Emerging Europe Macro Daily(Beta Mode)

Turkey Data Awaited, Poland Cuts Doubted

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 12,626.40 | -0.57% |

| iShares Poland | 34.64 | +0.17% |

| EUR/PLN | 4.29 | +0.16% |

| EUR/HUF | 386.43 | -0.25% |

| EUR/CZK | 24.54 | +0.17% |

| USD/TRY | 44.47 | +0.05% |

| Brent Crude | 107.37 | -4.80% |

| Gold | 4,596.20 | +1.55% |

| Bitcoin | 67,438.11 | +2.25% |

| Poland 10Y Govt Yield | 4.99% | -2.16% |

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

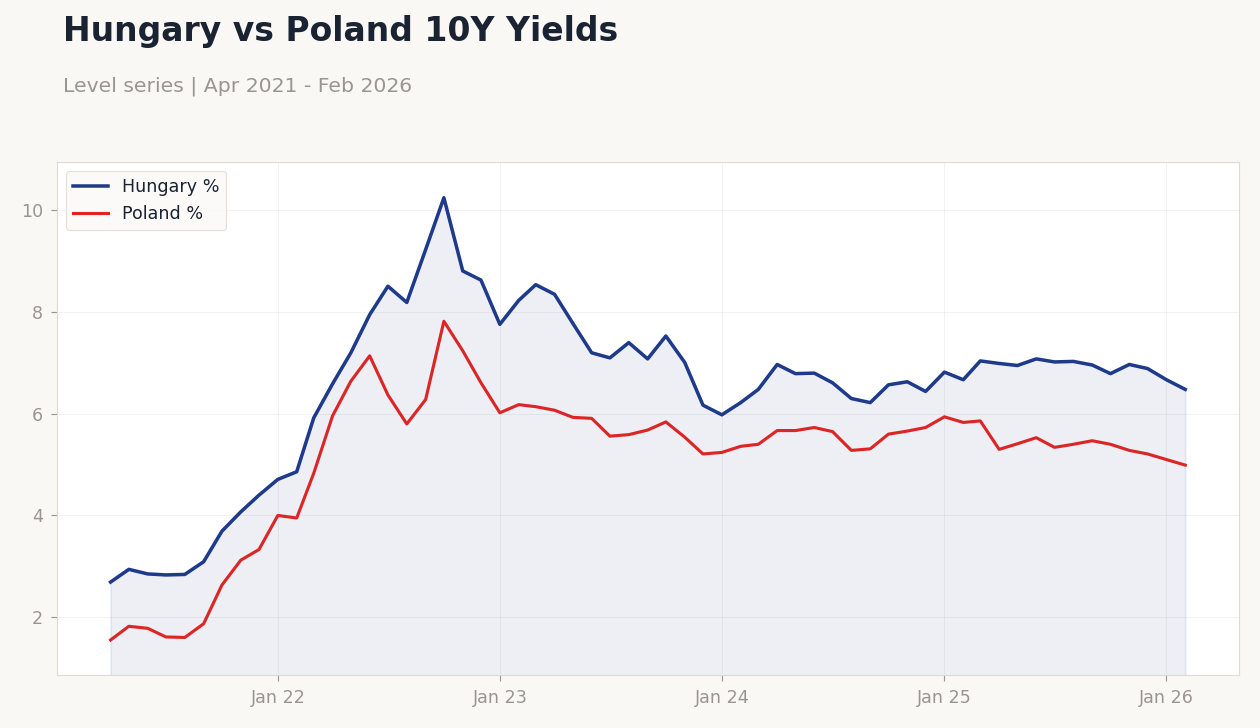

Hungary vs Poland 10Y Yields | Type: macro_line | Hungary %: 6.48 (2026-02-01) | Range: 2.69–10.25 | Trend(6pt): 2.69,7.95,7.4,6.57,6.89,6.48 | Poland %: 4.99 (2026-02-01) | Range: 1.55–7.82 | Trend(6pt): 1.55,7.14,5.59,5.6,5.21,4.99

Hungary vs Poland 10Y Yields | Type: macro_line | Hungary %: 6.48 (2026-02-01) | Range: 2.69–10.25 | Trend(6pt): 2.69,7.95,7.4,6.57,6.89,6.48 | Poland %: 4.99 (2026-02-01) | Range: 1.55–7.82 | Trend(6pt): 1.55,7.14,5.59,5.6,5.21,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Balance of Trade Final | -8,400m | - | 23:00 |

| Headline Unemployment Rate | 8.10 | - | 23:00 |

| Inflation Rate Year-over-Year Preliminary | 2.10 | - | 23:30 |

| Inflation Rate Month-over-Month | 2.96 | - | 23:00 |

| Inflation Rate Year-over-Year | 31.53 | - | 23:00 |

- Turkish markets dipped amid global risk-off, with BIST 100 down 0.57% and USD/TRY edging up 0.05%, as investors eye upcoming trade and unemployment data.

- Polish assets showed resilience, with iShares Poland up 0.17% and 10Y yields falling 2.16%, though news highlights doubts over NBP rate cuts due to Iran conflict risks.

- CEE currencies mixed versus EUR, with EUR/PLN +0.16%, EUR/CZK +0.17%, and EUR/HUF -0.25%, reflecting divergent policy outlooks amid steady regional data flow.

Yesterday's Recap

Emerging European markets displayed mixed performance on March 30, influenced by global commodity shifts and regional stability concerns. Turkey's BIST 100 index declined 0.57% to 12,626.40, pressured by Brent crude's 4.80% drop to 107.37, exacerbating energy import vulnerabilities for the inflation-prone economy. In Poland, the largest CEE economy, iShares Poland rose 0.17% to 34.64, supported by a 2.16% fall in 10Y government yields to 4.99%, signaling investor confidence despite no major data releases.

Hungary's 10Y yields decreased 2.85% to 6.48%, aiding a 0.25% strengthening in EUR/HUF to 386.43, while the Czech koruna weakened slightly with EUR/CZK up 0.17% to 24.54. Turkey's USD/TRY ticked up 0.05% to 44.47, underscoring ongoing lira fragility amid political constraints. Overall, the absence of key data left markets reactive to external factors like Bitcoin's 2.25% rise to 67,438.11 and gold's 1.55% gain to 4,596.20 as a safe-haven play, with Poland and Hungary outperforming Turkey.

The Day Ahead

Investors in Emerging Europe will focus on Turkey's final balance of trade data for March, expected around 23:00 ET, following a previous -8.4 billion deficit, which could highlight export challenges amid global slowdowns. Turkey's headline unemployment rate, also due at 23:00 ET, comes after an 8.1% prior reading and may signal labor market resilience despite high inflation. Poland's preliminary year-over-year inflation rate for March, slated for 23:30 ET, builds on the previous 2.1% print and could influence NBP's policy path amid euro convergence goals.

Looking slightly further, Turkey's month-over-month and year-over-year inflation rates are set for April 2 at 23:00 ET, with priors at 2.96% and 31.53% respectively, potentially pressuring CBRT for action. No major events are scheduled for Czech Republic, Hungary, or Romania today, allowing markets to digest these Turkish and Polish releases. Broader attention may turn to any EU fund disbursement updates affecting Poland and Hungary.

Other Economic Notes

Emerging Europe's energy dependency remains a key vulnerability, with Turkey and Poland particularly exposed to Brent crude fluctuations, as seen in yesterday's 4.80% oil price drop potentially easing import bills but risking growth slowdowns. (cont...)