Canada Macro Daily(Beta Mode)

Macklem Flags Above-Target Inflation

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,857.00 | +0.10% |

| USD/CAD | 1.42 | +0.04% |

| EUR/CAD | 1.62 | -0.09% |

| WTI Crude | 67.25 | -1.94% |

| Natural Gas | 3.17 | -1.65% |

| Gold | 4,078.00 | +0.24% |

| Brent Crude | 70.37 | -1.68% |

| Bitcoin | 61,215.16 | +2.02% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoC Gov Macklem Speech | - | - | - |

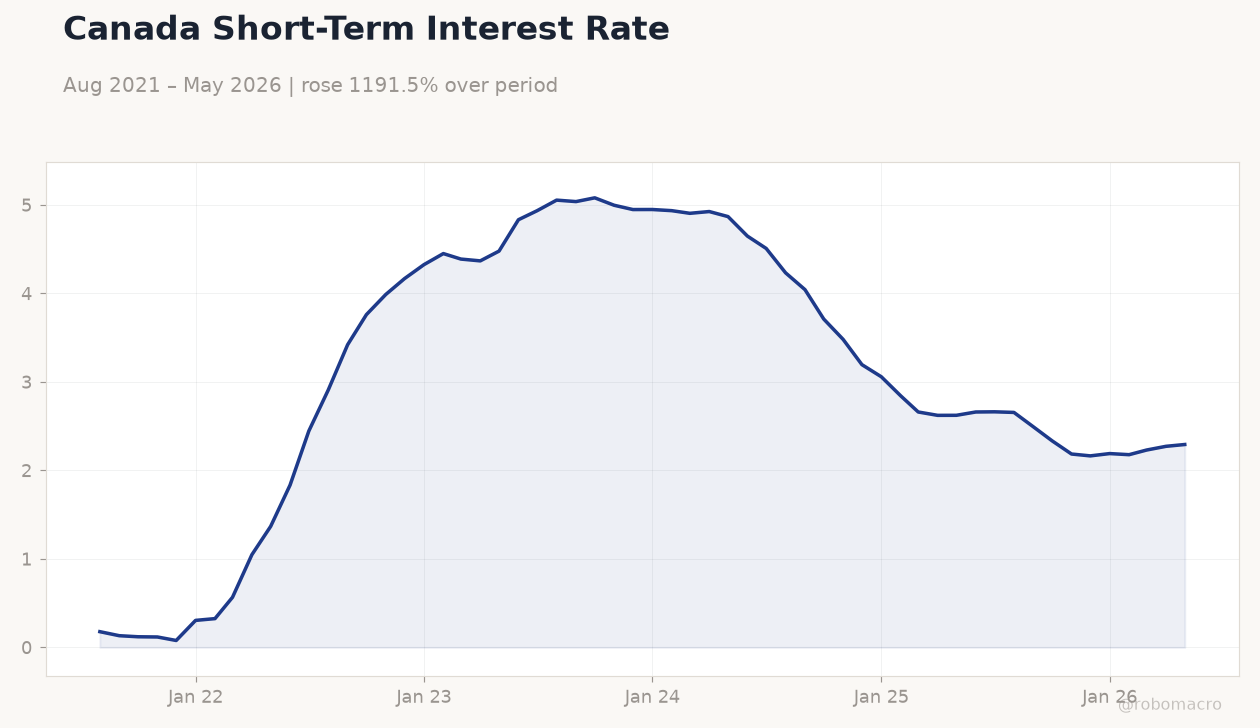

Canada Short-Term Interest Rate | Type: macro_line | Rate %: 2.292 (2026-05-01) | Range: 0.078–5.08 | Trend(6pt): 0.1775,3.76,4.947,2.842,2.272,2.292

Canada Short-Term Interest Rate | Type: macro_line | Rate %: 2.292 (2026-05-01) | Range: 0.078–5.08 | Trend(6pt): 0.1775,3.76,4.947,2.842,2.272,2.292

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Index | - | - | 05:30 |

- BoC Governor Macklem states inflation remains clearly above target while endorsing current policy stance.

- S&P/TSX edges up 0.10% to 34,857 as energy weakness offsets holiday sentiment.

- Canada 2-year yield falls 0.50% to 2.24% while 10-year yield rises 1.67% to 3.54%.

Yesterday's Recap

Governor Macklem delivered a high-impact speech on Canada Day, emphasizing that inflation sits clearly above the 2% target and that the Bank remains content with its current 2.24% policy rate. He noted balanced risks around AI-driven productivity gains and flagged excess imbalances in the shifting financial system. Markets responded with the S&P/TSX rising 0.10% to 34,857.00 while USD/CAD ticked up 0.04% to 1.42.

WTI crude dropped 1.94% to 67.25 and natural gas fell 1.65% to 3.17. The Canada 2-year yield declined 0.50% to 2.24% as short-end bonds attracted modest buying on the hawkish tone. Gold advanced 0.24% to 4,078.00 amid safe-haven flows.

The Day Ahead

Markets focus on the 05:30 ET release of the S&P Global Manufacturing PMI, the sole scheduled Canadian data point. The print will test whether factory conditions deteriorated further after recent soft readings. No Bank of Canada speakers or policy announcements are listed.

Traders will also monitor USD/CAD reaction to any PMI surprise that alters near-term easing odds. Broader attention turns to U.S. data that could influence cross-border capital flows.

Other Economic Notes

Energy infrastructure developments, including Enbridge pipeline expansions, continue to support medium-term export capacity. Ottawa’s new critical-minerals talks with the United States aim to reduce reliance on Chinese supply chains and may provide modest CAD support over time. CUSMA renewal uncertainty lingers with existing U.S.

tariffs still in place.

Global Macro News

The Federal Reserve’s latest projections signal fewer cuts than previously expected, keeping external pressure on the Canadian dollar. India’s central bank governor floated the possibility of a lower long-run inflation target, echoing similar debates at the BoC. South African rand strength on softer oil prices highlights commodity currency linkages that also affect CAD.

Eurozone data left EUR/CAD little changed at 1.62. <i>↓ p.2</i>