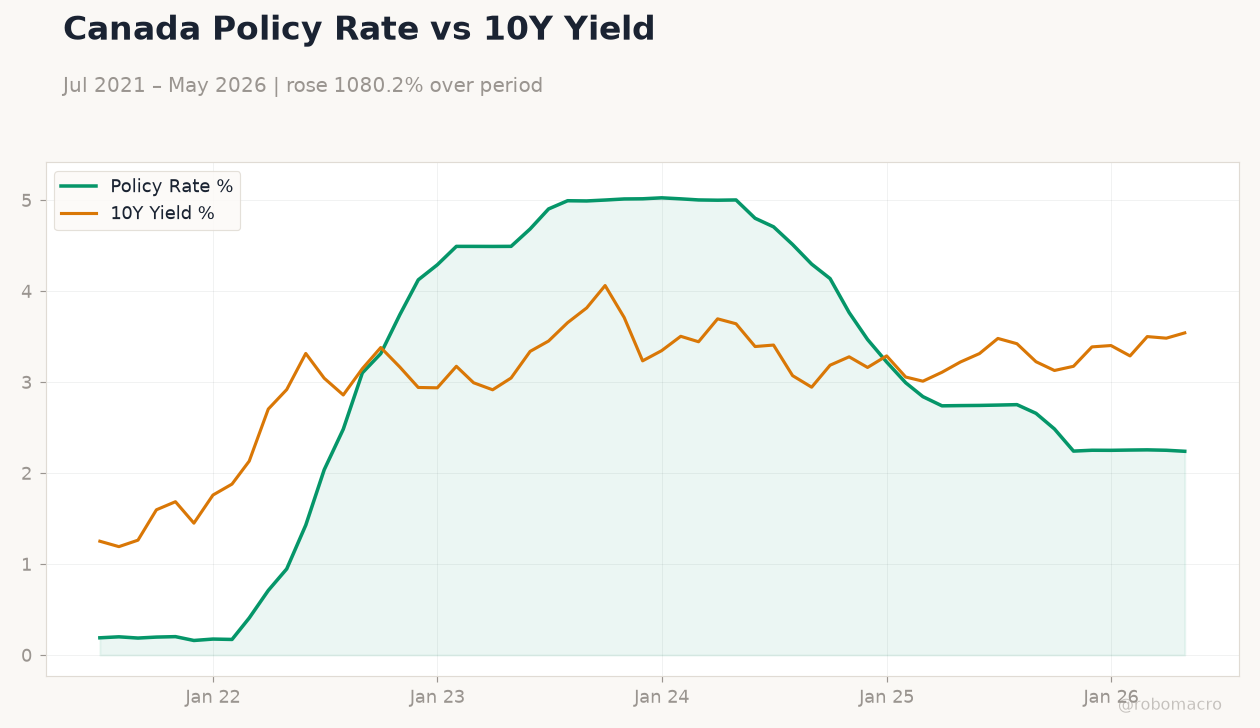

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

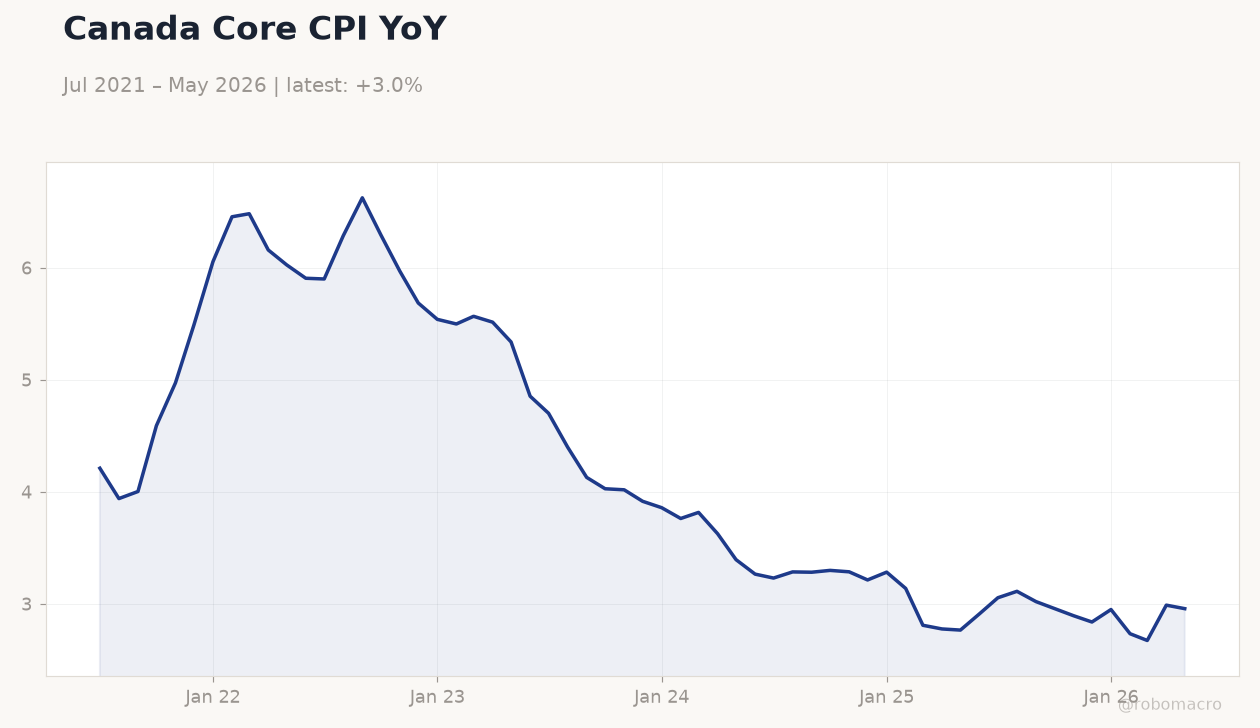

| Inflation Rate Year-over-Year | 2.80 | 3 | 3.20 |

| Core Inflation Rate Year-over-Year | 2.10 | - | 2.20 |

| Inflation Rate Month-over-Month | 0.40 | 0.80 | 1 |

| BoC Gov Macklem Speech | - | - | - |

| BoC Rogers Speech | - | - | - |

Canada Core CPI YoY | Type: macro_line | YoY %: 2.957 (2026-05-01) | Range: 2.673–6.624 | Trend(6pt): 4.211,6.624,4.018,3.283,2.988,2.957

Canada Core CPI YoY | Type: macro_line | YoY %: 2.957 (2026-05-01) | Range: 2.673–6.624 | Trend(6pt): 4.211,6.624,4.018,3.283,2.988,2.957

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Canada CPI YoY rose to 3.2% in May, above 3.0% consensus, while core reached 2.2%.

- S&P/TSX fell 0.55% to 34,736.10 as WTI Crude dropped 0.90% to 69.71.

- USD/CAD climbed 0.25% to 1.42 amid higher inflation and steady policy signals.

Yesterday's Recap

Statistics Canada reported May inflation data showing CPI YoY at 3.2%, exceeding the 3.0% consensus and prior 2.8% print, with month-over-month inflation at 1.0% versus 0.8% expected. Core CPI YoY edged up to 2.2%. Governor Macklem and Deputy Governor Rogers both delivered speeches emphasizing data dependence without signaling immediate policy shifts.

The S&P/TSX Composite declined 0.55% to close at 34,736.10 while the 2-year Government of Canada yield fell 0.50% to 2.24%, matching the current BoC policy rate. USD/CAD advanced 0.25% to 1.42 as higher inflation readings tempered cut expectations. Natural Gas gained 2.86% to 3.31 while Brent Crude eased 0.65% to 73.26.

Markets absorbed the hotter prints without altering the view that the BoC remains on hold.

The Day Ahead

The domestic calendar is empty today, leaving markets to focus on external developments and follow-through from yesterday’s inflation release. Attention will turn to any follow-up commentary from Governing Council members on the implications of the 3.2% CPI print. Energy traders will monitor WTI Crude and Natural Gas for direction ahead of weekend positioning.

CAD crosses may respond to broader USD moves and any shifts in rate-differential pricing. Participants will also watch for updates on Government of Canada bond auctions scheduled later in the week.

Other Economic Notes

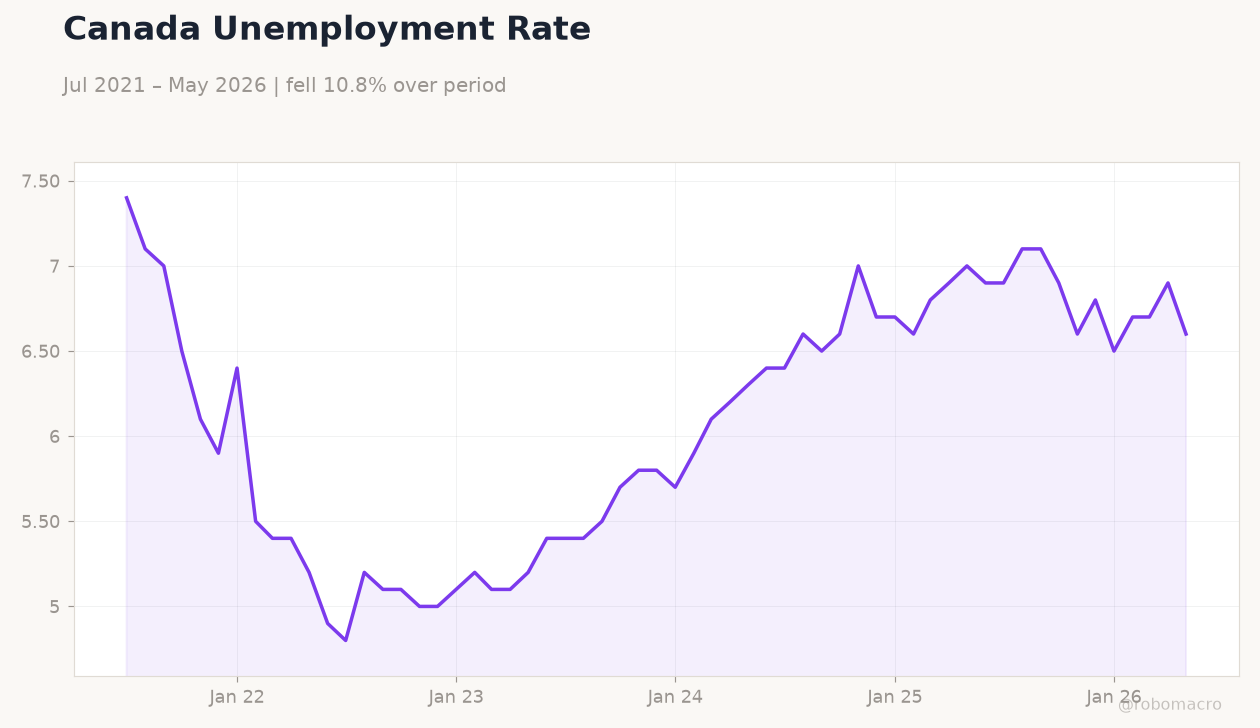

Recent data continue to show resilient consumer prices alongside subdued growth, creating a narrow path for policy. The 10-year yield rose 1.67% to 3.54%, steepening the curve and reflecting inflation concerns. Housing and retail indicators remain soft, yet officials have avoided recession terminology.

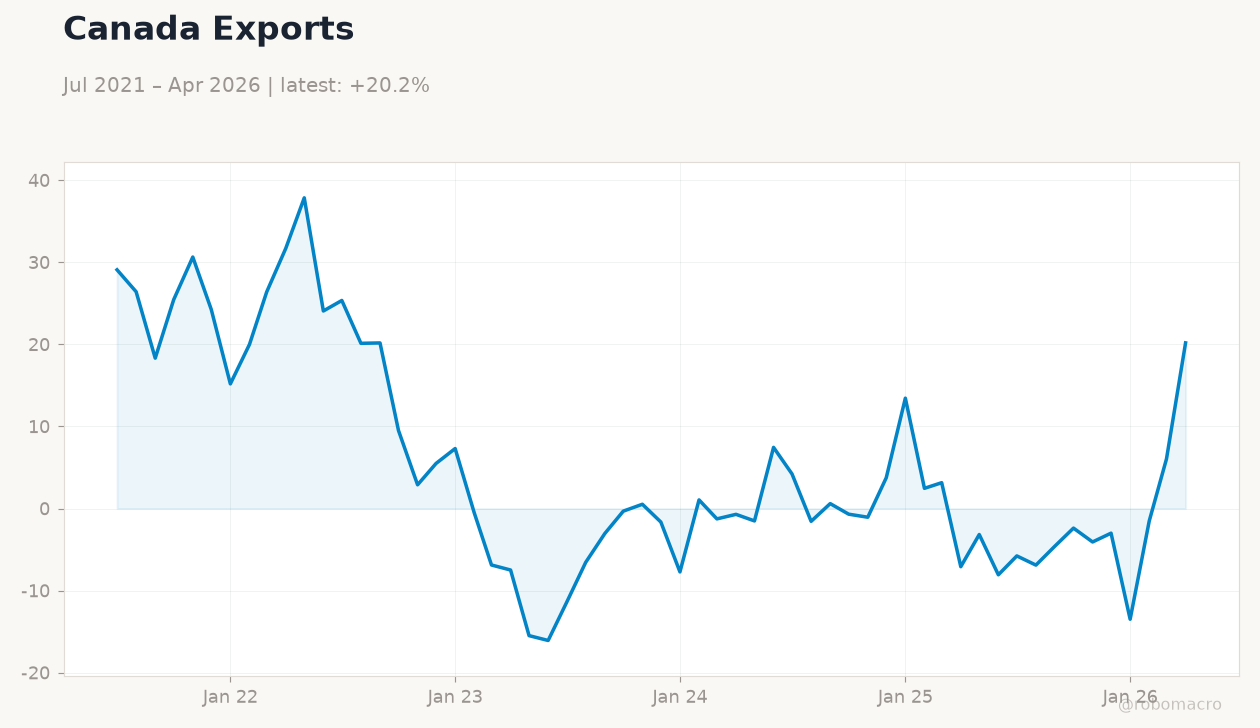

Energy markets stay central to the outlook given Canada’s export exposure and the recent pullback in WTI to 69.71.

Global Macro News

Oil prices fell toward pre-conflict levels as supply concerns eased in the Persian Gulf, pressuring Canadian energy names. The U.S. dollar held firmer on persistent rate-hike expectations, supporting USD/CAD at 1.42.

<i>↓ p.2</i>