The Day Ahead

With no major economic data releases scheduled for February 18, market attention will likely center on intraday sentiment and any ad-hoc policy announcements from Beijing. Traders may monitor offshore flows into A-shares, particularly in light of recent foreign investment trends, as global risk appetite influences liquidity.

Expectations for commodity volatility could rise, given ongoing global supply chain dynamics, with iron ore and copper futures potentially reacting to any updates on infrastructure spending. Currency desks will watch PBOC's daily fixing for signals on yuan management amid stable external conditions.

Overall, a quiet calendar suggests range-bound trading, but any headlines on U.S.-China trade relations could introduce swings, especially in export-sensitive sectors like manufacturing and tech.

Other Economic Notes

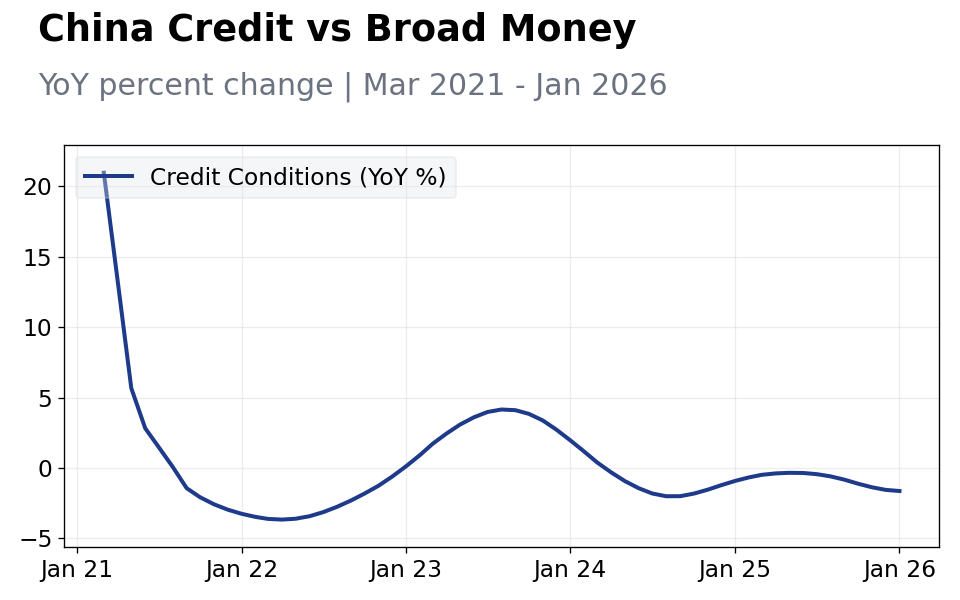

Credit conditions in China remain accommodative, with recent data indicating steady loan growth despite tighter regulatory scrutiny on shadow banking. Banks are channeling funds toward high-tech and green industries, aligning with national priorities, though overall credit expansion has moderated to curb leverage risks in the corporate sector.

This balanced approach supports economic recovery without fueling inflation, but investors should watch for any shifts in reserve requirements that could impact liquidity.

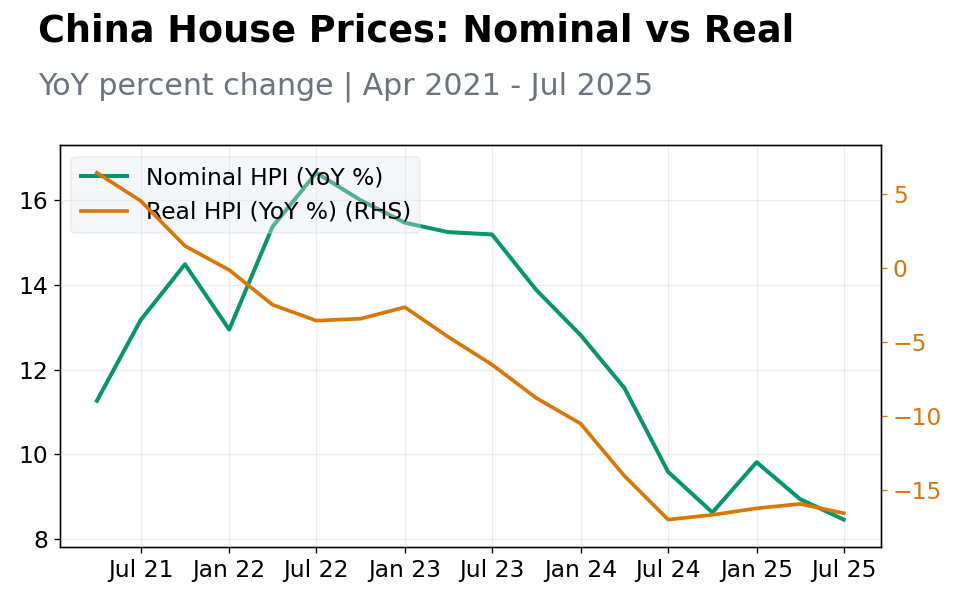

The property market continues to stabilize, aided by targeted easing measures such as lower mortgage rates and developer support. Home sales have shown modest upticks in tier-1 cities, but inventory overhang persists in smaller markets, pressuring prices.

Trade dynamics are mixed, with exports resilient to global slowdowns, particularly in EVs and renewables, while imports of commodities like iron ore reflect ongoing infrastructure needs. Commodity prices, including rising copper driven by AI and electrification demand, underscore China's role as a key consumer, potentially boosting related equities if global trends persist.

Global Macro News

Global macro developments are increasingly intertwined with China's economy, particularly through commodity channels. BHP's strategic pivot toward copper, highlighted in recent earnings, aligns with surging demand from AI infrastructure and electrification, which could benefit Chinese importers and processors.

This shift, amid record share prices for miners, signals positive upstream pressures for China's manufacturing sector, though it may elevate input costs if supply tightens.

Additionally, broader themes like IT sector resilience, as noted in analyses of oversold tech stocks and AI investments, point to opportunities for Sino-U.S. collaboration or competition.

Political noise, such as U.S. critiques of alternative climate diplomacy, adds uncertainty to trade relations, potentially affecting China's export outlook and global commodity flows.

PBoC Watch

The People's Bank of China (PBOC) maintained a neutral stance in its latest liquidity operations, injecting moderate funds via reverse repos to ensure stable interbank rates amid the Lunar New Year aftermath. Recent communications emphasize targeted support for the real economy, with no immediate signals of broad rate cuts, focusing instead on MLF rollovers at unchanged rates to anchor expectations.

This approach suggests a preference for precision tools over aggressive easing, aiming to balance growth with financial stability.

LPR guidance remains steady, with the 1-year rate at 3.45% and 5-year at 3.95% in the prior adjustment, reflecting caution on property lending. Markets interpret this as a signal of confidence in domestic recovery, reducing bets on near-term cuts, though OMO activities indicate readiness to counter any liquidity squeezes.

For markets, this implies continued yield stability, with potential upside for bonds if external risks escalate.

Looking ahead, PBOC statements hint at monitoring global factors like U.S. Fed moves, which could influence CNY policy.

Investors should note any forthcoming MLF decisions, as they may provide clues on 2026 easing trajectory, supporting equities in consumption-driven sectors while capping speculative flows.