Emerging Europe Macro Daily(Beta Mode)

Turkish Sentiment Dips, Polish Jobless Steady

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 12,727.10 | -1.83% |

| iShares Poland | 34.95 | -1.52% |

| EUR/PLN | 4.27 | +0.00% |

| EUR/HUF | 388.04 | +0.30% |

| EUR/CZK | 24.51 | +0.30% |

| USD/TRY | 44.45 | +0.20% |

| Brent Crude | 101.30 | -6.21% |

| Gold | 4,438.10 | +1.43% |

| Bitcoin | 68,669.95 | -3.70% |

| Poland 10Y Govt Yield | 4.99% | -2.16% |

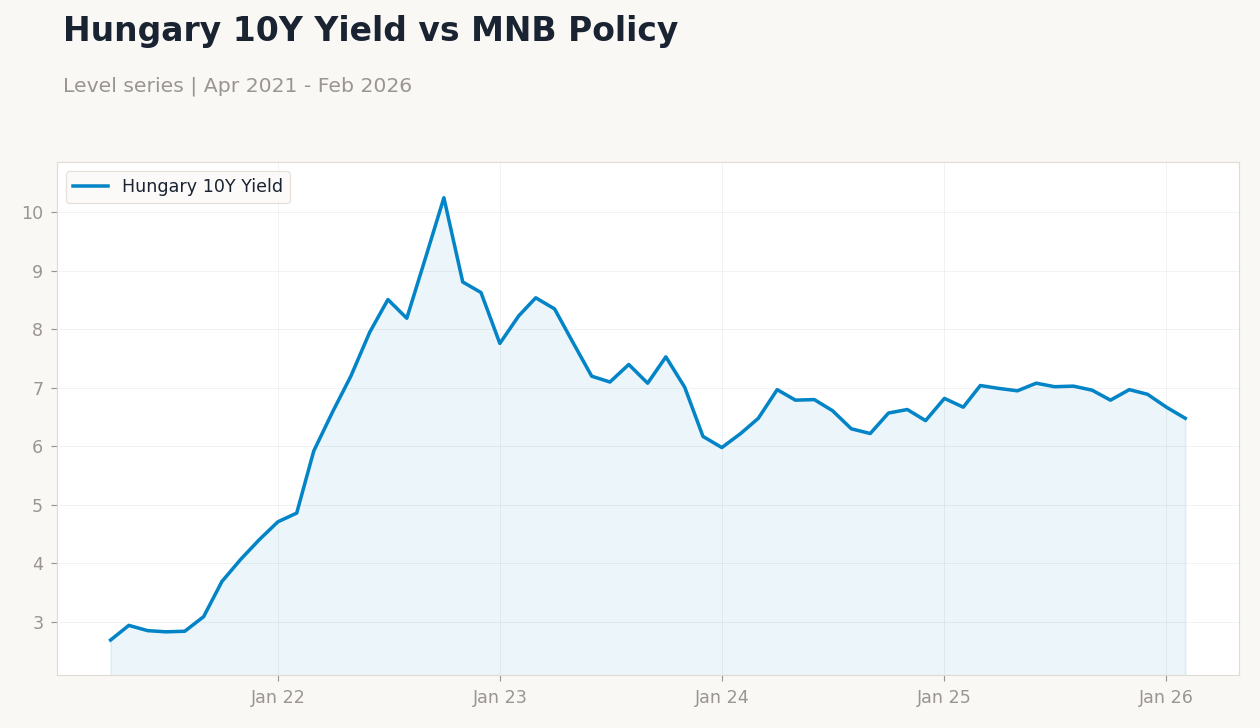

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | 85.70 | - | 85 |

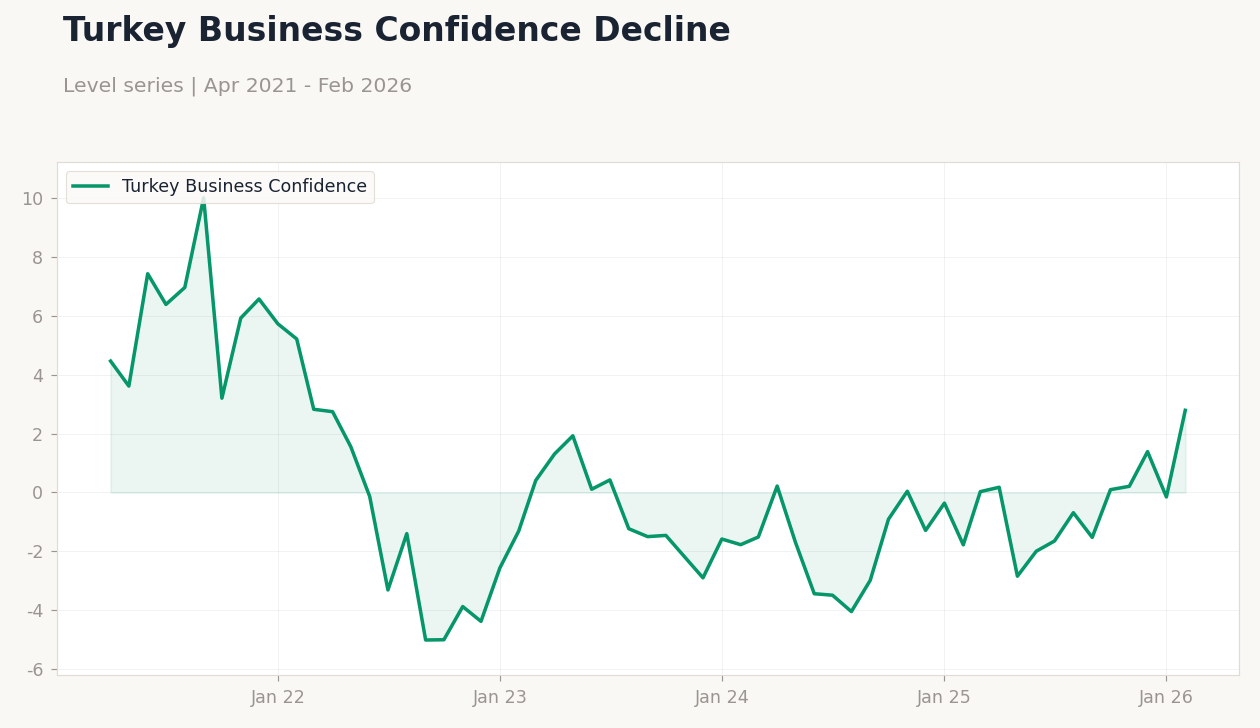

| Business Confidence Index | 104.10 | - | 101 |

| Headline Unemployment Rate | 6 | 6.10 | 6.10 |

Turkey Consumer Confidence Trend | Type: macro_line | Turkey Consumer Confidence: 85.7 (2026-02-01) | Range: 63.4–91.1 | Trend(6pt): 80.2,63.4,68,80.6,83.5,85.7

Turkey Consumer Confidence Trend | Type: macro_line | Turkey Consumer Confidence: 85.7 (2026-02-01) | Range: 63.4–91.1 | Trend(6pt): 80.2,63.4,68,80.6,83.5,85.7

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Turkish consumer and business confidence indices declined, signaling weakening sentiment amid persistent inflation pressures.

- Poland's headline unemployment rate aligned with consensus at 6.1%, reflecting stable labor market conditions in the largest CEE economy.

- Regional equities and currencies faced headwinds, with Turkish stocks down sharply and CEE bond yields easing on global risk-off mood.

Yesterday's Recap

Emerging Europe markets experienced mixed but mostly negative movements, with Turkey's BIST 100 index dropping 1.83% to 12,727.10 amid falling confidence indicators. In Turkey, the Consumer Confidence Index fell to 85 from a previous 85.7, while the Business Confidence Index declined to 101.00 from 104.1, highlighting ongoing economic challenges in the region's largest economy. Poland's headline unemployment rate met consensus expectations at 6.1%, up slightly from the previous 6%, underscoring resilient labor dynamics despite broader slowdown signals.

The iShares Poland ETF slid 1.52% to 34.95, reflecting investor caution, while the EUR/PLN held steady at 4.27 with no change. Hungarian and Czech currencies weakened modestly, with EUR/HUF up 0.30% to 388.04 and EUR/CZK also up 0.30% to 24.51, pressured by global risk aversion. Polish and Hungarian 10-year government yields fell, with Poland's to 4.99% (-2.16%) and Hungary's to 6.48% (-2.85%), as safe-haven flows supported bonds.

No major data emerged from the Czech Republic, Hungary, or Romania, keeping focus on Turkey's sentiment dip and Poland's steady jobs figures.

The Day Ahead

The Emerging Europe calendar remains light today with no scheduled economic releases across Poland, the Czech Republic, Hungary, Romania, or Turkey. Investors will monitor any unscheduled developments, such as potential FX interventions by the CBRT given recent USD/TRY volatility at 44.45 (+0.20%). Attention may shift to broader EU events, including any updates on energy supply amid Middle East tensions, which could impact import-dependent CEE economies.

Tomorrow also features an empty slate, potentially allowing markets to digest global cues like U.S. recession signals. Traders should watch for spillover from commodity moves, with Brent crude down 6.21% to 101.30, affecting Turkey's external balances.

Overall, the quiet period underscores the region's sensitivity to external shocks over domestic data.

Other Economic Notes

Broader themes in Emerging Europe highlight persistent energy vulnerabilities, particularly for EU members Poland, Czech Republic, Hungary, and Romania, which face risks from Middle East conflicts disrupting oil supplies. (cont...)