Canada Macro Daily(Beta Mode)

GDP Beat Bolsters Canada Outlook as Macklem Speaks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,857.00 | +0.10% |

| USD/CAD | 1.42 | +0.14% |

| EUR/CAD | 1.62 | -0.17% |

| WTI Crude | 68.97 | -0.76% |

| Natural Gas | 3.23 | -1.34% |

| Gold | 4,040.90 | +0.45% |

| Brent Crude | 72.32 | -0.82% |

| Bitcoin | 58,580.00 | +0.04% |

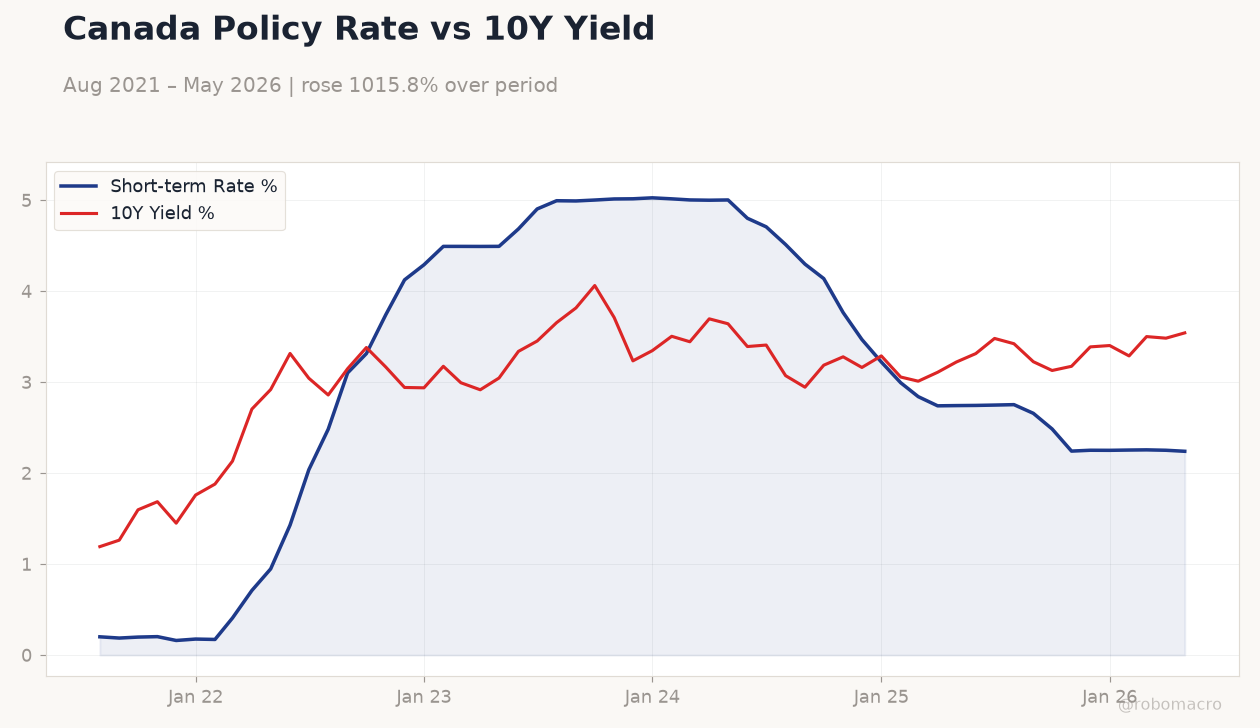

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| GDP Month-over-Month | -0.10 | 0.40 | 0.50 |

| GDP Month-over-Month Prel | 0.40 | - | 0.10 |

Canada Policy Rate vs 10Y Yield | Type: macro_line | Short-term Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.2007,3.314,5.015,2.993,2.251,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.192,3.381,3.234,3.056,3.483,3.542

Canada Policy Rate vs 10Y Yield | Type: macro_line | Short-term Rate %: 2.24 (2026-05-01) | Range: 0.1604–5.026 | Trend(6pt): 0.2007,3.314,5.015,2.993,2.251,2.24 | 10Y Yield %: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.192,3.381,3.234,3.056,3.483,3.542

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| BoC Gov Macklem Speech | - | - | 05:00 |

| Thursday (2026-07-02) | |||

| S&P Global Manufacturing PMI Index | - | - | 05:30 |

- Canada GDP rose 0.5% m/m in April, topping the 0.4% consensus and reversing March weakness.

- USD/CAD climbed to 1.42 while the S&P/TSX edged up 0.10% amid mixed yields.

- BoC Governor Macklem speaks today ahead of tomorrow’s manufacturing PMI release.

Yesterday's Recap

Statistics Canada reported April GDP expanded 0.5% month-over-month, beating consensus and marking the strongest monthly gain in nine months. The preliminary GDP reading also printed at 0.1%. The Canadian dollar strengthened on the data, pushing USD/CAD to 1.42.

The S&P/TSX closed 0.10% higher at 34,857. Canada 2-year yields fell 0.50% to 2.24% while the 10-year yield rose 1.67% to 3.54%. WTI crude declined 0.76% to 68.97 and natural gas fell 1.34% to 3.23.

Markets interpreted the GDP beat as evidence of a firmer second-quarter start after six months of stagnation.

The Day Ahead

Governor Macklem delivers a high-impact speech at 05:00 ET that will shape rate expectations. Markets will parse any fresh comments on inflation persistence and labor-market slack. Tomorrow’s S&P Global Manufacturing PMI is expected to show whether factory momentum is holding after the GDP rebound.

No other major Canadian data releases are scheduled for the session. Traders will also monitor USD/CAD reaction to any hawkish signals from the speech.

Other Economic Notes

The verified BoC policy rate stands at 2.24% while CPI inflation runs at 2.32% year-over-year. Stronger oil-sands output and resilient consumer spending are supporting the second-quarter rebound narrative. Housing starts and retail sales data continue to point to underlying demand that may keep the Bank of Canada on hold longer than previously priced.

Tariff reviews on U.S. steel remain a background risk for trade-sensitive sectors.

Global Macro News

Oil prices extended losses on softer China demand signals, pressuring CAD crosses. The ECB faces renewed debate over a possible September hike according to Apollo’s Torsten Slok. German inflation cooled more than expected in June, reflecting the broader retreat in energy costs.

The Fed’s hawkish tone lifted the U.S. dollar and weighed on USD/CAD-sensitive flows. <i>↓ p.2</i>