Emerging Europe Macro Daily(Beta Mode)

Polish Wages Slow Amid Geopolitics

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,047.72 | -0.51% |

| iShares Poland | 35.53 | +0.77% |

| EUR/PLN | 4.27 | -0.18% |

| EUR/HUF | 390.31 | -0.35% |

| EUR/CZK | 24.46 | -0.03% |

| USD/TRY | 44.31 | -0.03% |

| Brent Crude | 102.85 | -5.34% |

| Gold | 4,713.60 | +2.45% |

| Bitcoin | 70,839.20 | -0.57% |

| Poland 10Y Govt Yield | 4.99% | -2.16% |

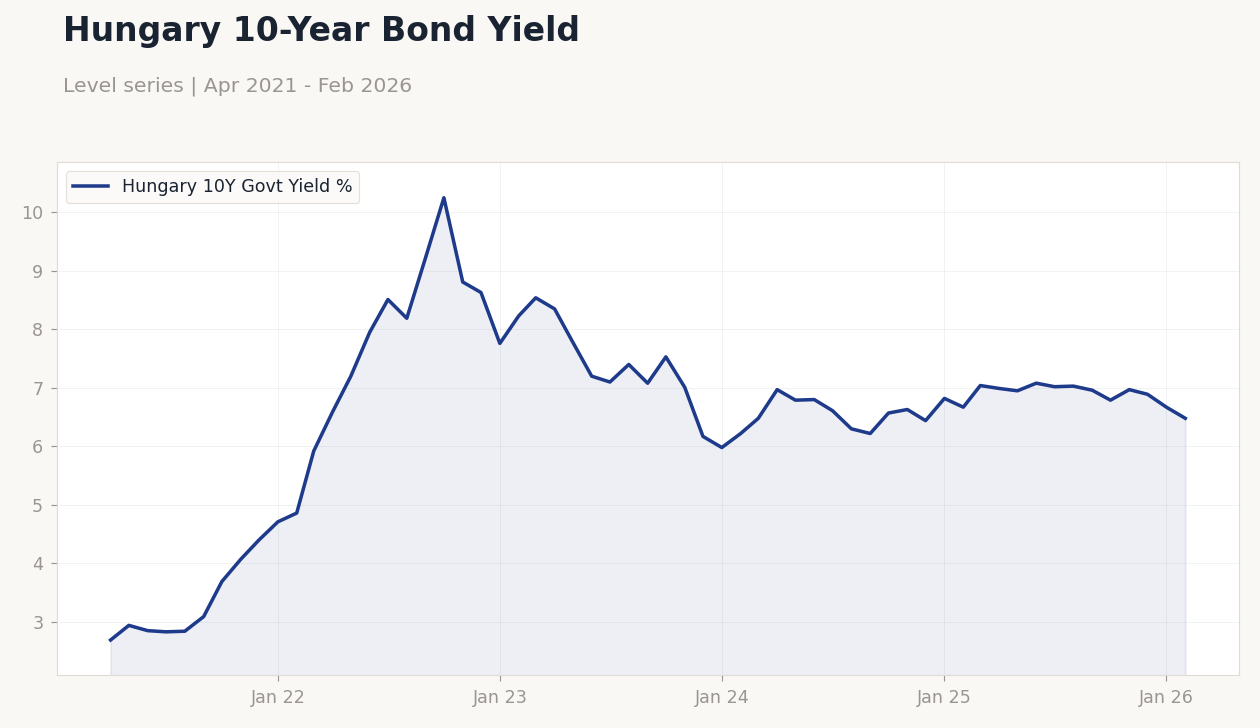

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Hungary 10-Year Bond Yield | Type: macro_line | Hungary 10Y Govt Yield %: 6.48 (2026-02-01) | Range: 2.69–10.25 | Trend(6pt): 2.69,7.95,7.4,6.57,6.89,6.48

Hungary 10-Year Bond Yield | Type: macro_line | Hungary 10Y Govt Yield %: 6.48 (2026-02-01) | Range: 2.69–10.25 | Trend(6pt): 2.69,7.95,7.4,6.57,6.89,6.48

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Poland's wage growth decelerated, but geopolitical tensions clouded the outlook for NBP rate cuts, with the zloty slightly weakening on Middle East escalation risks.

- Hungarian yields fell as markets digested EU summit clashes over Ukraine aid, where Hungary blocked a €90bn loan alongside Slovakia.

- Turkish equities dipped amid broader EM volatility, while Polish assets gained on EU fund optimism, contrasting with global war-driven inflation pressures.

Yesterday's Recap

Emerging Europe markets displayed mixed performances on March 19, with Turkey's BIST 100 index declining 0.51% to 13,047.72, reflecting ongoing inflation concerns and lira stability issues. In Poland, the iShares MSCI Poland ETF rose 0.77% to 35.53, supported by news of slowing wage growth that could ease domestic inflationary pressures, though geopolitics tempered rate cut expectations. The Polish zloty strengthened modestly against the euro, with EUR/PLN falling 0.18% to 4.27, despite brief weakening from Middle East tensions.

Hungarian assets saw bond yields drop, with the 10Y government yield decreasing 2.85% to 6.48%, amid reports of Hungary blocking EU aid to Ukraine, which highlighted fiscal and political divergences. Czech and Romanian markets remained subdued, with EUR/CZK nearly flat at 24.46 (down 0.03%) and limited data releases, while broader regional sentiment was influenced by falling Brent crude prices (down 5.34% to 102.85). Turkey's USD/TRY held steady at 44.31 (down 0.03%), underscoring the CBRT's challenges in a high-inflation environment distinct from CEE peers.

The Day Ahead

The calendar remains light on March 20 with no major data releases scheduled across Emerging Europe, allowing markets to digest recent geopolitical developments. Investors will monitor any follow-up from the EU summit on Ukraine aid, particularly Hungary's stance, which could impact regional FX and bond dynamics. In Turkey, attention turns to potential CBRT commentary on inflation amid global energy volatility.

Broader focus includes ECB signals, as CNB and MNB policies often align closely with euro-area moves. Expect quiet trading unless Middle East tensions escalate further, affecting risk appetite in Poland and Hungary.

Other Economic Notes

Broader economic themes in Emerging Europe highlight energy dependency vulnerabilities, exacerbated by the Iran war's impact on oil prices and supply chains, particularly for net importers like Poland and the Czech Republic. Convergence criteria for euro adoption remain in focus for Romania and Hungary, though political hurdles such as Hungary's EU disputes delay progress. Turkey's distinct macro dynamics, with structurally high inflation, contrast with CEE's disinflation trends, potentially widening policy divergences.