The Day Ahead

February 19 brings a quiet calendar for China-specific releases, with no scheduled economic data or policy announcements. Markets will monitor any unscheduled PBOC liquidity operations amid ongoing yuan stability efforts.

Attention turns to potential spillover from global events, including U.S. inflation readings that could influence Fed policy signals.

Investors eye commodity futures for cues on industrial demand, given recent iron ore stability at 99.74. Broader Asian market openings may set the tone, especially after Japan's export surge.

No major corporate earnings are due, shifting focus to geopolitical updates. Expect low volatility unless external shocks emerge.

Other Economic Notes

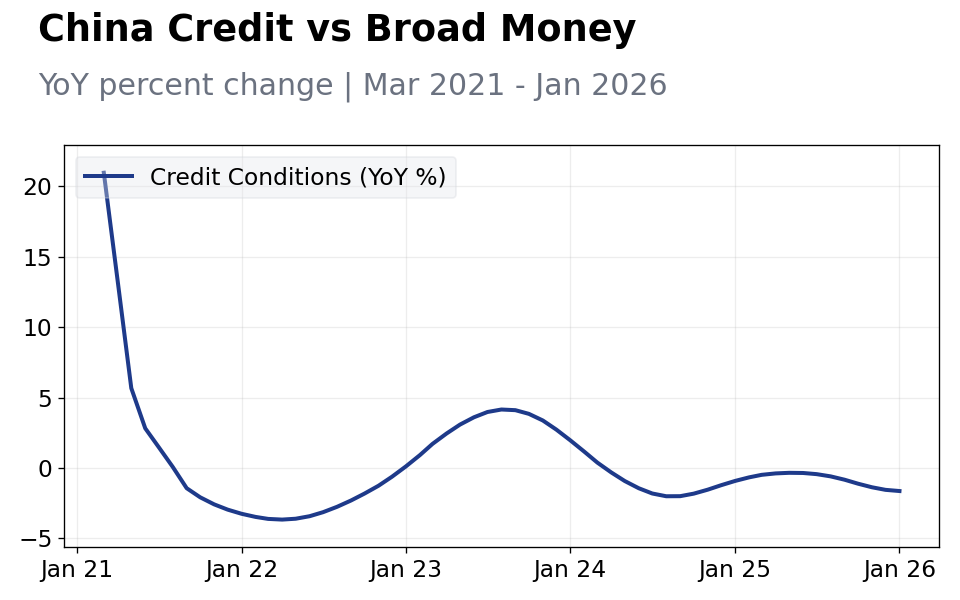

Credit growth remains subdued, with banks tightening lending amid property sector woes, potentially capping investment recovery. Property market stabilization efforts continue, but sales data suggest ongoing weakness, pressuring developers' funding costs.

Trade dynamics improved with Japan's 17% export surge to China in January, boosting bilateral flows and supporting commodity demand like iron ore. Commodities face headwinds, with copper prices slipping on global supply glut concerns despite steady iron ore levels.

These factors highlight a cautious economic outlook, with external trade providing some uplift against domestic challenges in lending and real estate.

Global Macro News

Global markets are navigating mixed signals that could impact China's export-driven economy, particularly with Japan's exports jumping 17% in January, largely due to strong shipments to China and other Asian markets, highlighting resilient regional demand amid broader slowdowns. This surge underscores China's role as a key importer, potentially bolstering its trade surplus but exposing it to yen fluctuations.

Meanwhile, the international express delivery market is projected to reach USD 76.42 billion by 2033, driven by e-commerce growth, which benefits Chinese logistics firms amid expanding cross-border trade. In Southeast Asia, Indonesia's alignment with U.S.

policies under Trump's "Board of Peace" could reshape regional alliances, indirectly affecting China's Belt and Road initiatives and investment flows. French heritage brand Weill is targeting global growth with expansions in the U.S., Asia, and Middle East, emphasizing fair pricing and artisanal craftsmanship, which may signal broader consumer trends in premium goods relevant to China's luxury import market.

Commodity markets remain volatile, with Brent crude edging up amid Middle East calm, supporting China's energy imports but pressuring inflation controls. U.S.

(cont...)

Global Macro News (continued)

inventory builds are capping oil gains, potentially easing China's import bills. Overall, these trends suggest a supportive external environment for China's recovery, though geopolitical risks persist.

PBoC Watch

The People's Bank of China maintained steady liquidity operations last week, injecting net funds via reverse repos to ensure ample banking system reserves amid holiday effects. Recent communications emphasize prudent monetary policy, with no hints of imminent rate cuts despite flat 2-year government yields at 2.90%.

MLF rates held unchanged in the latest rollover, signaling caution on easing to avoid yuan depreciation pressures. LPR guidance remains anchored, with markets pricing in stability after USD/CNY's minor dip to 6.90.

PBOC statements stress supporting real economy growth without fueling asset bubbles, interpreting weak equity moves as transient. This approach implies limited intervention unless trade data weakens further, fostering a neutral outlook for bond markets.

Analysts see room for targeted stimulus if property drags persist, based on prior deputy governor remarks on flexible tools. Overall, policy signals point to measured support, bolstering yuan resilience against global volatility.