Emerging Europe Macro Daily(Beta Mode)

CEE Bonds Rally on US-Iran Truce

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 12,921.60 | -1.45% |

| iShares Poland | 37.26 | +0.59% |

| EUR/PLN | 4.25 | -0.22% |

| EUR/HUF | 377.03 | +0.48% |

| EUR/CZK | 24.37 | -0.38% |

| USD/TRY | 44.50 | -0.16% |

| Brent Crude | 97.42 | +2.82% |

| Gold | 4,743.80 | -0.12% |

| Bitcoin | 70,807.14 | -1.58% |

| Poland 10Y Govt Yield | 4.99% | -2.16% |

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Poland 10Y Yield Trend | Type: macro_line | Poland 10Y Yield: 4.99 (2026-02-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,4.99

Poland 10Y Yield Trend | Type: macro_line | Poland 10Y Yield: 4.99 (2026-02-01) | Range: 1.6–7.82 | Trend(6pt): 1.82,6.37,5.68,5.66,5.1,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Year-over-Year | -1.80 | - | 23:00 |

| Friday (2026-04-10) | |||

| Industrial Production Year-over-Year | -1.80 | - | 23:00 |

- Polish rates hold steady amid cooling energy prices from US-Iran ceasefire, boosting bond markets across Central Europe.

- Turkish equities slide on lira pressures, while CEE currencies strengthen against euro.

- Global risk sentiment improves with Fed cut bets, lifting Poland's equity ETF.

Yesterday's Recap

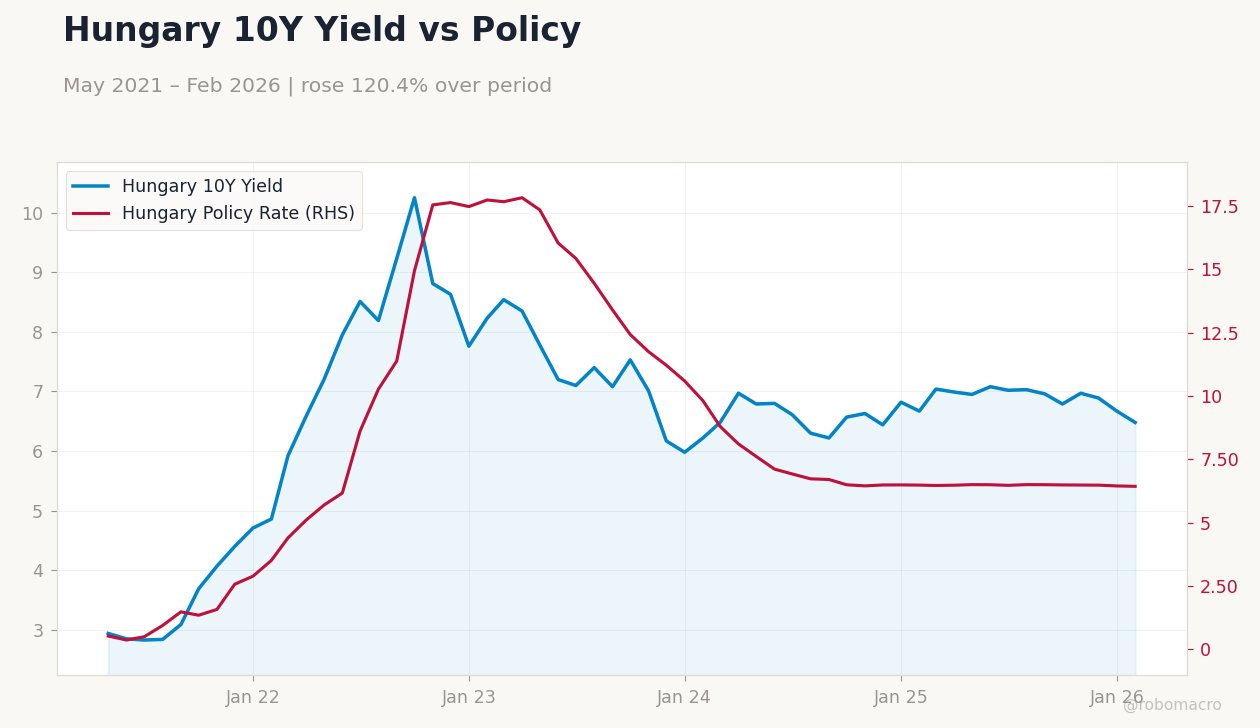

Emerging European markets showed mixed performance on April 8, with Turkey's BIST 100 index dropping 1.45% to 12,921.60 amid ongoing lira depreciation and fiscal concerns. In Poland, the largest CEE economy, the iShares Poland ETF rose 0.59% to 37.26, supported by expectations of steady NBP rates as a US-Iran ceasefire reduced energy price pressures. Hungarian bonds rallied, with the 10Y government yield falling 2.85% to 6.48%, reflecting improved EU fund access and lower inflation risks.

The EUR/PLN pair weakened 0.22% to 4.25, signaling zloty strength, while EUR/HUF rose 0.48% to 377.03 on forint volatility. Czech assets saw modest gains, with EUR/CZK declining 0.38% to 24.37 and Poland's 10Y yield dropping 2.16% to 4.99%. No major data releases occurred across the region, but news of reduced provisions at Poland's Bank Millennium highlighted banking sector resilience.

Turkey's USD/TRY edged down 0.16% to 44.50, tempering some FX pass-through worries.

The Day Ahead

Turkey's industrial production year-over-year for March is due today at 23:00 ET, with the previous reading at -1.8% and no consensus available, potentially signaling ongoing manufacturing weakness amid high inflation. Tomorrow repeats the same Turkish IP release, though it may reflect merged data from overlapping calendars. No other significant Emerging Europe events are scheduled, allowing markets to digest global cues like the US-Iran truce impacts.

Investors will watch for any ECB commentary that could influence CNB and MNB policy outlooks. Broader attention turns to potential EU fund disbursements for Hungary and Romania.

Other Economic Notes

Broader themes in Emerging Europe include energy import vulnerabilities, with the US-Iran ceasefire easing Brent crude pressures despite yesterday's rise to 97.42 (+2.82%), benefiting net importers like Poland and Czech Republic. Convergence criteria for euro adoption remain challenged, as fiscal deficits in Poland strain EU limits despite strong industrial rebounds. Turkey's distinct dynamics, with structurally high inflation, contrast CEE peers, underscoring the need for tailored FX interventions.