Emerging Europe Macro Daily(Beta Mode)

Poland Holds Rates Amid Iran Truce

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| BIST 100 | 13,689.00 | +1.12% |

| iShares Poland | 39.08 | +1.30% |

| EUR/PLN | 4.25 | -0.08% |

| EUR/HUF | 376.15 | +0.18% |

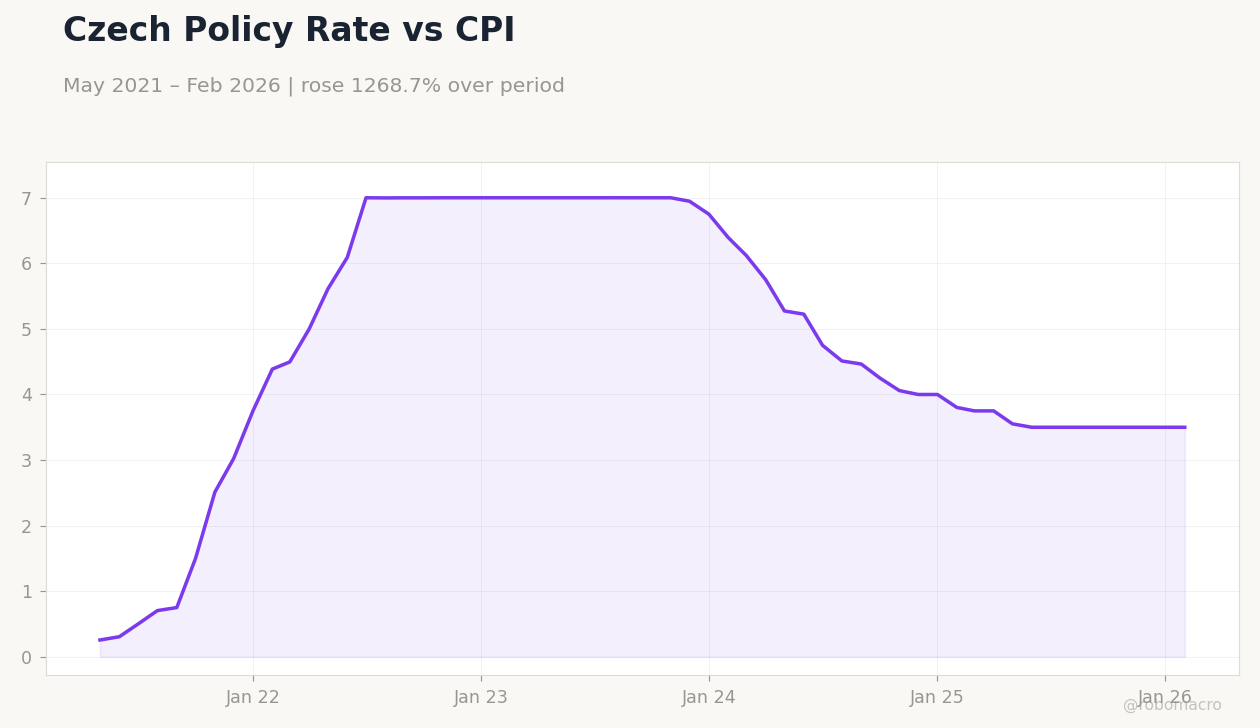

| EUR/CZK | 24.37 | +0.01% |

| USD/TRY | 44.64 | +0.34% |

| Brent Crude | 96.61 | +0.72% |

| Gold | 4,782.80 | -0.20% |

| Bitcoin | 72,027.41 | +1.27% |

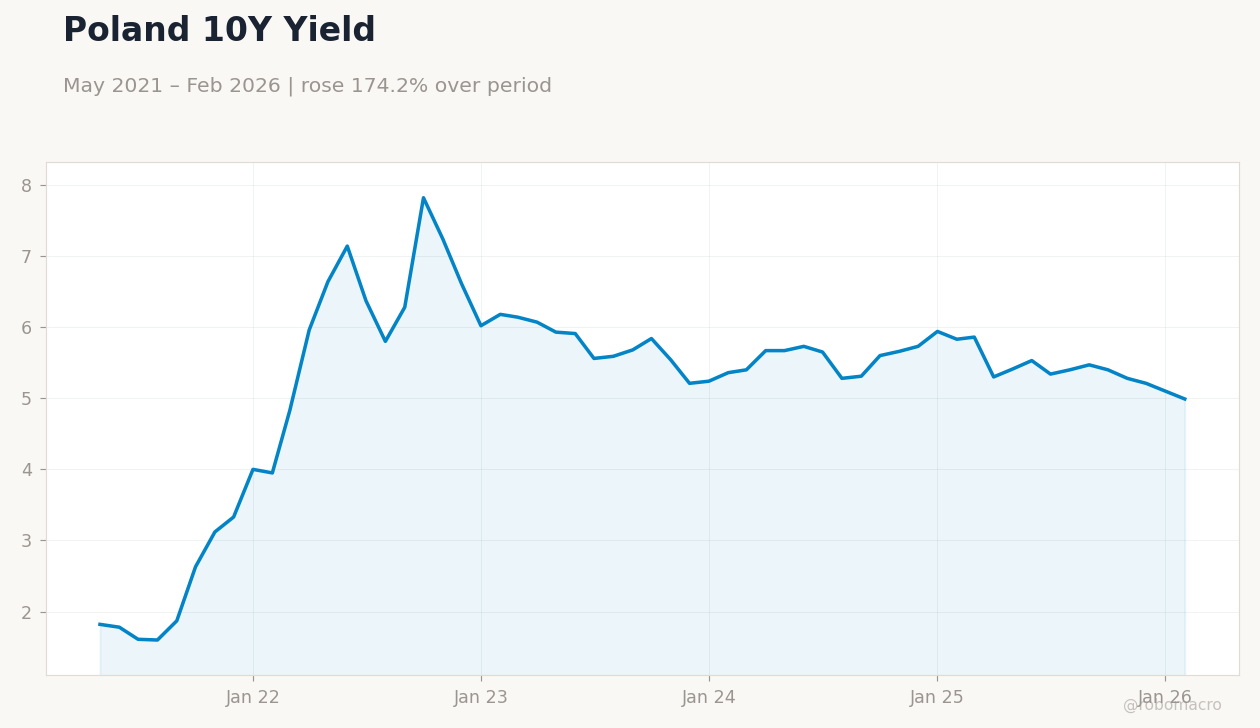

| Poland 10Y Govt Yield | 4.99% | -2.16% |

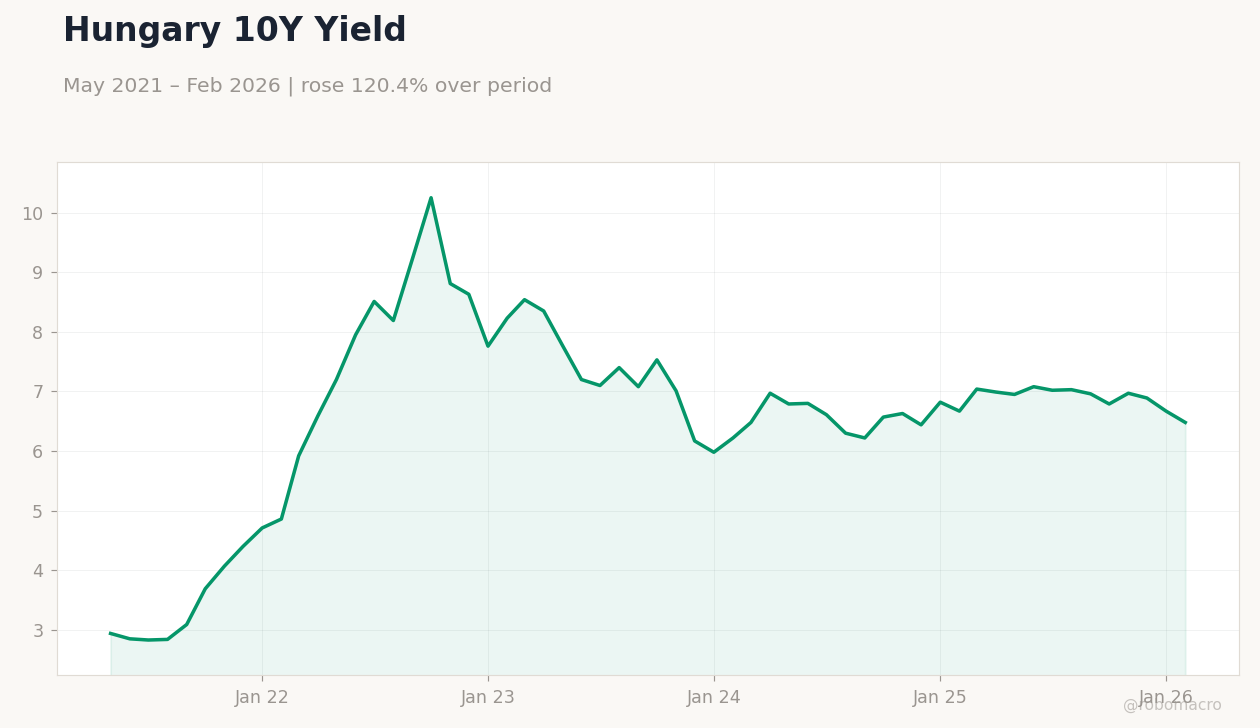

| Hungary 10Y Govt Yield | 6.48% | -2.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | Brent Price: 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(5pt): 62.38,114,91.37,77.84,127.6

Brent Crude Oil Price | Type: macro_line | Brent Price: 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(5pt): 62.38,114,91.37,77.84,127.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Year-over-Year | -1.80 | - | 23:00 |

- Poland's NBP expected to hold rates as Iran ceasefire eases energy costs and inflation pressures.

- Hungarian politics heat up with elections nearing and EU sanctions betrayal claims.

- Turkish industrial production data due, amid global stagflation fears impacting EM Europe.

Yesterday's Recap

Emerging European markets rallied modestly on reduced geopolitical tensions from the Iran truce, with Turkey's BIST 100 index climbing 1.12% to 13,689.00, driven by energy sector gains amid stabilizing oil prices. Poland's iShares ETF advanced 1.30% to 39.08, supported by a PIE study highlighting the economy's 42% growth boost from EU membership. The Polish zloty firmed slightly, with EUR/PLN dipping 0.08% to 4.25, as markets shrugged off Middle East uncertainties per Bankier.pl reports.

Hungarian assets showed resilience despite political noise, with EUR/HUF rising 0.18% to 376.15 and the 10Y government yield falling 2.85% to 6.48%. Czech koruna held steady, EUR/CZK up just 0.01% to 24.37. Overall, bond yields declined across Poland and Hungary, with Poland's 10Y yield dropping 2.16% to 4.99%, reflecting safe-haven flows amid global volatility.

The Day Ahead

Turkey's industrial production year-over-year is set for release at 23:00 ET, with medium impact expected; consensus is unavailable, but previous -1.8% suggests ongoing contraction risks from high inflation and lira weakness. No other major Emerging Europe data drops today, allowing focus on global cues like US inflation prints. Hungarian election developments could influence forint volatility as opposition challenges Orbán's rule.

Broader EU fund flows may see updates, potentially affecting Poland and Hungary's fiscal positions. Markets will watch for any ECB signals on euro convergence for Czech Republic and Romania. Turkish CBRT rhetoric might emerge post-data, given sticky inflation dynamics.

Other Economic Notes

Poland's EU membership has delivered substantial economic dividends, enlarging GDP by 42% through trade access and funds, bolstering its position as the largest CEE economy. Hungary faces convergence hurdles with its budget deficit exceeding EU limits, compounded by political risks from upcoming elections and sanctions disputes. Turkey's distinct macro challenges, including energy import dependency, contrast with CEE peers' euro-area linkages, heightening vulnerability to global oil swings.

Global Macro News

Global markets grapple with stagflation fears, as US headlines warn of low growth and high inflation amid rising tensions, potentially pressuring Emerging Europe's export-dependent economies like Poland and Czech Republic. (cont...)