Emerging Europe Macro Daily(Beta Mode)

CEE Markets Mixed, Yields Ease

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 12,698.20 | -0.23% |

| iShares Poland | 34.58 | -1.06% |

| EUR/PLN | 4.28 | +0.16% |

| EUR/HUF | 389.40 | +0.67% |

| EUR/CZK | 24.51 | +0.10% |

| USD/TRY | 44.45 | -0.01% |

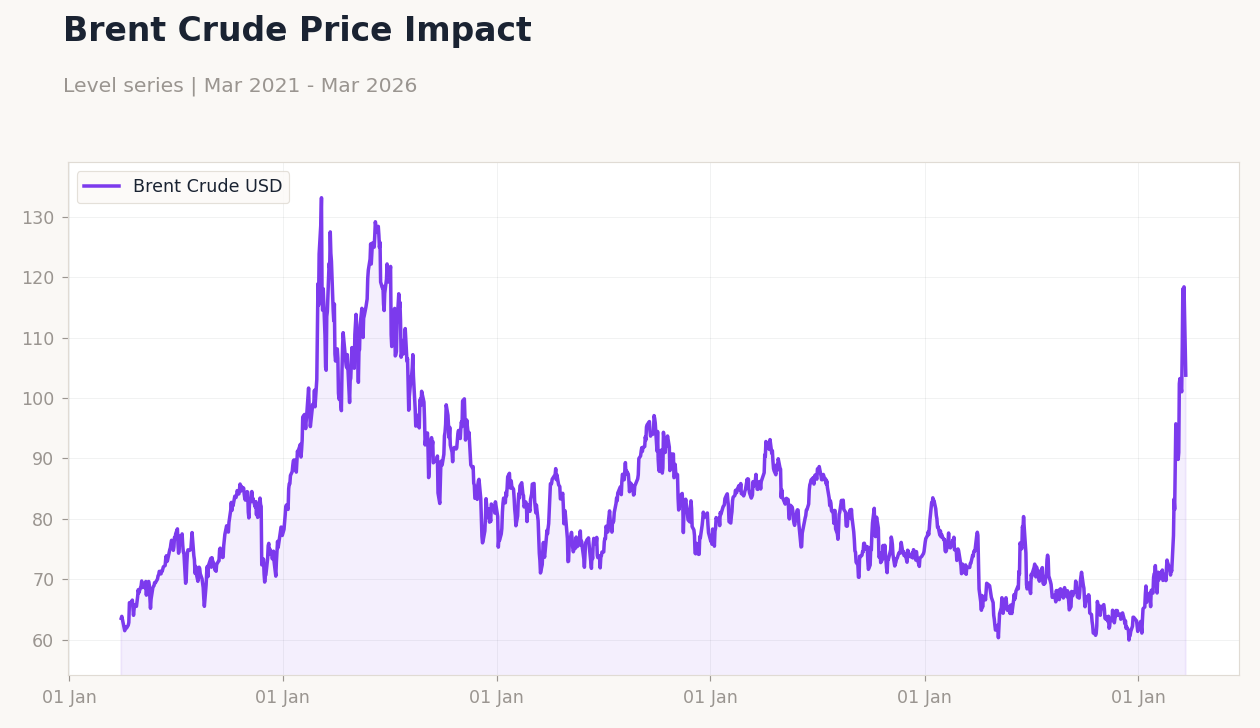

| Brent Crude | 108.05 | -4.02% |

| Gold | 4,529.10 | +0.83% |

| Bitcoin | 67,640.24 | +1.99% |

| Poland 10Y Govt Yield | 4.99% | -2.16% |

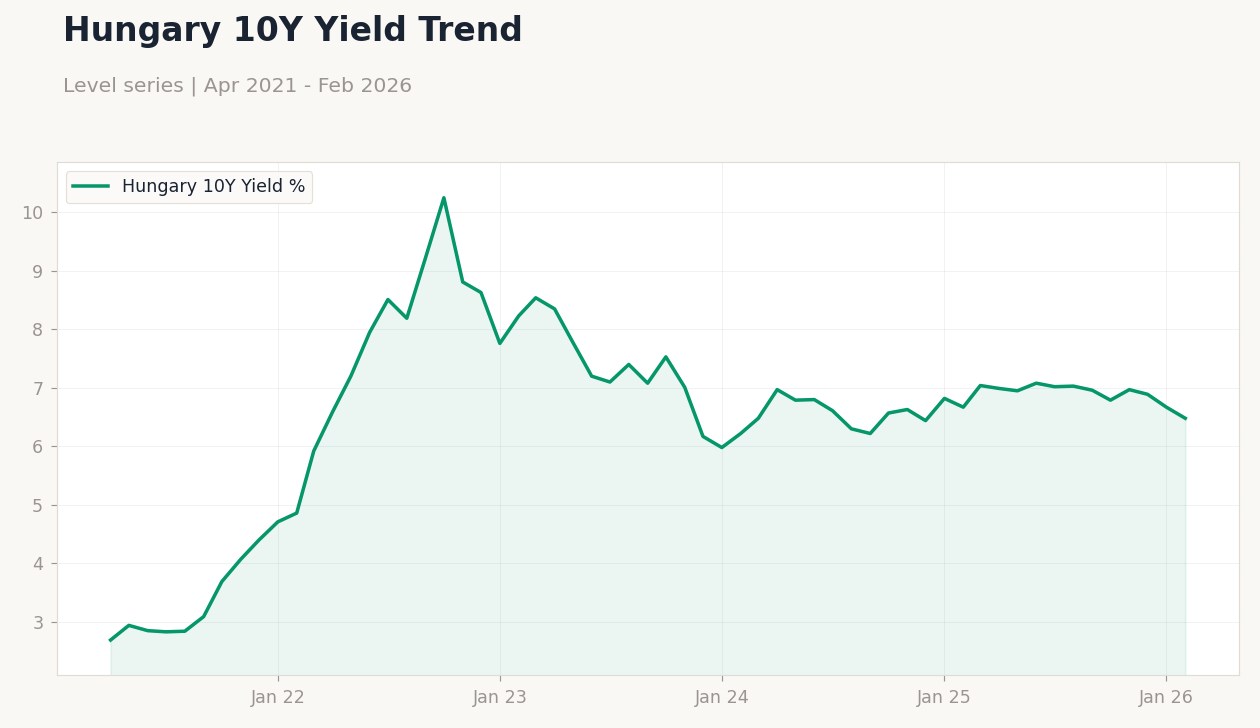

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

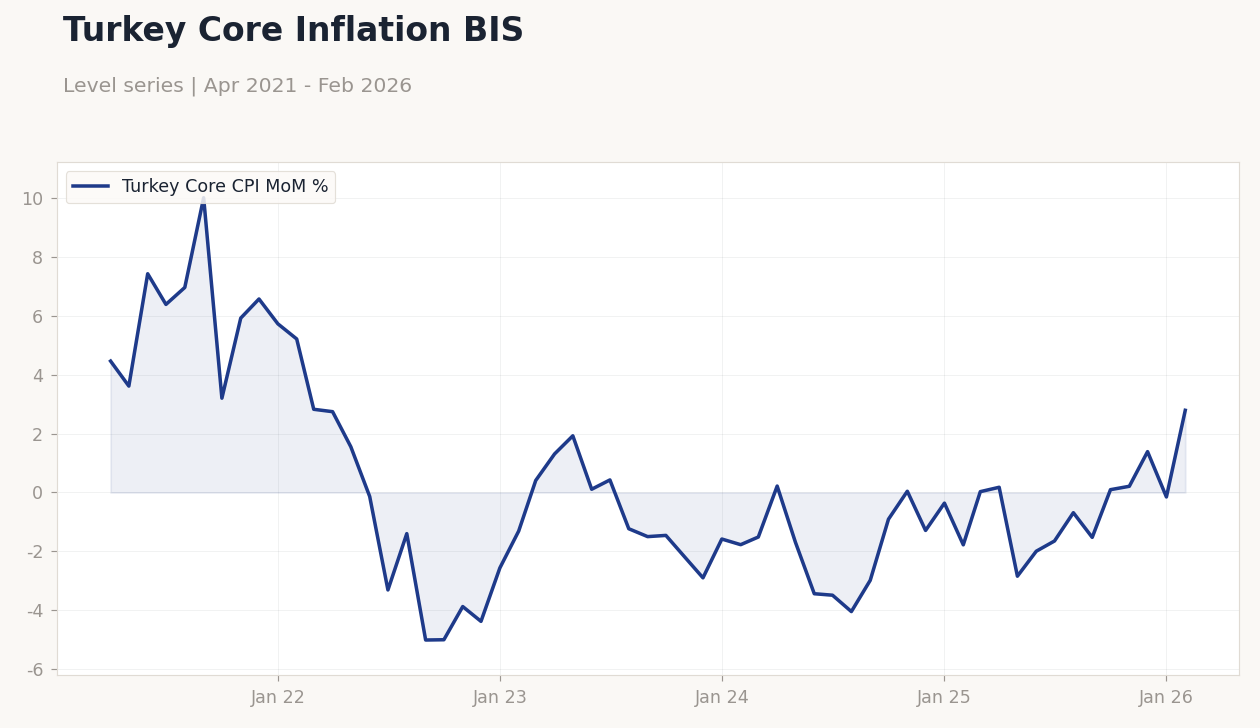

Turkey Core Inflation BIS | Type: macro_line | Turkey Core CPI MoM %: 2.796 (2026-02-01) | Range: -5.017–10.03 | Trend(6pt): 4.47,-0.1346,-1.232,-0.9081,1.39,2.796

Turkey Core Inflation BIS | Type: macro_line | Turkey Core CPI MoM %: 2.796 (2026-02-01) | Range: -5.017–10.03 | Trend(6pt): 4.47,-0.1346,-1.232,-0.9081,1.39,2.796

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Balance of Trade Final | -8,400m | - | 03:00 |

| Headline Unemployment Rate | 8.10 | - | 03:00 |

| Inflation Rate Year-over-Year Preliminary | 2.10 | - | 03:30 |

| Inflation Rate Month-over-Month | 2.96 | - | 03:00 |

| Inflation Rate Year-over-Year | 31.53 | - | 03:00 |

- Emerging Europe equities displayed mixed results, with Turkish and Polish indices declining amid global risk-off sentiment, while bond yields in Poland and Hungary decreased on safe-haven demand.

- Yesterday featured no significant economic data releases, shifting focus to upcoming Turkish trade balance, unemployment, and Polish preliminary inflation data.

- Regional central banks adopt cautious approaches, with Turkey grappling with persistent inflation pressures contrasting CEE's euro-convergence strategies.

Yesterday's Recap

Emerging Europe markets showed varied performance on March 29, as Turkey's BIST 100 index ended at 12,698.20 with a 0.23% drop, influenced by lira steadiness and commodity fluctuations. Poland's iShares Poland ETF declined 1.06% to 34.58, mirroring equity softness in the key CEE market, while EUR/PLN rose 0.16% to 4.28, exerting slight pressure on the zloty. Hungary's EUR/HUF climbed 0.67% to 389.40, indicating forint weakening, and its 10Y government yield fell 2.85% to 6.48%, pointing to bond gains amid fiscal hopes.

The Czech EUR/CZK edged up 0.10% to 24.51, with the region experiencing safe-haven inflows into bonds as Brent crude tumbled 4.02% to 108.05. Turkey's USD/TRY dipped 0.01% to 44.45, highlighting the CBRT's firm policy stance despite energy exposure. No notable macro indicators came from Romania, but EU reports on rule-of-law erosion in Hungary, Bulgaria, Croatia, Italy, and Slovakia heightened investor caution.

In summary, the absence of data emphasized FX and yield trends, with Poland's 10Y yield declining 2.16% to 4.99%.

The Day Ahead

Attention turns to Turkey's final balance of trade at 03:00 ET on March 31, following a previous -8.4 billion, which may reflect export dynamics amid lira strains. Concurrently, Turkey's headline unemployment rate, last at 8.1%, will provide labor market updates under elevated inflation. Poland's preliminary year-over-year inflation follows at 03:30 ET, with the prior at 2.1%, possibly affecting NBP decisions tied to euro goals.

Looking further, Turkey's month-over-month and year-over-year inflation on April 3, previously 2.96% and 31.53%, could challenge CBRT actions. No direct events for the Czech Republic, Hungary, or Romania, though EU youth mobility proposals may influence regional labor indirectly. Traders will watch these for contrasts between Turkey's turbulence and CEE steadiness.

Other Economic Notes

Key trends in Emerging Europe underscore energy import reliance, with Poland and the Czech Republic progressing in diversification from Russian supplies post-Ukraine invasion to curb vulnerabilities. (cont...)