Yesterday's Recap

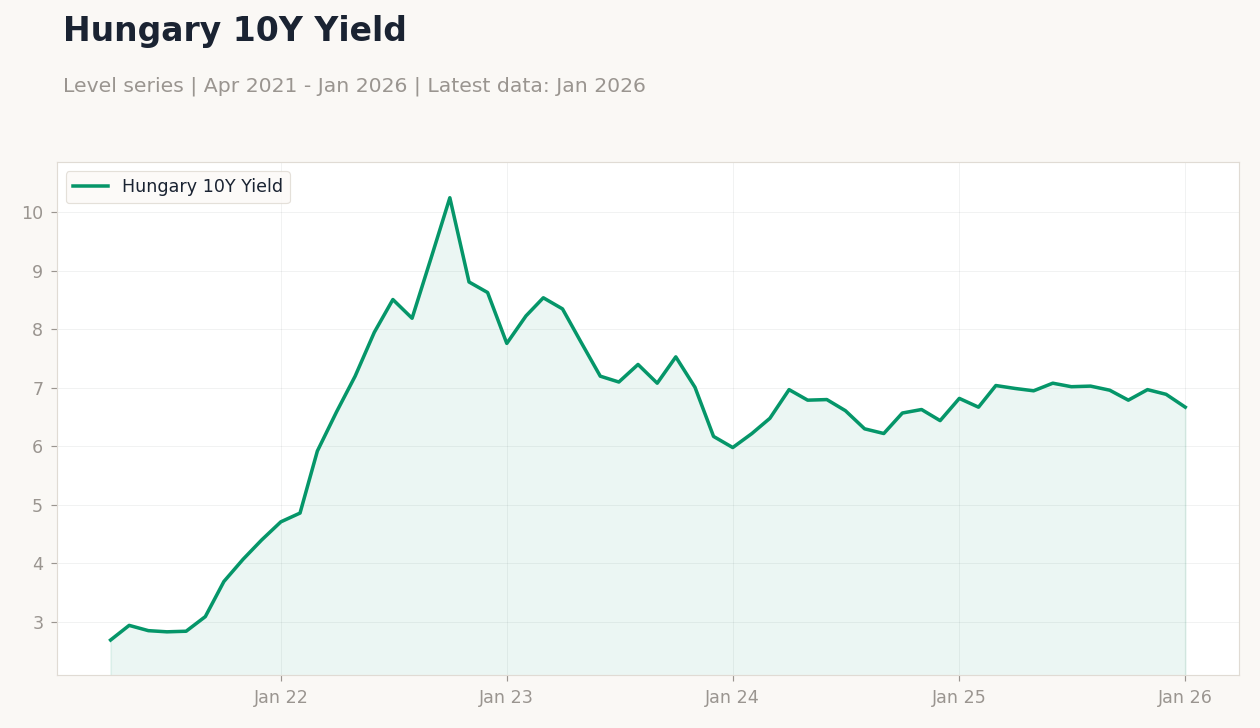

Emerging European markets displayed resilience yesterday amid global geopolitical uncertainties, with currencies appreciating against the euro as investors sought regional safe havens. In Poland, the largest CEE economy, the iShares Poland ETF rose 0.82% to 35.66, supported by a 1.03% decline in EUR/PLN to 4.25, indicating PLN strength, while the 10Y government yield dropped 2.11% to 5.10%, signaling a bond rally. Hungary saw EUR/HUF fall 1.92% to 387.15, bolstering the forint, alongside a 3.19% decrease in the 10Y yield to 6.67%, though the BUX index was not directly reported; this reflects fiscal caution amid EU fund negotiations.

The Czech Republic experienced a modest 0.27% drop in EUR/CZK to 24.35, with no major equity moves noted, underscoring its closer alignment to eurozone stability. Turkey, operating under distinct high-inflation dynamics, had its BIST 100 index decline 0.71% to 12,702.00, with USD/TRY edging down 0.03% to 44.07, as markets awaited industrial data; Romania was relatively quiet, with no standout moves in available proxies. Overall, these shifts highlight shared vulnerabilities to energy prices, as Brent crude rose 0.91% to 93.53, exacerbating import costs for gas-dependent PL, CZ, HU, and RO.

The Day Ahead

Today's calendar features Turkey's industrial production year-over-year release at 23:00 ET, with the previous figure at -2.1% and no consensus available, potentially signaling ongoing manufacturing weakness amid high inflation. Looking further, Turkey's TCMB interest rate decision is slated for March 12 at 03:00 ET, expected to hold at 37% based on consensus, though persistent price pressures could prompt surprises. Poland's inflation data arrives on March 13 at 01:00 ET, including month-over-month at a consensus of 0.6% (previous 0.6%) and year-over-year with no consensus (previous 2.2%), which may influence NBP's policy outlook.

No immediate events are noted for Czech Republic, Hungary, or Romania, allowing focus on these Turkish and Polish indicators. Markets will monitor these for insights into regional disinflation progress and euro convergence. Broader attention may turn to any ECB-related spillovers affecting CNB and MNB decisions.

Poland 10Y Yield vs NBP Context | Type: macro_line | Poland 10Y Yield: 5.1 (2026-01-01) | Range: 1.55–7.82 | Trend(6pt): 1.55,7.14,5.59,5.6,5.21,5.1 | Poland Interbank Rate: 3.93 (2026-01-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.05,6.69,5.85,4.06,3.93

Poland 10Y Yield vs NBP Context | Type: macro_line | Poland 10Y Yield: 5.1 (2026-01-01) | Range: 1.55–7.82 | Trend(6pt): 1.55,7.14,5.59,5.6,5.21,5.1 | Poland Interbank Rate: 3.93 (2026-01-01) | Range: 0.21–7.51 | Trend(6pt): 0.21,7.05,6.69,5.85,4.06,3.93