China Macro Daily(Beta Mode)

China Stocks Dip, Yuan Edges Up

Market Snapshot

| Asset | Level | Change |

|---|---|---|

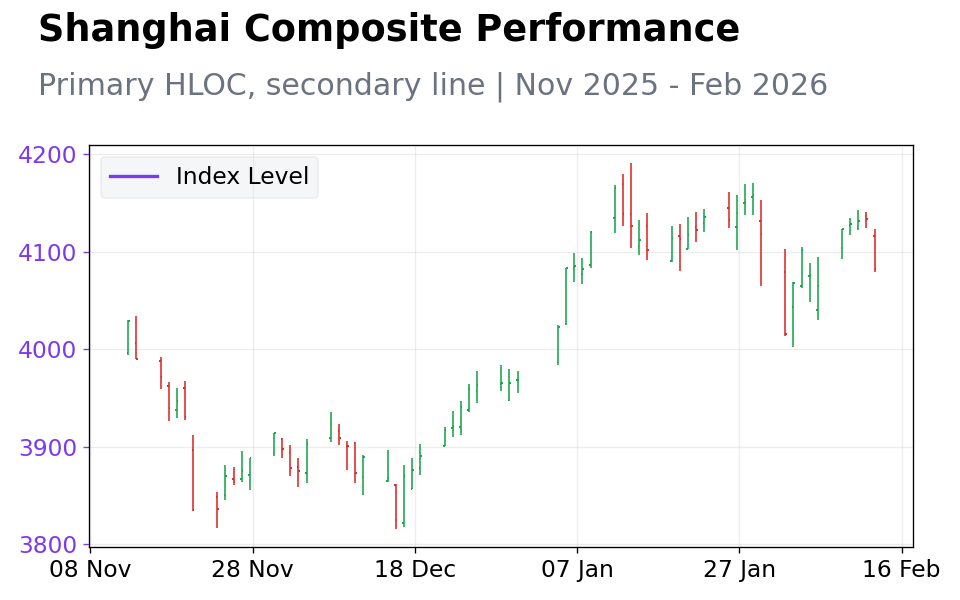

| Shanghai Composite | 4,082.07 | -1.26% |

| CSI 300 | 4,660.41 | -1.25% |

| Hang Seng | 26,413.35 | -1.10% |

| USD/CNY | 6.90 | -0.07% |

| EUR/CNY | 8.12 | -0.25% |

| Gold | 5,063.70 | +1.76% |

| Brent Crude | 70.95 | -0.99% |

| Bitcoin | 66,801.70 | -0.23% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Chinese equities fell over 1% amid regulatory concerns and foreign outflows, with Shanghai Composite at 4,082.07 and CSI 300 at 4,660.41.

- Yuan firmed slightly against USD to 6.90, while gold rose 1.76% to 5,063.70 and Brent crude slipped 0.99% to 70.95.

- No bond yield data available; markets eye potential PBoC easing amid subdued economic calendar and global volatility.

Yesterday's Recap

Chinese stock markets closed lower on February 19, with the Shanghai Composite dropping 1.26% to 4,082.07, driven by weakness in tech and consumer sectors amid ongoing regulatory concerns. The CSI 300 index fell 1.25% to 4,660.41, mirroring broader mainland declines as foreign outflows persisted. Hong Kong's Hang Seng index slid 1.10% to 26,413.35, pressured by regional sentiment despite some resilience in financials.

The USD/CNY pair edged down 0.07% to 6.90, indicating modest yuan appreciation supported by stable liquidity conditions. EUR/CNY weakened 0.25% to 8.12, reflecting eurozone uncertainties. Gold prices climbed 1.76% to 5,063.70 yuan per ounce, acting as a safe haven, while Brent crude dipped 0.99% to 70.95, weighed by demand fears.

Bitcoin held steady, declining 0.23% to 66,801.70. No bond yield data was reported for China's 2-year or 10-year government bonds. No major economic data was released, keeping focus on market dynamics and policy anticipation.

The Day Ahead

February 20 brings no scheduled economic releases from China, allowing markets to digest recent global cues and monitor yuan fixing. Attention may shift to any unscheduled PBoC liquidity operations, which could influence short-term rates. Traders will watch for State Council signals on stimulus amid persistent deflation risks.

Broader Asian events remain light, but U.S. data could indirectly impact sentiment. Expect volatility in equities if foreign flows reverse.

Overall, a quiet session focused on technical levels in stocks and FX.

Other Economic Notes

China's growth outlook remains clouded by weak domestic demand and export headwinds, with recent data suggesting manufacturing challenges. Trade tensions with the U.S. continue to pressure supply chains, prompting calls for more fiscal support.

Deflationary pressures in producer prices underscore the need for targeted stimulus to boost consumption. Recent Lunar New Year holidays have contributed to subdued trading volumes, with mainland markets resuming but facing lingering effects on sentiment.