Canada Macro Daily(Beta Mode)

Canada PMI Holds at 53, TSX Edges Higher

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| S&P/TSX | 34,966.70 | +0.31% |

| USD/CAD | 1.42 | -0.11% |

| EUR/CAD | 1.63 | +0.51% |

| WTI Crude | 68.40 | -0.42% |

| Natural Gas | 3.24 | +1.41% |

| Gold | 4,193.00 | +1.95% |

| Brent Crude | 71.68 | -0.17% |

| Bitcoin | 62,015.81 | +0.86% |

| Canada 2Y Govt Yield | 2.24% | -0.50% |

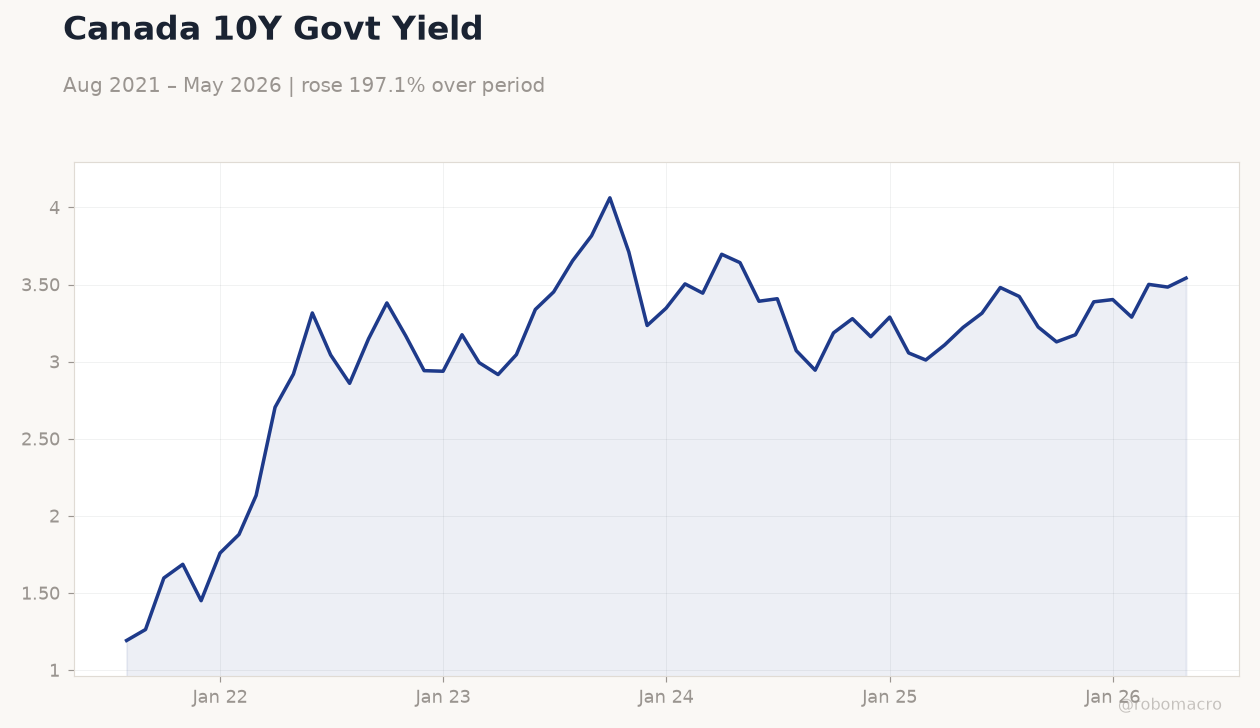

| Canada 10Y Govt Yield | 3.54% | +1.67% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| BoC Gov Macklem Speech | - | - | - |

| S&P Global Manufacturing PMI Index | 52.90 | - | 53 |

Canada 10Y Govt Yield | Type: macro_line | Percent: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.192,3.381,3.234,3.056,3.483,3.542

Canada 10Y Govt Yield | Type: macro_line | Percent: 3.542 (2026-05-01) | Range: 1.192–4.062 | Trend(6pt): 1.192,3.381,3.234,3.056,3.483,3.542

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- S&P Global Manufacturing PMI edged up to 53.0, extending expansion and reinforcing BoC caution on policy easing.

- S&P/TSX rose 0.31% to 34,966.70 while Canada 2-year yield fell 0.50% to 2.24%, narrowing the policy spread.

- USD/CAD declined 0.11% to 1.42 as WTI Crude slipped 0.42% to $68.40 amid mixed energy flows.

Yesterday's Recap

S&P Global Manufacturing PMI printed 53.0 versus 52.9 prior, confirming steady factory expansion and aligning with the Bank of Canada’s measured tone. Governor Macklem delivered remarks that markets interpreted as data-dependent without shifting near-term rate expectations. The S&P/TSX advanced 0.31% to 34,966.70, supported by energy and materials sectors.

Canada 2-year yield dropped 0.50% to 2.24% while the 10-year yield rose 1.67% to 3.54%, steepening the curve. USD/CAD fell 0.11% to 1.42 as CAD outperformed on relative yield stability. Natural Gas rose 1.41% to $3.24 while Gold jumped 1.95% to $4,193.00, reflecting safe-haven demand.

Broader equity and FX moves stayed contained ahead of the weekend.

The Day Ahead

No scheduled Canadian data releases appear on 3 July, leaving markets to digest yesterday’s PMI and Macklem comments. Focus shifts to external drivers including US employment figures that could influence CAD crosses. Energy traders will monitor WTI and Brent for any follow-through after modest declines.

Government of Canada bonds may see light positioning as participants await next week’s inflation update. The absence of domestic events keeps attention on BoC forward guidance already priced into the 2-year sector.

Other Economic Notes

Alberta’s oil and gas surge drove the strongest monthly GDP gain since last summer, easing recession concerns. Ottawa’s push for new Pacific crude pipelines signals continued emphasis on energy export capacity. Canada-Philippines trade and defence agreements expand non-US market access for Canadian firms.

CUSMA renewal uncertainty and lingering US tariffs remain the dominant external risk for Canadian manufacturers. Home-price growth slowed to 0.3% m/m in June, the weakest pace in four months.

Global Macro News

US data showed weak jobs alongside sticky inflation, raising the prospect of a policy dilemma for the Federal Reserve. <i>↓ p.2</i>