The Day Ahead

Today's calendar remains light with no scheduled economic releases or events, allowing markets to digest recent global developments and position for the week ahead. Investors may focus on any spillover from Asian peers, particularly in thin volumes, with potential volatility from currency pairs if US data influences the dollar.

Attention could shift to sector-specific moves, such as renewables and mobility, following reports of strong growth projections in carbon fiber demand, which may support related equities in China.

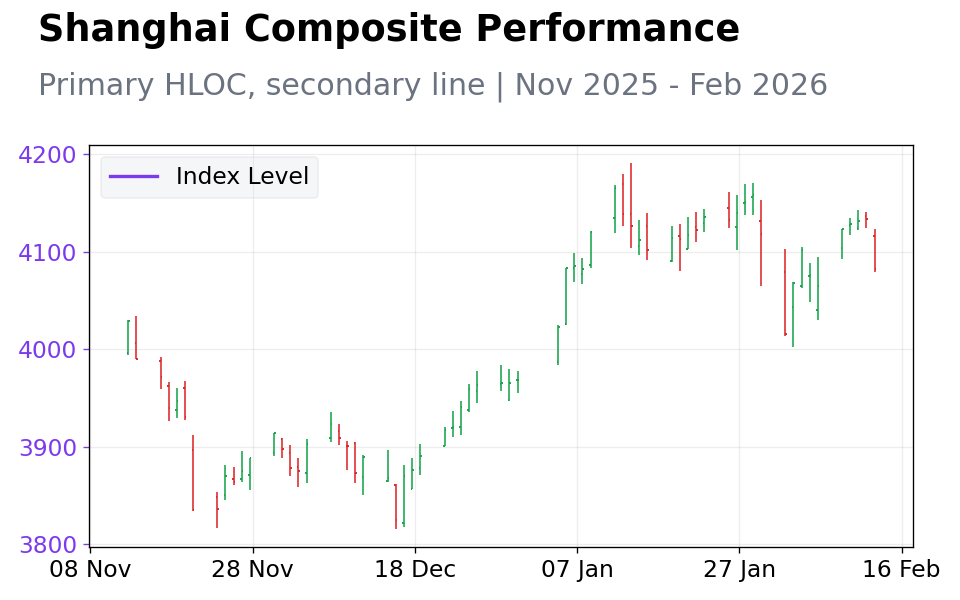

Overall, without major catalysts, trading is expected to be range-bound, with yields on Chinese government bonds holding steady—the 2Y at 2.90% unchanged—providing a stable backdrop for fixed income.

Other Economic Notes

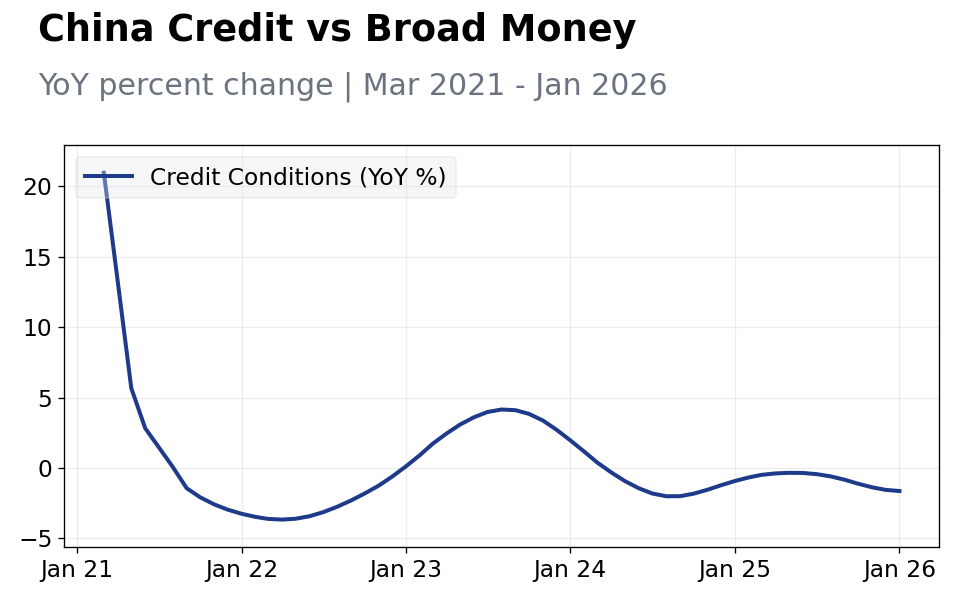

Credit conditions in China continue to show resilience, with steady liquidity supporting corporate borrowing despite global rate uncertainties. Recent PBOC operations have maintained ample funding, aiding credit expansion in key sectors like manufacturing and infrastructure, though analysts watch for any tightening signals amid inflation watch.

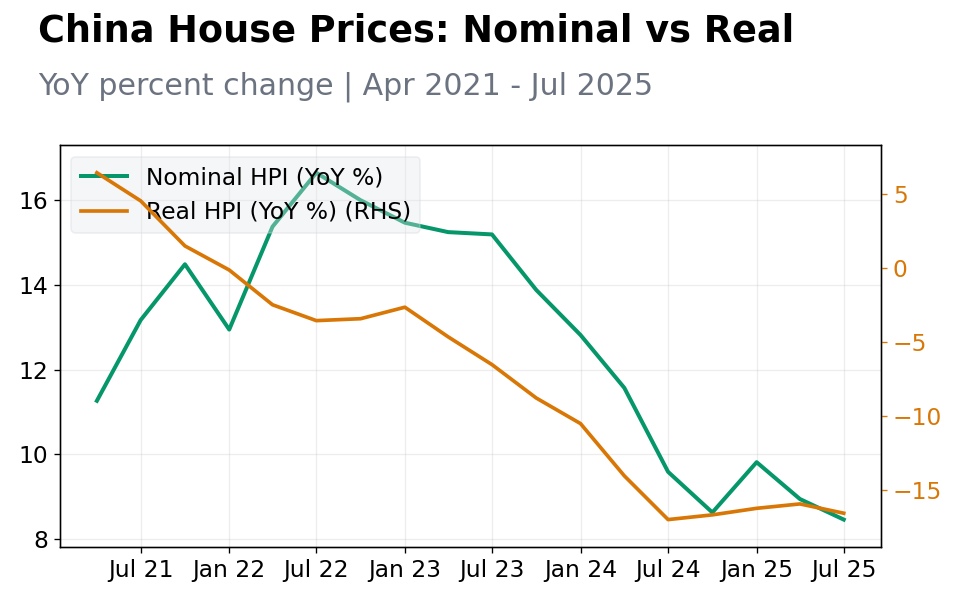

Property markets remain under pressure, with ongoing regulatory oversight curbing speculative activity; however, targeted stimulus in urban renewal could stabilize developer sentiment. Trade dynamics are mixed, with exports benefiting from Asia-Pacific demand in renewables, but imports face headwinds from commodity price volatility.

Commodities outlook is cautious, as softening copper and iron ore prices reflect global supply gluts and slower construction activity, while oil's modest gains from geopolitical risks could indirectly boost China's energy import costs if tensions escalate.

Global Macro News

Asian stocks edged higher in thin holiday trading, influenced by rising crude oil prices amid heightened geopolitical risks from Iran's naval exercises near key shipping corridors ahead of US talks. This could indirectly pressure China's import bills and energy sectors, though modest gains in regional indices provide a supportive backdrop for Hong Kong-listed Chinese firms.

Broader global themes, including surging demand for memory chips driven by AI applications and strong growth in carbon fiber markets (projected 18% CAGR through 2031, led by Asia-Pacific), highlight opportunities for China's tech and renewable sectors, potentially offsetting commodity weaknesses.

PBoC Watch

The People's Bank of China (PBOC) maintained a neutral stance in recent communications, with no adjustments to key rates in the latest liquidity operations. (cont...)