Canada Macro Daily(Beta Mode)

Canada GDP Rebound Eyed Ahead of Macklem Speech

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,980.00 | +0.37% |

| USD/CAD | 1.42 | +0.03% |

| EUR/CAD | 1.62 | +0.38% |

| WTI Crude | 70.02 | +1.14% |

| Natural Gas | 3.28 | +1.42% |

| Gold | 4,045.90 | -0.80% |

| Brent Crude | 73.14 | +1.60% |

| Bitcoin | 59,751.04 | +0.37% |

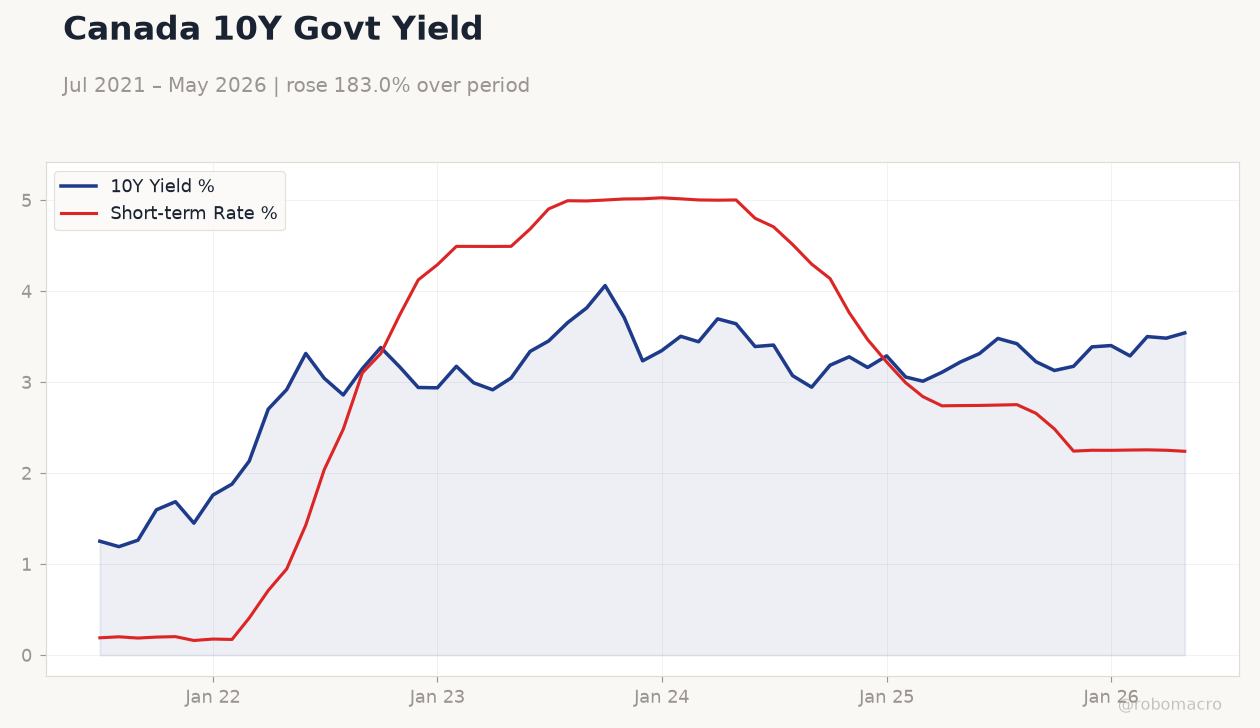

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542 | Short-term Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24

Canada 10Y Govt Yield | Type: macro_line | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.251,3.148,3.711,3.289,3.501,3.542 | Short-term Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.1898,3.102,5.014,3.222,2.256,2.24

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Tuesday (2026-06-30) | |||

| GDP Month-over-Month | -0.10 | 0.40 | 04:30 |

| GDP Month-over-Month Prel | 0.40 | - | 04:30 |

| Wednesday (2026-07-01) | |||

| BoC Gov Macklem Speech | - | - | 05:00 |

| Thursday (2026-07-02) | |||

| S&P Global Manufacturing PMI Index | - | - | 05:30 |

- June GDP expected to rebound 0.4% m/m after May contraction, supporting BoC easing path at 2.24% policy rate.

- TSX rose 0.37% to 34,980 while USD/CAD edged 0.03% higher to 1.42 amid mixed energy gains.

- Canada CPI at 2.32% y/y keeps focus on headline inflation as BoC weighs further cuts.

Yesterday's Recap

Canadian markets posted modest gains on June 28 with the S&P/TSX closing at 34,980, up 0.37%, led by energy and financial sectors. USD/CAD finished at 1.42 after a 0.03% advance while EUR/CAD climbed 0.38% to 1.62. WTI crude settled at 70.02, up 1.14%, and natural gas rose 1.42% to 3.28.

Canada 2-year yields fell 0.50% to 2.24% while the 10-year yield rose 1.67% to 3.54%. Gold declined 0.80% to 4,045.90 as Bitcoin gained 0.37% to 59,751. No major data releases occurred, leaving price action driven by positioning ahead of the June GDP print.

The Day Ahead

June GDP month-over-month is scheduled for release at 04:30 ET on June 30 with consensus at 0.4% following the prior -0.1% reading. A preliminary GDP estimate will also print at the same time. Bank of Canada Governor Tiff Macklem is set to speak at 05:00 ET on July 1, providing fresh forward guidance.

The S&P Global Manufacturing PMI follows on July 2 at 05:30 ET. Markets will parse the GDP outcome for confirmation of a second-quarter rebound that could influence July policy probabilities.

Other Economic Notes

Economists have lowered 2026 growth forecasts after early-year weakness and renewed recession concerns. Canada’s demographic trends are producing slower labor-force expansion that weighs on potential output. Wage gains have failed to alter inflation outlooks according to Rosenberg, keeping pressure on the BoC to monitor headline prints closely.

Housing and consumer sectors remain sensitive to the current 2.24% policy rate amid persistent affordability challenges.

Global Macro News

Oil prices posted gains with Brent up 1.60% to 73.14, supporting CAD crosses despite broader USD strength. US-Iran developments and shifting Fed expectations continue to influence CAD trading ranges. Global equity sentiment lifted risk assets including the TSX while commodity currencies benefited from energy rebounds.

Canadian dollar movements remain capped by softer US data and domestic growth concerns. International investors monitor BoC communications for divergence from other G10 central banks.